by Carl Tannebaum, Chief Economist, Northern Trust

Are lower saving rates a sign of trouble ahead?

When I started earning money as a paper boy, my parents made me open a savings account at the local bank. Every week, I would take my pay (eight dollars!) and my passbook to a teller, who would update my principal and interest using a huge accounting machine. On rare occasions, I was allowed to withdraw fifty cents to purchase a milk shake at the local Woolworth’s.

By my count, there are at least five anachronisms in that story. But the focus on savings remains as relevant today as it was back then. Putting money aside is important for individuals, and the aggregate amount of saving is important for an economy. Recent discussions of saving rates and their relationship to spending illustrate how much has changed over the decades, and how much remains the same.

Saving rates rose immensely across economies during the pandemic period. Government support programs, many designed to stimulate demand, elevated household incomes. A considerable portion of the transfer payments were set aside for later use, given the uncertain outlook and restricted access to services like leisure and hospitality.

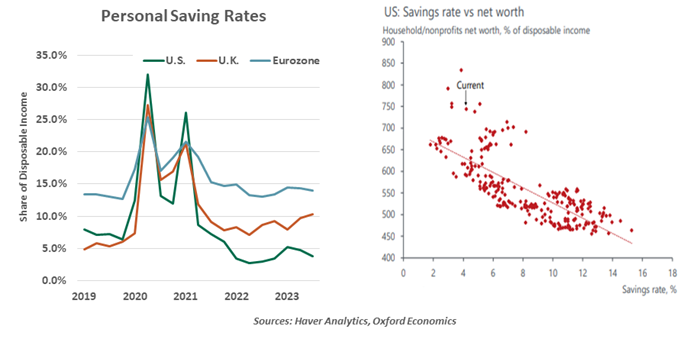

As economies reopened, households began to dip into their reserves. Saving rates are down significantly over the past three years; in the United States, they stand at about half of their pre-pandemic level. A high level of saving can provide fuel for future spending; low levels of saving might lead to belt tightening. This is one of the reasons forecasters have been expecting much more modest growth in consumption.

The saving rate, though, is an incomplete gauge of household wherewithal. Real incomes are the most direct driver of consumption; strong wage growth and falling inflation should continue to support spending this year.

Further, the saving rate is based on the difference between income and spending for a given period; it does not include accumulated savings done in the past. And measures of income do not include asset price appreciation. As shown in the chart above, high levels of wealth are closely correlated with low saving rates. In this way, rising net worth creates “wealth effects,” allowing investors to spend more out of their incomes without compromising their solvency.

The unexpectedly powerful run of equity markets during the last few months of 2023 (the U.S. S&P 500 rose by 11.7% during the fourth quarter alone) provided an enrichment that may have been overlooked by forecasters. Retailers had a much-better-than-expected holiday season, which boosted growth in gross domestic product (GDP).

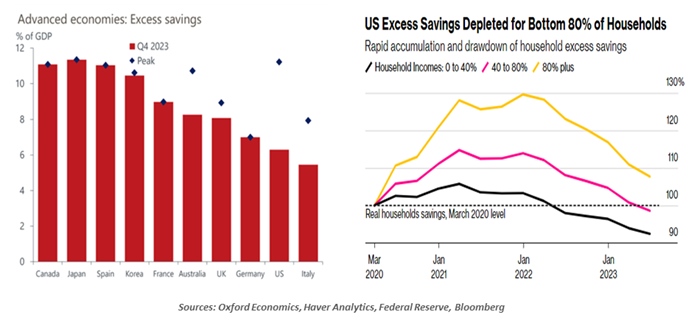

The data suggest that most countries still have a huge volume of savings in excess of pre-pandemic levels. According to Oxford Economics, western countries have between 6% and 11% of their GDP remaining in reserve. This is an immense sum: in the U.S., the total is more than $1.5 trillion dollars.

Savings have been depleted, but consumption has powered on.

These amounts, however, are concentrated among upper income households which have a lower propensity to spend. Those with more modest means, who spend more out of their incomes, have largely exhausted their extra resources; these families have begun borrowing again. Consumer debt, which dropped sharply during the pandemic, has returned to 2019 levels. The cost of interest on that debt will take a bite out of budgets in the months ahead.

It has been frustrating, but gratifying, to see consumption exceed expectations so consistently over the past few quarters. Nonetheless, projections (including ours) are once again calling for more modest results in the new year. While commentary often focuses on downside risks, potential upside cannot be dismissed. And that may delay interest rate cuts from central banks.

I made my first trip to a bank branch in many years recently. There were almost no tellers on duty. I was there to access my safe deposit box, which contained the savings bonds my children received when they were young; the time had come to disburse them to their rightful owners. The branch manager offered to determine current values for the certificates by taking a picture with his phone. Oh, how the times (and saving) have changed.

Copyright © Northern Trust