by Ryan Boyle, Senior Economist, Northern Trust

Small businesses are a vital part of the American economy. The U.S. Small Business Administration estimates that they represent over 46% of employment and account for the majority of new job creation. Small business openings are an expression of optimism in an entrepreneur’s ability and support from their community.

Particularly in the current cycle, small businesses have caught our attention as a bellwether of credit stress. While still performing well today, we will watch small businesses’ performance as an indicator of potential trouble.

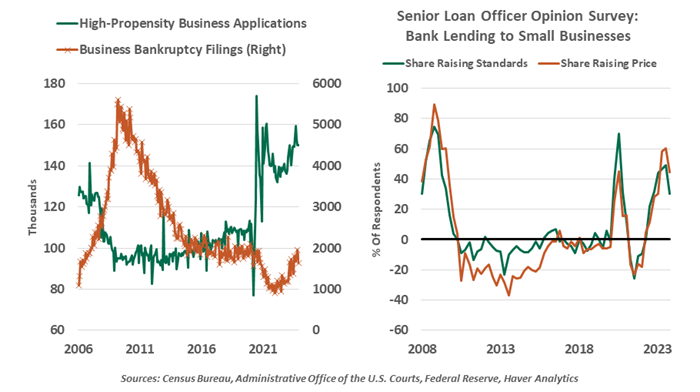

The sample to monitor has grown. During the pandemic, new business formation surged, and the trend has endured. Many people saw the interruption to their work routines as a cue to strike out on their own. Though the worst of the COVID era is in the past, new business applications and openings have remained elevated.

U.S. consumer review site Yelp observed that 2023 was a record year for new businesses appearing on the platform. Restaurants and travel destinations are well represented in this collection; demand for new experiences, dining out and takeout meals has endured. Home services like painting and decorating, which are easy to establish, were the largest category of new businesses. As the cost of new dwellings rose to levels unattainable for many households, consumers are instead spending on upgrading their existing homes.

Small business performance is an important economic indicator.

Small businesses are an important barometer because they are the borrowers most exposed to rising credit costs. They typically rely on revolving credit from banks, priced at variable rates. Debts in many sectors have been structured to avoid the impact of higher rates. Larger businesses issued high volumes of bonds before rates began to rise. Small businesses, however, cannot access capital markets and have felt the pain of higher financing costs.

The stress on small business owners is accumulating. They have had to reckon with the same inflationary forces as other firms, but they are less likely to have the pricing power of larger incumbents to sustain their margins. The monthly survey by the National Federation of Independent Business shows a rising share of owners see a lack of labor and tighter credit as their biggest risk; prior to the pandemic, credit never merited mention as a top concern.

Worries are justified, as banks continue to tighten their commercial lending standards. Even when credit is granted, the cost is higher, and limits are lower. Many lenders, particularly smaller community banks, have their fortunes tied to the small business environment. Recent earnings from publicly-traded banks have shown loan charge-offs and provisions for future losses in commercial loans were still rising through the end of 2023.

Some businesses will fail, an unfortunate but routine outcome. Much like anomalously low consumer credit defaults, the pandemic led business bankruptcy filings down to modern record lows in 2021. Most businesses qualified for programs like the Paycheck Protection Program (PPP), federal loans that were forgiven for businesses that maintained employment through the pandemic. These loans-turned-grants were lifelines during the COVID era, but that buffer has been depleted.

Bankruptcy data will help to gauge the business cycle. In 2023, monthly bankruptcy filings returned to 2019 levels; these are far below the peaks seen in the years following the 2008 financial crisis.

Inflation and interest rates have hampered the profitability of small firms.

We will also monitor business deaths, a grim term for the phenomenon of a business closing permanently. Where a bankruptcy may allow a business to reorganize and reopen, a death is a permanent closure identified after a business shows no employment activity for three consecutive quarters. Establishment deaths were elevated in 2022, but lower than births; on net, the number of small businesses is still growing.

The outlook calls for continued growth, which requires new firms to take new borrowings in order to create new jobs and new wealth. In the year ahead, the fates of small businesses may determine whether our economic landing is soft or hard.

Copyright © Northern Trust