by Russ Koesterich, JD, CFA, Portfolio Manager, BlackRock

In this article, Russ Koesterich discusses why a different approach to portfolio construction within equities is warranted in 2024.

Key takeaways

- 2023 was characterized by narrow leadership and multiple expansion.

- While last year’s gains have led to headline valuations appearing stretched, there are many segments of the market that are not as aggressively priced.

- With the expectation for more muted but broader equity returns in 2024, investors may want to barbell their equity exposure.

Last year’s sizeable and unexpected market rally was characterized by two, distinct themes: narrow leadership and multiple expansion. Gains were concentrated in a handful of names, and while several tech companies did post stellar earnings, most of the advance was driven by investors willing to pay more for a dollar of earnings (i.e. multiple expansion).

After the turmoil of 2022, investors took advantage of moderating inflation and the absence of a recession by bidding up most markets in 2023. With the notable exception of China, valuations rose in most equity markets. This was particularly true in two of last year’s big winners: the United States and Japan.

After a year of multiple driven gains, it’s healthy to question whether stock valuations have gotten stretched. Last year’s multiple expansion did indeed leave markets, particularly the United States, priced at a premium. The S&P 500 currently trades more than 19x forward looking 1 year (FY1) earnings. And unlike last year, when analysts were discounting a recession into earnings estimates, current expectations already bake in earnings growth of more than 10%.

That said, headline valuations are deceiving owing to last year’s other theme: narrow breadth. Outside of a couple of sectors and a relatively small number of growth names, most markets and industries are not priced aggressively. Except for India, virtually every major international market is cheaper than the United States. Japan, much of Europe and most of emerging markets trade at less than 15x FY1 earnings.

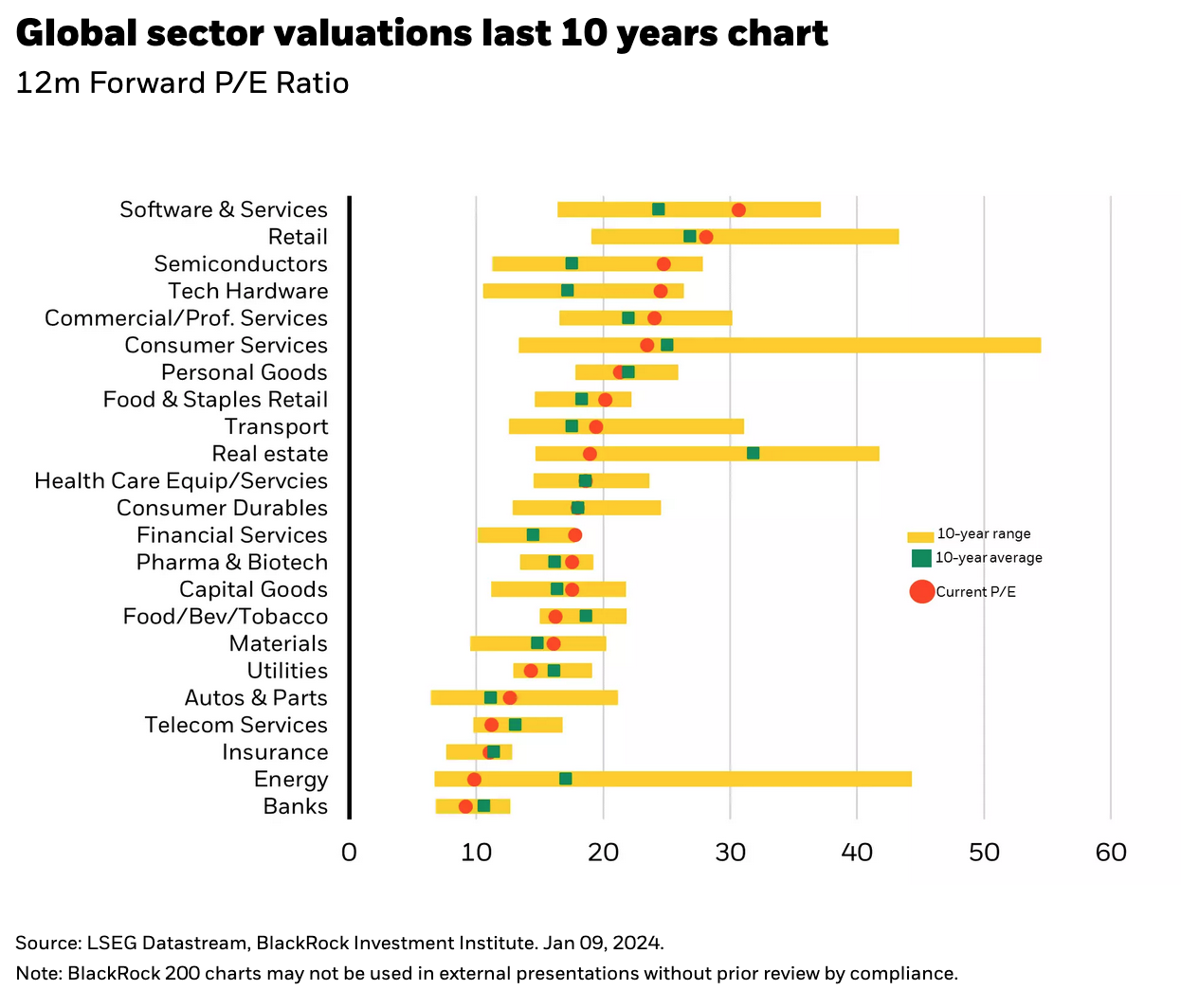

A similar pattern holds at the industry level. While much of the information technology sector trades at a premium to the broader equity market, most sectors and industries do not. Not only are most industries trading below the market’s multiple, but more than half are trading at or below their longer-term average valuation (see Chart 1).

A Barbell Structure for a Stronger Portfolio

Last year the best portfolio construction strategy was to build a concentrated portfolio, focused on a few sectors and, ideally, a handful of stocks. This year, with economic normalization likely to be the dominant theme, I would expect more muted but broader gains. Investors should consider paring some of last year’s winners to take advantage of the discounts available in many parts of the market.

To be clear, I am not advocating rotating into shaky markets or impaired, deep value companies. Given the likelihood for some slowing in the economy, this is probably the wrong time to go ‘bottom fishing’. Instead, I would suggest maintaining a somewhat smaller overweight in secular growth names, paired with high-quality value companies in some of last year’s laggard sectors.

What does this mean in practice? Continue to emphasize names and themes exposed to secular trends tied to artificial intelligence, semiconductors, healthcare services and internet commerce. At the same time, consider adding to names in segments of the market that were left behind in last year’s rally, and as a result are trading at a substantial discount. Examples of the latter include energy, autos, airlines, and aerospace and defense. To be clear, this does not suggest abandoning stocks geared to winning secular themes, but perhaps owning a bit less to take advantage of a number of names and sectors that are surprisingly cheap.

Copyright © BlackRock