Food prices illustrate several challenges of containing inflation.

by Carl Tannenbaum, Chief Economist, Northern Trust

Editor’s Note: We are publishing this abbreviated commentary in advance of Thanksgiving. For those celebrating, we hope you have a wonderful holiday.

I’m expecting a record crowd for Thanksgiving this year. Three tables, spread over three rooms. Three turkeys, three quarts of cranberry sauce, and three pumpkin pies. Oh, and I will need three days afterwards to rest and recuperate.

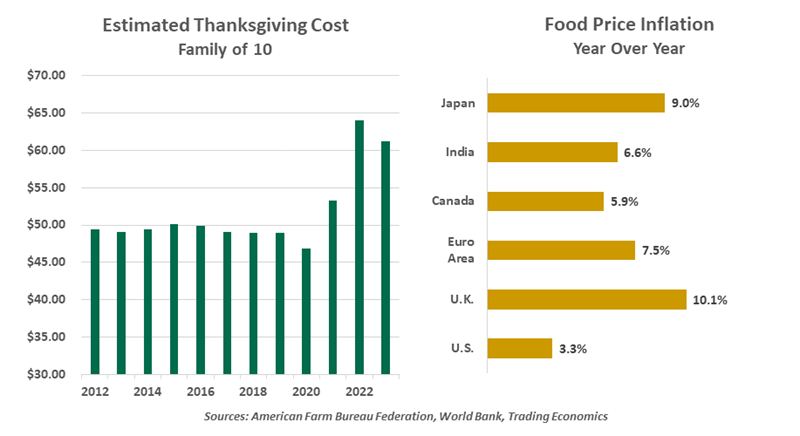

At least the cost of this year’s meal will be a little more modest. The American Farm Bureau Federation announced that feeding a group of 10 will cost just over $61 this year, down 4.5% from last year. That is welcome relief, but the price of the meal is still 15% higher than it was in 2021.The cost of Thanksgiving staples traces a trajectory that is similar to what we have seen globally. The United Nations index of world food prices is down about 25% from its 2022 peak, but it is still about 25% higher than the pre-pandemic reading. Groceries have gotten a little cheaper, but they are still taking a big bite out of household budgets.

Disruptions caused by the pandemic and the war in Ukraine shocked the supply chains that feed the world. Higher energy prices have affected costs of production and transportation. Labor shortages have challenged harvesting and processing in spots.

Regional markets have had to cope with a series of additional disruptions. Avian flu reduced supplies of eggs and poultry in the United States; restricted grain exports from India reduced the availability of staples in Europe; and adverse weather patterns have affected harvests in a series of locations. Brexit has complicated the import of food in the United Kingdom. In several countries, concerns have arisen that industry concentration among supermarkets is also a factor keeping prices high.

Food is a basic essential. When most goods get more expensive, consumers can substitute or defer purchasing; but those options are more difficult to exercise when it comes to groceries. With the prices of so many items rising sharply, it becomes harder to keep bills down. And that takes a toll on household finances: food absorbs between 6% and 10% of the average family’s budget in developed countries, and up to 50% in some developing countries.

Economists and the average household view inflation quite differently. The former are focused on rates of change in prices, while the latter is often more focused on the level of prices. Economists will note that inflation for food is in decline, but shoppers will still feel as if they need special financing to purchase a holiday roast.

Since food prices can be volatile, they are removed from core measures of inflation. But they contribute importantly to the way that households perceive inflation. Workers trying to keep pace with the expense of feeding their families have pressed for higher wages, in some cases striking to do so.

For all of the anxiety over food prices in developed countries, it could be a lot worse. There are a handful of nations including Egypt, Argentina and Turkey that are currently experiencing food inflation of more than 50%. These countries have weak currencies, raising the cost of imports. The hyperinflation creates significant challenges for both governments and the populations they serve.

And we shouldn’t overlook the 35 million refugees around the world, who often wonder where their next meal is coming from.

The cost and scarcity of food has historically been a contributor to social unrest, so food subsidies have been employed to keep the peace. But these programs expand public debt and deficits. And once in place, they are politically difficult to remove.

So while feeding all of my guests will cost a pretty penny, I am thankful for the opportunity to host them. I’m thankful for having amazing friends and family members, and thankful that we are free from hunger. And I’m thankful for the global agencies that work so hard to alleviate hunger when it arises.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions. © 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

Carl R. Tannenbaum

Executive Vice President and Chief Economist

Carl Tannenbaum is the Chief Economist for Northern Trust. In this role, he briefs clients and colleagues on the economy and business conditions, prepares the bank's official economic outlook and participates in forecast surveys. He is a member of Northern Trust's investment policy committee, its capital committee, and its asset/liability management committee.