by Kristina Hooper, Chief Global Market Strategist, Invesco

Key takeaways

Manufacturing weaknessPurchasing Managers’ Indexes painted a weaker picture for manufacturing in Japan, the eurozone and the UK. |

Treasury yieldsThe 10-year US Treasury yield continued its roller coaster ride as a wide range of factors contributed to big swings in this key data point. |

Earnings seasonSo far, companies who beat 3Q earnings expectations have not generally been rewarded by markets, but earnings misses have been punished. |

Manufacturing looks weaker in Japan, the eurozone and the UK

We got a flurry of Purchasing Managers’ Index (PMI) readings last week for a variety of different economies. I’m always interested in PMI surveys because they give us a snapshot on the state of an economy.

- Japan. Japan’s flash PMI readings1 for October showed us a bifurcated economy where the services sector is stronger than the manufacturing sector. Manufacturing PMI clocked in at 47.6, which is in contraction territory. Services PMI was 51.1, which is down from last month’s reading of 53.8 but is still in expansion territory, no doubt helped by fiscal stimulus and the accommodative monetary policy environment.

- Eurozone. The eurozone economy is under significant pressure, with flash composite PMI2 at a 35-month low. There is greater weakness in the manufacturing PMI at 43.1. Services PMI is better at 47.8, but remains in contraction territory. Of particular note is the extreme weakness in Germany’s manufacturing PMI, which clocked in at 41.4. Dr. Cyrus de la Rubia, Chief Economist for the Hamburg Commercial Bank, which conducts the PMI survey, explained: “In the Eurozone, things are moving from bad to worse. Manufacturing has been in a slump for sixteen months, services for three, and both PMI headline indices just took another hit. In addition, all subindices point very consistently downwards, too, with only a few exceptions.” He said he wouldn’t be surprised to see a “mild recession” in the eurozone in the second half of this year.

- UK. The weaker manufacturing picture can also be seen in the UK, where manufacturing PMI was 45.3 while services PMI was 49.2.3 Both are in contraction territory, but manufacturing is in much worse shape — although it seems to be becoming an increasingly challenging environment for the UK consumer.

10-year US Treasury yield continues its roller coaster ride

The 10-year US Treasury yield4 rose to 5.02% early on Oct. 23, but closed the day significantly lower. On Oct. 26, the yield again moved higher, only to finish the week at 4.83%, likely on increased demand for Treasuries as a “safe haven” asset class with the Israel-Hamas war intensifying. It’s likely to continue moving in a wide range given the many different factors impacting the 10-year yield and the lack of clarity from the US Federal Reserve (Fed) on monetary policy.

Markets seem to be ignoring better-than-expected earnings

Third-quarter earnings season5 is in full swing. In the US, 78% of S&P 500 companies have reported a positive earnings-per-share surprise and 62% have reported a positive revenue surprise (49% of S&P 500 companies have reported earnings thus far).

In Europe, 57% of Stoxx600 companies have beaten earnings estimates so far, while in Japan, 58% of Topix companies have beaten earnings estimates. There are still more companies yet to report, but the key takeaway thus far is that, in general, companies that beat earnings expectations are not being rewarded by markets, but earnings misses are being punished.

China plans to boost fiscal spending targets

Chinese policymakers have announced a significant increase in debt to fund targeted fiscal spending.6 We don’t have a lot of specifics, but we can assume that this signals a focus on accelerating economic growth despite it already seeming to be on track to meet the government’s 5% gross domestic product (GDP) growth objective. Just as targeted fiscal spending thus far has been positive for consumer sentiment and spending, I expect this should do the same but even more substantially.

US inflation tame but economy shows strength while inflation expectations rise significantly

There were no surprises with the Fed’s most watched gauge of inflation, core Personal Consumption Expenditures. It rose 0.3% month-over-month for September, which was in line with expectations, and 3.7% year-over-year.7 This enabled markets to heave a sigh of relief, as this print did not conflict with the thesis that the disinflation process remains underway.

However, there were a few flies in the ointment last week. The third quarter GDP print showed a robust economy powered by the American consumer. However, that reflects consumer spending before the reinstatement of student loan payments. We are starting to see signs that the consumer is weakening on the margins — for example, auto loan delinquencies are on the rise — and that should result in some softening of demand going forward.

Then came the University of Michigan consumer inflation expectations reading for October, which showed that inflation expectations have risen dramatically for the one-year ahead period and modestly for the five-years ahead period.8 Short-term inflation expectations are typically more volatile and are often driven by energy prices. We saw a similar spike in one-year ahead inflation expectations from March to April 2023, when there also was a major increase in the price of crude oil.

It’s important to note that the Fed pays close attention to inflation expectations, although it is focused on ensuring that longer-term inflation expectations (rather than shorter-term ones such as the one-year reading) are “well anchored.” Given its focus on the longer-term data, I would not expect the Fed to hike rates at its November meeting despite the higher inflation expectations print.

Central banks keep rates steady in Canada and Europe

Last week, the Bank of Canada and then the European Central Bank (ECB) decided to keep policy rates static. For Europe, this comes after 10 consecutive rate hikes. ECB President Christine Lagarde recognized that the risks to economic growth lean to the downside (but she was quick to note that any discussion on rate cuts is very premature).

Over the last several years, the Bank of Canada has been at the vanguard of monetary policy moves, so it seems fitting that its decision last week to keep rates steady for two meetings in a row following 10 rate hikes preceded a similar decision from the ECB — and I believe it’s likely to foreshadow a similar decision from the Fed this week. The Bank of England and Bank of Japan also meet this week.

Update: Shortly after I published this piece, the Bank of Japan (BOJ) decided to further increase the flexibility in its yield curve control policy at its October Monetary Policy Meeting. The BOJ previously set a strict cap of 1.0% for the 10-year Japanese government bond (JGB) yield. But it has now decided that 1% should be a “reference” (not a strict cap), which effectively allows the yield to rise above 1% when the BOJ thinks it is appropriate. This new policy was a surprise to markets, although perhaps it shouldn’t have been given the BOJ’s upward revision to median forecasted core inflation to 3.8% from 3.2% for fiscal year 2023, as well as the recent sharp increase in the 10-year US Treasury yield.

BOJ Governor Kazuo Ueda emphasized the importance of next year’s Shunto (the annual collective wage bargaining between companies and labor unions) in helping to determine whether or not Japan will be on track to achieve a sustainable 2% level of inflation. It is widely expected that a considerable wage increase from Shunto could trigger a tightening move from the BOJ, in the form of a hike in the targeted 10-year JGB yield and/or abolishment of its negative interest rate policy. The BOJ’s upward revision to its inflation outlook has certainly increased the probability of tightening by the BOJ in 2024, in our view.

The higher likelihood of achieving sustained 2% inflation in Japan increases the probability that Japan could experience stronger domestic growth, which would likely benefit Japanese equities. From a cyclical perspective, the Japanese economy is currently maintaining its strength, and we think it is unlikely that the limited rise in Japanese long-term bond yields and yen appreciation will undermine economic growth, which should continue to support Japan equities in the short run.

An important life lesson

I would be remiss if I didn’t note the passing of veteran strategist Byron Wien last week. I was lucky enough to be in his company a few times over the last three decades, and I was struck by his wisdom, his humour, and his commitment to mentoring. I am particularly inspired by this piece of wisdom from his 20 life lessons: “When your children are grown or if you have no children, always find someone younger to mentor. It is very satisfying to help someone steer through life’s obstacles, and you’ll be surprised at how much you will learn in the process.”

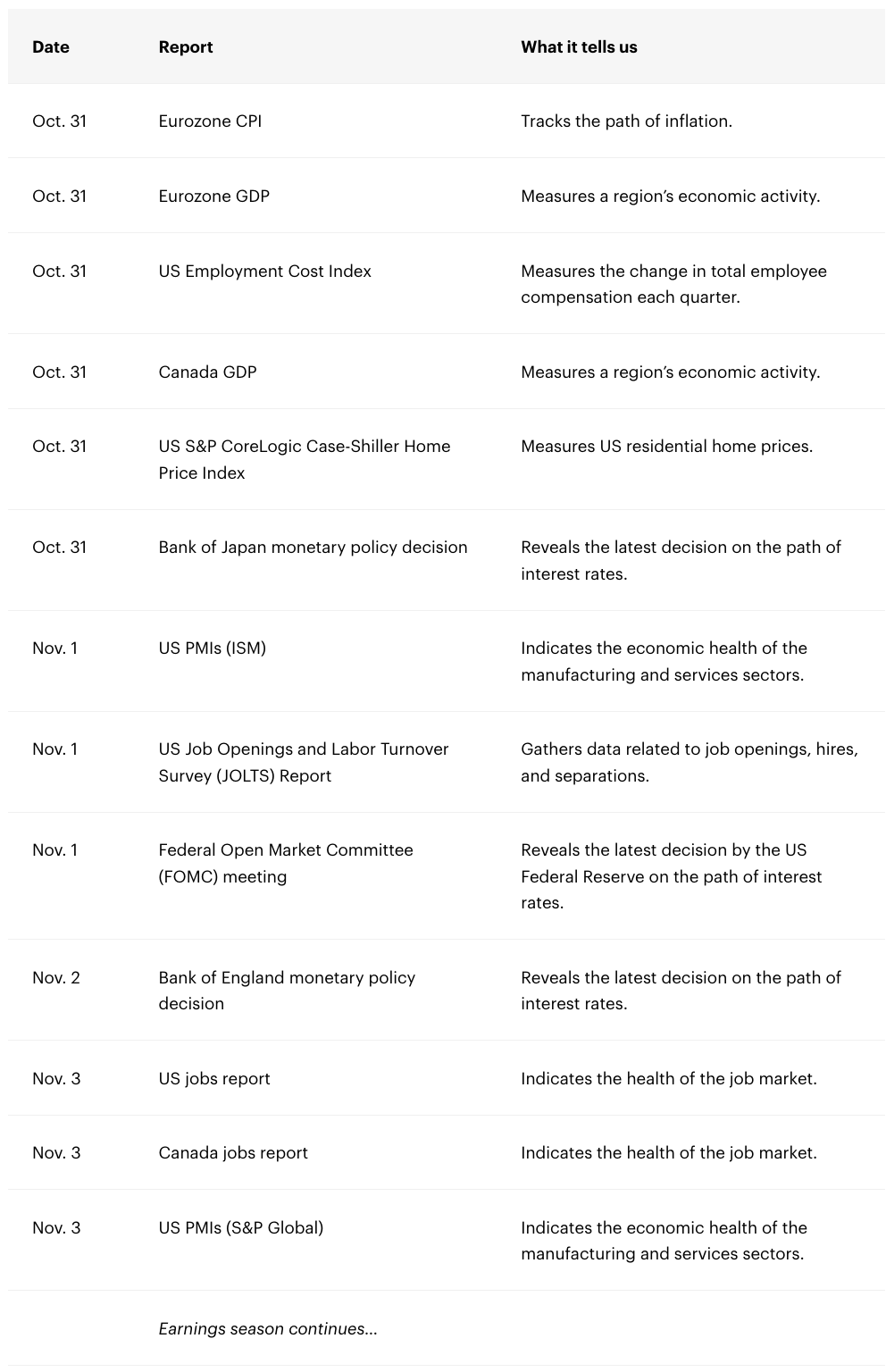

Dates to watch

The data reports aren’t slowing down. See below for a list of what I’m watching. And on Nov. 1, join me on X, formerly known as Twitter, as I share my real time views of the Federal Open Market Committee interest rate decision and key takeaways from Fed Chair Jay Powell’s press conference as it happens.

With contributions from Tomo Kinoshita

Copyright © Invesco

Footnotes

1 Source for all Japan PMI data: S&P Global / AuJibun

2 Source for all eurozone and German PMI data and quotes: S&P Global/HCOB

3 Source: S&P Global

4 Source for all US Treasury yield information: Bloomberg, L.P., as of Oct. 26, 2023

5 Source for all earnings season information: Factset Earnings Insight, JP Morgan Earnings Season Tracker

6 Source: Reuters

7 Source: US Bureau of Economic Analysis

8 Source: University of Michigan Survey of Consumers, October 2023