by Vaibhav Tandon, Senior Economist, Northern Trust

The BRI has left both China and the signatories saddled with debt.

“Road to Nowhere” is a classic rock song by American band Talking Heads with a reflective vibe. It speaks to the aimlessness and uncertainty of life, but still finds hope in the journey. The lyrics suggest that it is sometimes necessary to take a symbolic ride to nowhere and accept what comes with “taking that ride.”

China’s Belt and Road Initiative (BRI) feels much like a road to nowhere. Last week, Beijing hosted representatives of several nations to mark the tenth anniversary of the BRI. During that decade, China has become the lender of first resort for many low- and middle-income economies, pouring an estimated $1 trillion into 3,000 projects. About 150 countries have signed on for the BRI, hoping to upgrade their infrastructure.

The BRI has opened new markets for Chinese output and helped it diversify sources of crucial commodities. Goods worth $19 trillion were traded between China and BRI nations over the past decade. To take one example, China used to rely heavily on the U.S. for supplies of soybeans. But amid the ongoing tariff war between the two countries, Beijing has increased its purchases of soybeans from countries like Brazil, Latin America’s largest recipient of BRI funding. The BRI has also bolstered China’s energy security: more of its gas flows through BRI-funded pipelines from Central Asia and Russia.

The BRI was touted a means to boost the Chinese economy: absorbing Chinese corporations' excess capacity, attaining greater acceptance of the renminbi and bolstering the nation’s alliances. Unfortunately, those objectives are far from realized. Overall, exports are struggling amid the greater focus on “friendshoring.”

BRI investments were also aimed at stimulating development and bringing jobs to host nations. Instead, BRI projects have faced constant criticism over issues like labor violations, corruption and environmental damage. Chinese loans are covered in secrecy, with lenders funding activity through special-purpose companies instead of host governments. Deals come with expensive lending terms compared with the financial support from multilateral institutions like the International Monetary Fund (IMF).

But the biggest concern surrounding the Belt and Road Initiative is that it plunges nations into a debt trap. Sri Lanka granted China control over the Hambantota port project on a 99-year lease in 2017 because it could not pay its debt. While debt renegotiations, write-offs and financial assistance are the most common outcomes when BRI loans do not perform, Sri Lanka’s episode is a cautionary tale.

As a result, the BRI is facing increasing political pushback in many countries. Malaysian and Tanzanian authorities canceled BRI deals amid a growing backlash. Geoeconomic fragmentation is also causing a re-think about the benefits of accepting support from China. Italy, the only BRI signatory from the Group of Seven nations, is set to exit in the coming months.

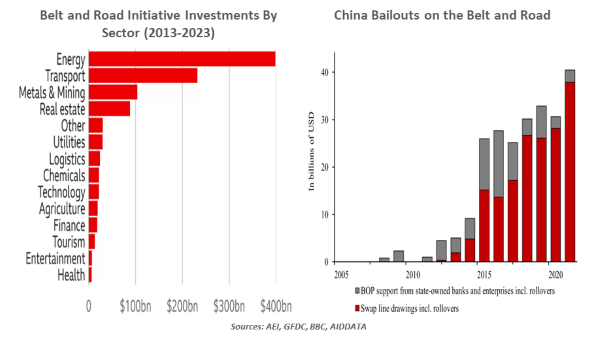

As the Chinese economy slows, the BRI is losing steam. The average BRI deal size decreased by 48% from its 2018 peak to $392 million in the first half of 2023. Limits on external lending by Chinese banks have been reduced by 50% in the past five years.

China is now realizing the true cost of the BRI. A study by the Rhodium Group showed that close to $80 billion worth of borrowing had turned bad over the past three years. China’s external bailouts have surged and correspond to over 20% of total IMF lending over the past decade.

This has put the Chinese government in a tight spot. A struggling domestic economy will likely make allocation of resources for international projects more challenging and could fuel discontent.

A change of approach is the need of the hour, else the One Belt and One Road Initiative risks turning into a one big expensive mistake—and a long ride to nowhere.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions. © 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

Copyright © Northern Trust