by Ryan Jame Boyle, Senior Economist, Northern Trust

A favorable inflation report is just one step in a long journey.

My extended family has a long-running tradition of Super Bowl parties, which involve some friendly wagering. Every now and then, someone on track to win a squares pool begins counting the prize money…until a last-minute play changes the game’s score. The moral: never celebrate too soon.

Coverage of the recent inflation data took me back to those Super Bowl parties. There is reason for cheer, and I welcome signs of progress. But victory laps are premature; plenty of time remains on the clock.

Let’s start with the good news. The June consumer price index (CPI) carried a headline gain of only 3.0% year-over-year, its lowest reading in over two years. Much of that improvement was driven by lower energy prices. Excluding food and energy, year-over-year core inflation improved to 4.8% from 5.3% a month earlier. Drilling into the data revealed more reasons for optimism: core service prices, a point of emphasis for the Fed, were flat on the month.

Other perspectives on inflation are also encouraging. There are myriad ways to slice and dice price data to reflect different purchase baskets and behaviors. The “trimmed mean” CPI removes categories that are extreme outliers to show a more stable signal of underlying inflation, and it is improving. The Harmonized Index of Consumer Prices (HICP) approach, used in Europe, excludes approximations of housing costs and shows a complete recovery.

Proxy metrics ranging from import prices to used car indices to freight rates to real-time price data all reflect solid progress in the effort to tame the price level. And lower inflation serves to increase real bond yields, which will raise the cost of borrowing and further cool the economy.

As encouraging as all this sounds, the challenge of controlling inflation persists.

This month’s CPI improvement came from a favorable base effect: at this time last year, energy prices (among other commodities) were surging. Food and energy markets are notoriously volatile, and they are therefore excluded from the core inflation measure that central banks target.

The Federal Reserve focuses on the deflator for core personal consumption expenditures. From January through May, the year-over-year change in this gauge has measured 4.6% or higher. Repeatedly, Fed Chair Jerome Powell has cited a need to see sustained progress toward the target of 2% before rate cuts will be considered; this year has brought no progress at all.

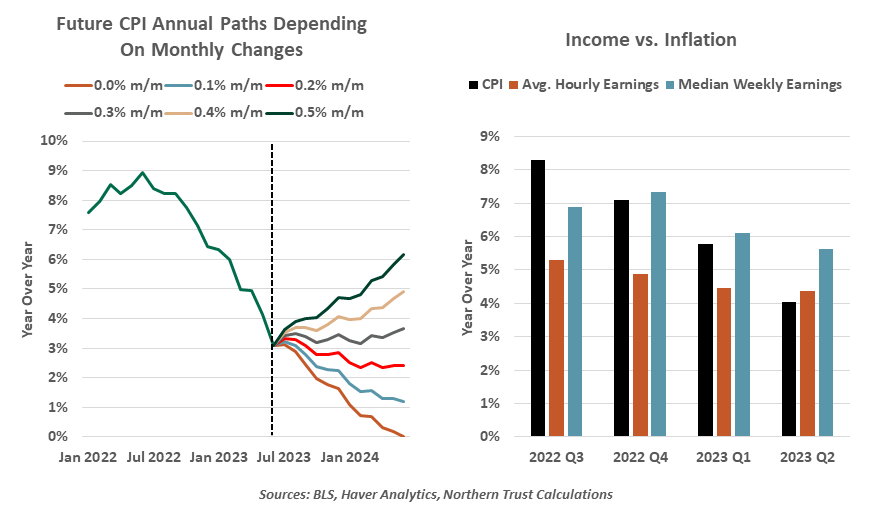

The year-ago base effect will present a further complication. As the most painful months of inflation last year age out of the comparison, the overall inflation rate is likely to shift higher in year-over-year comparisons. After the surge of 2021-22, inflation in most categories has settled into a steadier pace that is exceeding a 2% annual rate. Steadily low monthly inflation readings will be needed to hold down the year-over-year rate, and feels like wishful thinking in an economy with strong momentum.

Inflation does not materialize out of nowhere; something must push prices higher. Among other drivers, much of the current round of inflation has come from higher costs, passed along to final prices. An important cost driver has been higher wage gains, which remain historically elevated. Labor-dependent services will struggle to see sustained inflation declines. And now, for the first time since March 2021, the rate of inflation is below the growth rate of average hourly earnings. After losing so much ground to inflation, workers are starting to get real wage gains, which may fuel more spending.

Analysis of monthly inflation details is an important exercise, but the direction of prices should be kept in a broader context. The macro economy benefitted for decades from structurally deflationary forces that are now weakening. Globalization allowed goods to be produced wherever it was most cost-effective to do so; today, a push toward re-shoring and supply chain resiliency will add some inefficiencies and costs to the system. Labor is in short supply; wage pressures will be difficult to contain. Re-shoring, if successful, will only add to demand for the limited supply of workers. Government investment to support domestic resiliency will also add to economic activity, counteracting any cyclical cooling.

Finally, we must be modest about our inflation forecasts, which have persistently underestimated what actually occurred. Even if the cooling is finally upon is, it has arrived two years too late. We cannot be too confident in projections that price increases will recede smoothly from here to the targeted range.

Central bankers are challenged to make sense of all of this, and differences of opinion are growing. A dove could make a case for keeping interest rates steady: perhaps it’s time to stop and let inflation run its course. A hawk could retort that inflation remains too high, and it will require more restraint to keep inflation and its expectations anchored.

The hawks are having their moment. Several central banks (notably in Canada and Australia) returned to hiking after a pause; the Fed looks likely to follow suit. Policymakers have acted decisively to combat inflation over the past 18 months, and we don’t see that changing now.

On the brighter side, if disinflation is really here to stay, any further hikes will be limited. A pause will sustain, and cuts will come into view. Given the difficulty we are witnessing calling an interest rate peak, we expect a contentious debate leading to the decision to start cutting. Fed leaders do not want to repeat past mistakes of premature easing that had to be reversed, a disorienting experience that damages credibility.

If the beginning of durable disinflation is upon us, I will be delighted. But to respect lessons learned at Boyle family Super Bowl parties, I need to be sure of the outcome before I plan any celebrations.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.