by Tony Davidow, CIMA®, Senior Alternatives Investment Strategist, Franklin Templeton Institute

While the financial media has focused on the headwinds for commercial real estate and the challenges the office and retail sectors face, this narrative ignores the differences across sectors and the potential opportunities available in today’s market environment, according to Franklin Templeton Institute’s Tony Davidow.

Based on its historical growth and income characteristics, commercial real estate (private real estate) represents a significant allocation for many institutions and family offices. According to the 2022 Institutional Real Estate Monitor,1 real estate represents an 11% global allocation in institutional portfolios, and according to the UBS Global Family Office Report,2 real estate represents a 13% allocation in family office portfolios. In recent years, private real estate has been more accessible to high-net-worth investors due to product innovation, as well as the willingness of institutional-quality managers to bring products to the market.

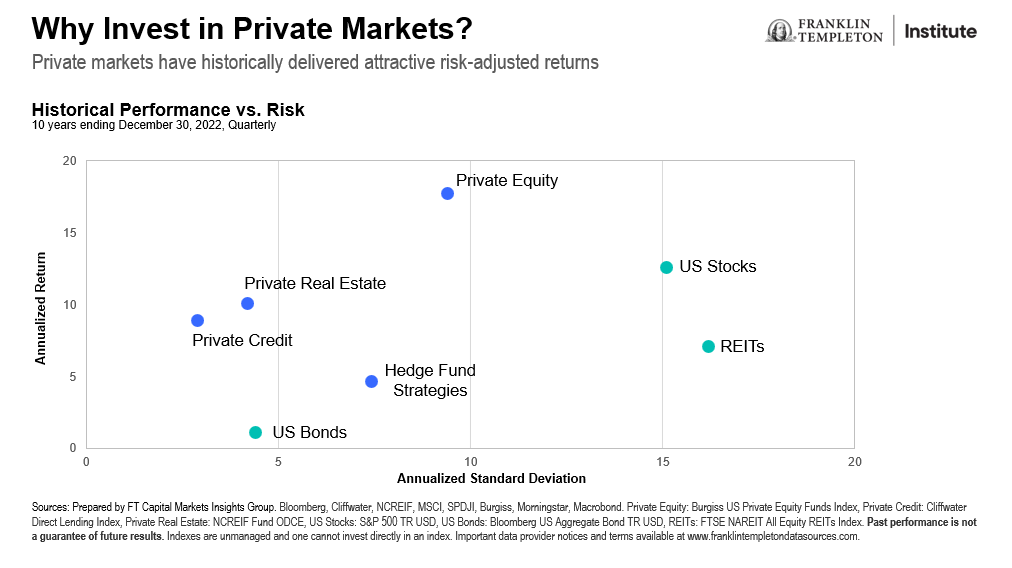

Last year, we were reminded of the limitations of the 60/40 portfolio3 and the need for an expanded toolbox to meet client goals. Consequently, advisors and investors have sought alternative sources of growth and income, and an effective way to dampen volatility and hedge inflation. As the data below illustrate, real estate has historically delivered attractive risk-adjusted returns relative to stocks, bonds and publicly traded real estate investment trusts (REITs).

Private real estate has historically delivered higher income than most traditional fixed income options4 and publicly traded REITs. Private real estate managers also can increase rents in rising inflationary environments.

The current market environment

After interest rates rose dramatically throughout 2022 and the early part of 2023, some have suggested that this would provide headwinds for real estate. Coupled with the tighter credit conditions in the post-Silicon Valley Bank (SVB) environment, and the fact that office and retail sectors were still struggling with occupancy levels, there were concerns about risks across the overall private real estate market.

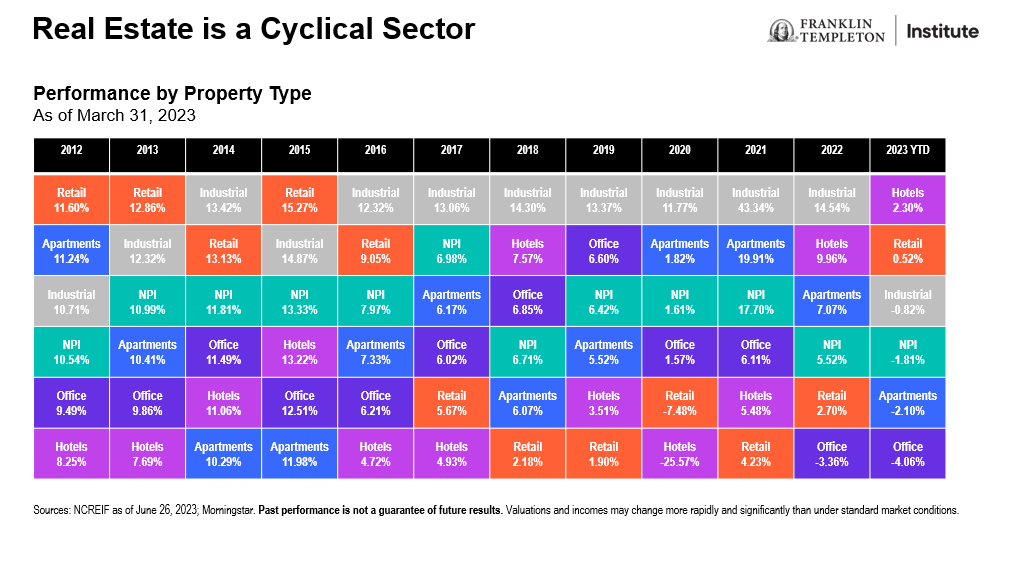

As the data below show, the office sector was struggling before the COVID-19 pandemic and will likely struggle for the foreseeable future. However, private real estate represents a diverse set of sectors, which are responding to a changing US economy. While offices have struggled over the last several years, the industrials property sector has been a growing sector of the market, driven by Amazon fulfillment centers and other industrial-use facilities.

Real estate valuations are ultimately about supply and demand. While there might currently be an oversupply of office and retail space, there is a shortage of industrial and multifamily real estate. We believe that the changing economy is driving growth in industrials, which represents a long-term secular trend. Millennials are entering their peak earning years, and consumers will continue to buy online, which leads to increased demand for fulfillment centers across America. E-commerce sales are forecast to grow at 5-10% annually,5 continuing to gain market share from brick-and-mortar retail stores.

Multifamily housing represents another bright spot with pent up demand and an overall housing shortage (3-5 million units by some estimates).6 We have experienced strong job growth and a migration from high-tax states (New York, New Jersey, Connecticut and California) to low-tax states (Florida, Texas, North Carolina and Tennessee), which is where we see many opportunities in multifamily housing.

With a growing remote workforce and flex schedules, the office building segment will continue to face challenges in evolving to meet today’s needs. Vacancy rates are elevated, sentiment is negative and lending conditions are tight. Certain markets may regain their prior occupancy levels, while others may need to revert their office space into a more modern and scalable solution.

Not all real estate is created equal—and not all sectors will provide the same results in the future. We believe advisors and investors should consider hiring an experienced manager who can allocate capital based on the attractiveness of the various sectors and underlying investments. To learn more, please visit https://www.franklintempleton.com/investments/capabilities/alternatives and alternativesbyft.com.

Copyright © Franklin Templeton Institute