by Carl R. Tannenbaum, Ryan James Boyle, Vaibhav Tandon, Northern Trust

We review the key themes of the first half of a busy year.

Editor’s Note: We take this opportunity to reflect on six themes that have defined an eventful first half of the year.

Stress Test

Monetary policy across developed countries has been tightening for more than a year. Careful foreshadowing by central banks has been designed to limit any dislocation. For a long time, the regime change for interest rates seemed to be well managed.

And then came the Ides of March. Silicon Valley Bank (SVB) failed suddenly and dramatically, precipitating a period of high anxiety that blanketed the global financial system. The headlines have calmed, but concerns about latent vulnerabilities remain.

Lessons have been learned. Institutions should have been better prepared for rising interest rates, hedging their risks and ensuring appropriate liquidity. Financial supervisors should have been more proactive and forceful. Management teams, their boards of directors and investors should have asked more questions, sooner.

But the overarching lesson of this year’s banking stress is one that has been offered a number of times in the past. Finance is built on trust, which can take a long time to establish but only moments to lose. The psychological reaction that attends the loss of confidence is powerful; in the current day, its expression is accelerated by modern communications and banking platforms.

The consequences of the SVB failure were indiscriminate. Mental linkages formed between organizations that are fundamentally different, casting doubt on all of them. The whole of the financial services industry suffered for the sins of a few.

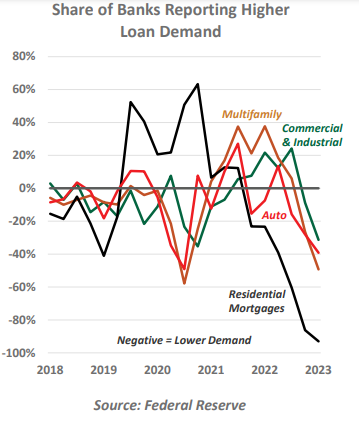

Banks whose share prices and deposits are in doubt react by restricting credit, which slows economic activity. The degree of restraint hinges on how dependent borrowers are on banks. Overall loan demand has been soft, but certain sectors in certain places rely more heavily on banks; office real estate credit has become an acute focus. This degree of potential restraint has been actively debated during recent central bank meetings and may have contributed to the Federal Reserve’s decision to pause its tightening program earlier this month.

Interest rates are a poor tool for managing financial instability, but “macroprudential” policy has once again proven to work better in theory than in practice. A period of re-regulation is underway, but may raise costs without solving problems. The question of more banks or fewer is receiving renewed attention.

Inflation is still too high, and central banks have suggested that their jobs are not done. Each increment of tightening risks another round of distress. Some have suggested that monetary authorities will keep the pressure on until something breaks. We’ll need to be on the lookout for new cracks in the financial system during the second half of the year.

Fiscal Drag

While central banks have been making concerted efforts to tame price pressures, there is also a growing realization that monetary policy alone may not be enough to control inflation. Fiscal policy will also play an important role.

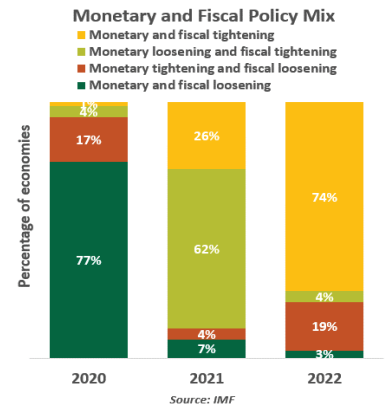

Consequently, governments have been tightening their purse strings to prevent further overheating of the economy that can drive prices higher. The fiscal impulse has turned contractionary in most economies. Following a surge in the first year of the pandemic from massive government support, both public debt and deficits have declined, as support measures have come to an end. Nearly 75% of countries tightened both fiscal and monetary policies in 2022. With strong nominal GDP growth in the past two years, global debt posted the steepest decline in seven decades of almost eight percentage points to 92% of GDP at the end of 2022. On average, fiscal deficits nearly halved from 2020 levels to 4.7% of GDP last year.

Nearly all COVID-era support measures have sunset in the U.S. Talks are underway in the European Union on reforming or reverting to the fiscal rules defined under the Stability and Growth Pact. The U.K. government is on track toward a more responsible fiscal trajectory. Governments are facing a complicated mandate of restraining debt and spending while avoiding recession.

That said, both debt and deficits remain elevated and are expected to go up this year. Rising interest payments and pressures to boost public spending on wages and pensions amid high inflation will partially reverse the recent improvement in public finances. Policymakers, especially in Europe, remain under pressure to provide targeted support measures to cap rising prices and protect purchasing power. Germany introduced a subsidized ticket for public transport at the start of May, while major retailers in France agreed to a policy of keeping prices of essential food items at the lowest level possible.

Responses from various governments during COVID has reminded us how fiscal policy can be a strong source of resilience. History is also full of instances of large public account imbalances quickly becoming a source of political and economic instability.

Stuck-flation

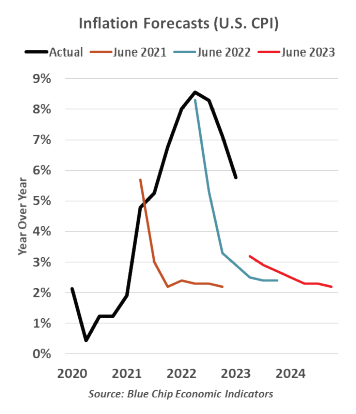

Asked about “transitory” inflation in testimony before the Senate Banking Committee in November 2021, Fed Chair Jerome Powell stated “it’s time to retire that word.” Eighteen months later, “transitory” has become a punchline more than an inflation expectation.

Inflation this year has improved to varying extents around the world. However, much of last year’s runup was driven by spiking energy and food prices, tying back to the Ukraine War and other idiosyncratic shocks. Countries more exposed to trade with Russia and Ukraine are experiencing a slower recovery. Even in the U.S., this year’s better inflation readings are still far too high for comfort. Excluding food and energy, the core Consumer Price Index (CPI) most recently showed a 5.3% annual gain, an insufficient improvement from its peak of 6.6% last September.

This cycle has taught a new generation the key risk around inflation: once it takes off, it spreads uncontrollably and is difficult to rein in. Most categories of goods and services have had a turn surprising to the upside. Forecasters and policymakers have been persistently disappointed by actual readings holding higher than expectations.

Hope remains for an inflation improvement ahead. Wage gains, though historically elevated, have not kept pace with inflation in this cycle. While the lack of a wage-price spiral thus far is a positive omen, many households are falling behind on a real basis. For better or worse, slower consumer demand will help to temper prices.

Behavioral economics teaches us the concept of recency bias: taking our most recent experience as a baseline expectation, regardless of its similarity. Tying our expectations to the old norms of inflation has made the current cycle especially shocking. From 1995 to 2020, the U.S. never saw core CPI reach 3%; we could rationally disregard inflation for years at a time. But as high readings drag on, the old norm of low, forgettable inflation may become a more distant memory.

Rolling Recession

Everyone knows the moment they have caught the common cold, with an ill feeling in the upper respiratory tract signaling a bad week ahead. And most of us know that recessions have familiar omens at their onset: deferred projects, hiring freezes, curtailed hours, layoffs. As we track the broad economy, we don’t see much evidence of a recession in the aggregate, national indicators. But readers may recognize those symptoms in their own lines of work. The recession is rolling across each sector in due course.

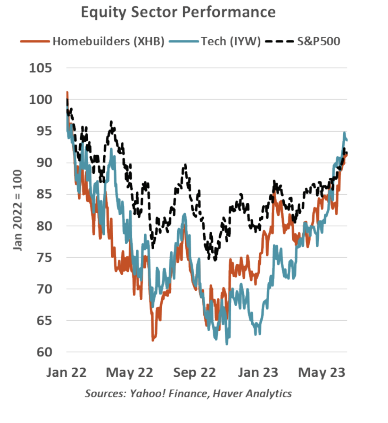

Examples abound. An early victim was the auto sector. As the reopening surge lifted demand for durable goods, automakers were unable to finish vehicles and get them to dealers. Today, as supply chains heal, pent-up demand is supporting automakers. A year ago, homebuilders feared that rising interest rates would be fatal to their sales prospects; today, they report steady demand. Large technology firms faced a reckoning last year, and their layoff announcements were well-publicized; since March, tech firms have led this year’s market rally.

The good news about recessions is that they are temporary. Sooner or later, demand returns and employers grow again. For sectors that struggled in the COVID recovery, the bad times have ended relatively quickly. As challenges spread—most recently, to the freight and financial sectors—we take these examples as hopeful illustrations that the sun also rises.

But this is not to make light of real job losses and earnings constraints; even a short setback can cause lasting damage and economic scarring. A rolling recession gives hope that a bad interval will be short-lived. The greatest risk is that the recession rolls to too many sectors at once, and the entire economy falls into contraction.

Opening Cracks

Major Western economies have expanded this year, defying expectations of recession. Tighter monetary and fiscal policy will make it difficult to sustain momentum during the second half.

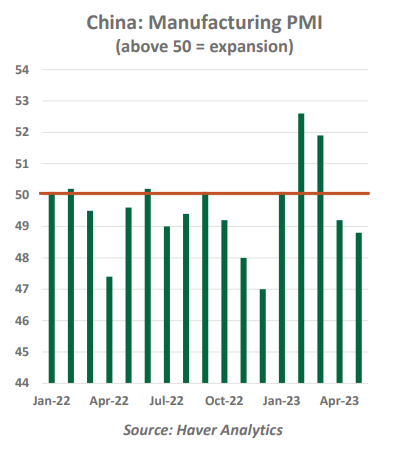

China, emerging from its fight against COVID-19, is being counted on to take the baton and lead global growth. But a visit to Beijing in early May suggested that expectations of a powerful Chinese reopening may be greatly exaggerated.

The Chinese populace is trying to re-define normalcy after two and a half years in lockdown followed by months of viral contagion. Property market declines have diminished household net worth. The mood among Chinese consumers is anything but ebullient.

Chinese manufacturers are facing sluggish export demand and intensifying efforts by countries and companies to re-shore production. Chinese technology firms face further headwinds from expanding restrictions on transfers of equipment and intellectual property, as Western providers seek the mantle of leadership for next-generation hardware and software. Recent readings show China’s heavy industries have fallen back into decline.

Economic policymakers in China have implemented new rounds of stimulus to boost demand. China has also steered away from a fulsome embrace of Russia in its conflict with Ukraine, aware that full support would prompt restrictive sanctions from the West. The commercial consequences of such measures would be immense.

China’s enthusiasm is also being tempered by what lies on the horizon. Its demographic profile is among the worst in the world, as is its carbon footprint. Both of these challenges will bear heavily on China’s economic prospects over the coming decades.

Beijing’s ability to navigate near-term and long-term challenges will be critical not only for its own fortunes, but also for those of its neighbors. The economic ecosystem in southeast Asia has brought heightened prosperity to many nations and enabled them to manage high levels of government debt. Any loss of momentum would be collectively and individually costly.

Developing nations often fall into a “middle income trap,” which sees their growth rates diminish after a long period of outperformance. China has seemingly defied this law of economic gravity, but the aftermath of COVID-19 may bring the Chinese economy back down to earth.

Booster Dose

Artificial intelligence (AI) has taken the world by storm in the last few years, from voice assistants to advancements in analytics. Recent progress in generative AI added to the buzz, as the tangible gain makes it easier to envision changes to the way we live and work.

AI is seen as an engine of productivity and economic growth. Firms are rapidly adopting the technology for its ability to improve efficiency. The world has been waiting for a productivity surge linked to innovations of the past two decades. Now, that boost could finally arrive with artificial intelligence. According to Goldman Sachs, AI has the potential to drive a 7% or almost $7 trillion increase in annual global GDP over the next decade. Various academic studies have estimated up to a three percentage point boost to labor productivity growth from adoption of AI.

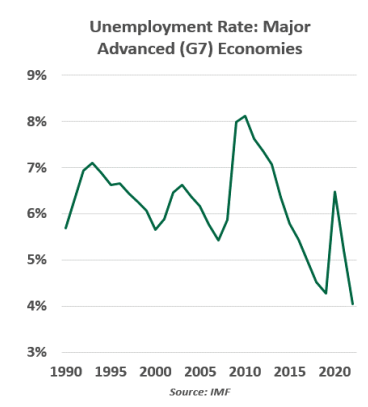

The use of AI presents many opportunities, but has also prompted anxiety that large-scale job losses are imminent. These concerns echo past worries about innovations like computing and robotics. In retrospect, the scale of actual dislocation was overestimated. Over the past decade, unemployment rates in advanced economies have roughly halved, and the share of working-age people in employment is at an all-time high. Economies with the highest rates of automation and robotics, such as Japan and Singapore, have among the lowest unemployment rates. A study by the U.S. Bureau of Labor Statistics found that in recent years, occupations classified as at risk from new technologies “did not exhibit any general tendency toward notably rapid job loss”.

While some dislocation is imminent from the technological shift, it is also likely that automation of certain tasks simply alters the composition of jobs. Historically, jobs displaced by modernization have been offset by the creation of new occupations. But concerns of AI having a disruptive effect on the economy and society cannot be ignored. Challenges pertaining to privacy, legal or financial risk and behavioral manipulation must be addressed as the technology matures.

Governments need to foster advancement and innovation in AI while protecting employees and consumers from the disruptions that could arise. Without proper oversight, the potential for transformative change is unlikely to be fully realized.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

Copyright © Northern Trust