by Vaibhav Tandon, Senior Economist, Northern Trust

Volatile input prices have been a major inflationary force.

The efficient market hypothesis, endorsed by prominent economists like Friedrich Hayek and Milton Friedman, argues that asset prices immediately reflect all available information about the supply and demand of a given asset.

This conventional wisdom or economic orthodoxy has often been put to the test. However, the large, sustained gains followed by declines in commodities since the onset of COVID has only restored confidence in the markets’ ability to price in risks.

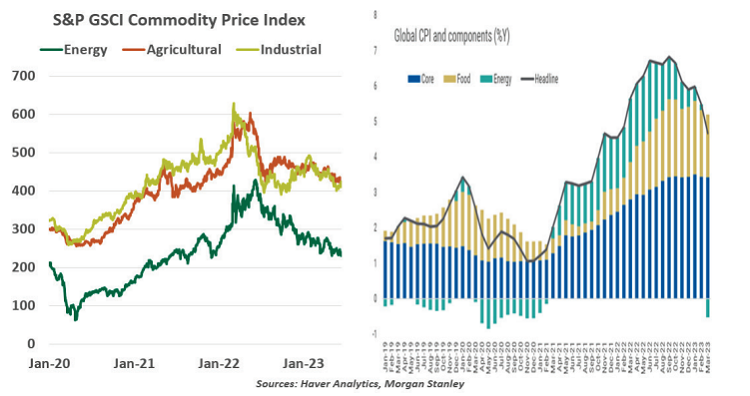

In the early days of the pandemic, demand plummeted amid the first wave of stringent lockdowns. Prices of commodities ranging from food to energy to industrial metals fell sharply. But as the world started to co-exist with the virus and demand recovered, supply remained disrupted, causing a surge in global commodity prices. The Ukraine war added to the demand-supply mismatch, with Russia being a major supplier of commodities like oil, gas, fertilizer and food, propelling prices even higher. Elevated commodity costs, particularly energy and food, have been the key driver of the global inflation surge.

With the euphoria from economic reopening and supply disruptions fading, prices of commodities have retreated substantially from their recent peaks. The World Bank’s Global Commodity Price Index fell 14% in the first quarter of 2023. By March month-end, they were about 30% below their historic peak in June 2022. From copper to wheat to natural gas, prices of most of the world’s important commodities have corrected sharply. The European natural gas price benchmark plunged by 80% from its peak in August 2022.

Aiming to push up stubbornly low oil prices, the Organization of the Petroleum Exporting Countries+ decided to prolong production cuts into 2024. In July, Saudi Arabia will decrease its production by one million barrels per day with the option to extend the cut. Yet, prices have barely budged, and Brent continues to trade around its May level.

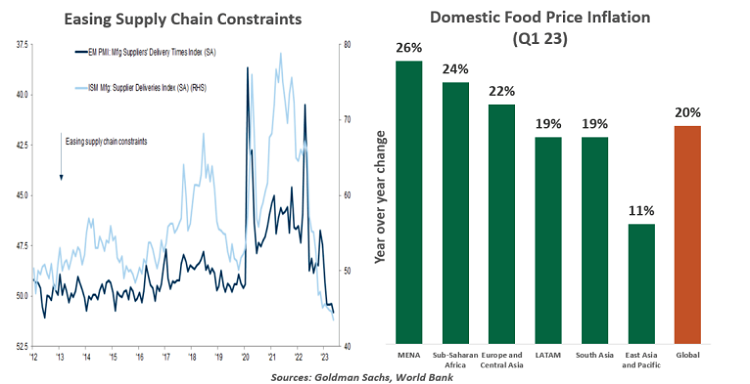

Both demand- and supply-side factors have contributed to easing commodity prices. The decline in prices reflects a combination of weaker economic activity, a relatively mild winter and a reallocation of commodity trade flows. Supply chain snarls have eased from their pandemic peaks. European natural gas prices have declined amid weaker demand on account of the milder winter, healthy inventories and intensive efforts to increase energy efficiency and conservation.

Forecasters have been trimming their base metal price expectations following the sizeable correction in the month of May amid signs that China is struggling to maintain its reopening momentum. The renewal of the Black Sea grain deal has helped stabilize supplies, especially of corn and wheat, which registered sizeable declines in price last month. High energy prices also feed into transportation and fertilizers for food production. As a result, lower transport and production costs coupled with better harvests in major grain-producing nations have pushed prices of agricultural commodities down, well below the peaks seen last year.

Energy and food commodities account for a significant share of consumer expenditures, especially in emerging markets, with a quick and large pass-through to the headline consumer price index (CPI). They represent up to 30% of the CPI basket in developed regions like North America and Europe and half or more in many developing nations. According to the Bank for International Settlements, a 10% rise in the price of oil lifts year over year inflation 0.2 percentage points across importers and exporters; agricultural commodity price rises are twice as inflationary. Plus, the impact of higher commodity prices is not confined to energy and food. Core inflation also rises for the many categories that take commodities as inputs, complicating central banks’ efforts to meet their inflation targets.

Since last year’s peaks, commodities have progressed from a cause of inflation to a source of relief for households and businesses that were stung by soaring costs. Energy inflation in the U.S has dropped from 41% year over year last June to -11% in May 2023. In Europe, the energy component has entered a deflationary zone and is set to become a bigger drag in the second half of the year, even if energy costs remain flat or increase slightly. Inflation in the core goods component, excluding food and energy products, has been decelerating on the back of lower input costs. Core inflation is proving to be stickier than expected, primarily due to services. However, lower headline inflation from falling commodity costs will condense the second-order effects, tone down demand for higher wages and stabilize inflation expectations.

Domestic food prices remain a key concern in many major and small economies, exerting upward pressure on inflation. It is the largest contributor to the level of the headline consumer price index (CPI) in Europe. Higher food prices are pushing millions into food insecurity, especially in poorer countries. The World Food Program estimates that 345 million people in almost 80 countries will face acute food insecurity this year, more than double the number in the first year of COVID. With global food indices trending down over the past year, we are hopeful of a pass-through to consumer prices in the coming months.

That said, a host of factors could reignite inflationary pressures. We are mindful of the tighter oil supply, a commodity-intensive rebound in China, higher geopolitical tensions, trade restrictions and the risk of unfavorable weather conditions from the emerging El Niño. Prices of several commodities are still above their pre-COVID levels. With no clear path to a resolution of the Ukraine war, an escalation could easily disrupt the flow of agriculture commodities.

Amid so many exogenous shocks and whipsawing demand and supply, commodity prices have been highly volatile. Putting a value on so many risks has put the efficient market hypothesis to the test. Today’s lower, steadier prices are a welcome reprieve from last year’s price pressures, and we hope they set the stage for calmer times to come.

Copyright © Northern Trust

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions. © 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.