by Tony Davidow, CIMA®, Senior Alternatives Investment Strategist, Franklin Templeton Institute

Secondary funds, commonly referred to as secondaries or continuation transactions, purchase existing interests from limited partners (LPs) or assets from primary private equity fund investors. Although once considered a niche strategy, secondaries have matured and now represent a vital cog in the private equity ecosystem, according to Franklin Templeton Institute’s Tony Davidow. Read more:

In a traditional private equity fund, a pension plan, endowment, foundation or family office (a privately held company that handles investment and wealth management for a wealthy family) commits to invest capital over a period of time (seven-10 years). They are considered limited partners in the fund (LPs). When the fund manager, also known as the general partner (GP), finds an attractive investment, they call for capital from the LPs’ (capital calls) original commitment.

The LPs understand that these are long-term investments, but sometimes they have liquidity needs, and they may seek a buyer for their ownership stake. These are referred to as secondaries transactions since the original owner seeks a secondary buyer.

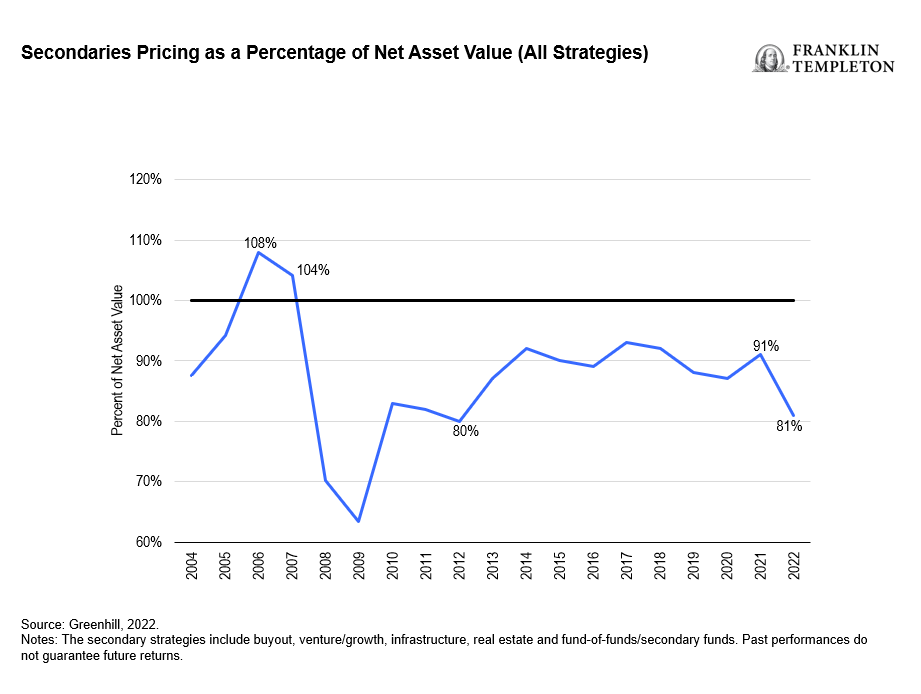

As the data above illustrates, secondaries have traded at a discount to net asset value (NAV) since 2007, with more attractive pricing during periods of economic slowdowns. This is partially driven by the “denominator effect,” as public pension funds find themselves overallocated to alternative investments due to the decline in value of their public market positions. As institutional investors reduce or diversify their private equity, new investors have the ability to benefit through participating in secondaries and purchasing these positions at discounts.

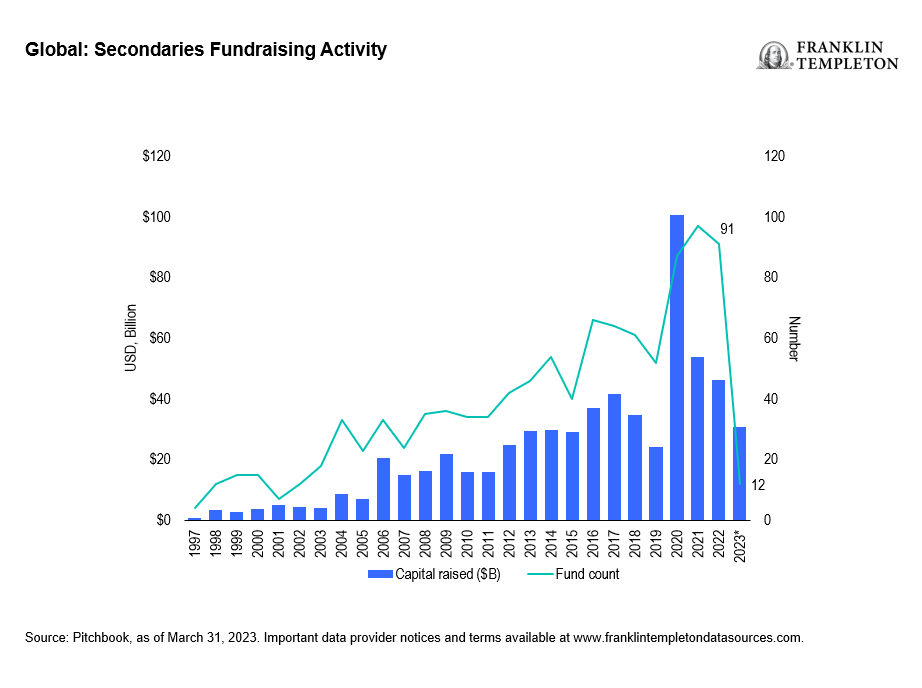

According to PitchBook,1 secondaries fundraising rose from US$20 billion in 2006, to US$100 billion in 2020. Up until 2022, most funds could exit their investments through acquisitions or initial public offerings (IPOs). This created a lot of cash flow and liquidity for LPs. In 2022, exits began to slow dramatically, and have essentially dried-up since the collapse of Silicon Valley Bank. LPs will likely need some liquidity in the coming years to meet capital calls and diversify their holdings.

Secondaries managers can diversify their holdings based on the stages, geography, industry and vintage of the primary funds available. By diversifying vintage years, the secondaries manager can attempt to mitigate the J-Curve effect, where capital is drawn down as opportunities are sourced and returns are typically negative. Secondaries managers with experience and capital to deploy may be able to take advantage of the current market and find many attractive opportunities in the coming years.

In today’s market environment, with exits slowing dramatically from peak levels, we anticipate that many institutions and family offices will seek liquidity in the near future. We believe this scenario provides a significant opportunity for secondaries managers to select highly prized assets from a diverse pool and negotiate favorable pricing.

WHAT ARE THE RISKS?

All investments involve risks, including the possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Bond prices generally move in the opposite direction of interest rates. Thus, as prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline.

Investing in private companies involves a number of significant risks, including that they: may have limited financial resources and may be unable to meet their obligations under their debt securities, which may be accompanied by a deterioration in the value of any collateral and a reduction in the likelihood of realizing any guarantees that may have obtained in connection with the investment; have shorter operating histories, narrower product lines and smaller market shares than larger businesses, which tend to render them more vulnerable to competitors’ actions and changing market conditions, as well as general economic downturns; are more likely to depend on the management talents and efforts of a small group of persons; therefore, the death, disability, resignation or termination of one or more of these persons could have a material adverse impact on the portfolio company and, in turn, on the investment; generally have less predictable operating results, may from time to time be parties to litigation, may be engaged in rapidly changing businesses with products subject to a substantial risk of obsolescence, and may require substantial additional capital to support their operations, finance expansion or maintain their competitive position.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.