by Ryan James Boyle, Senior Economist, Northern Trust

The 2011 U.S. reality television show Doomsday Preppers showed an uncommon side of life, spotlighting families that prepared to survive extreme, potentially fatal scenarios. Their plans included accumulating a surplus of food, fuel, and other essentials, all of which came at a cost.

By contrast, most households and businesses carry just enough supplies to go about their routines, assuming more will always be available. The pandemic and its ensuing disruptions drew down stocks; rebuilding and holding the appropriate level of inventories has been a challenge ever since.

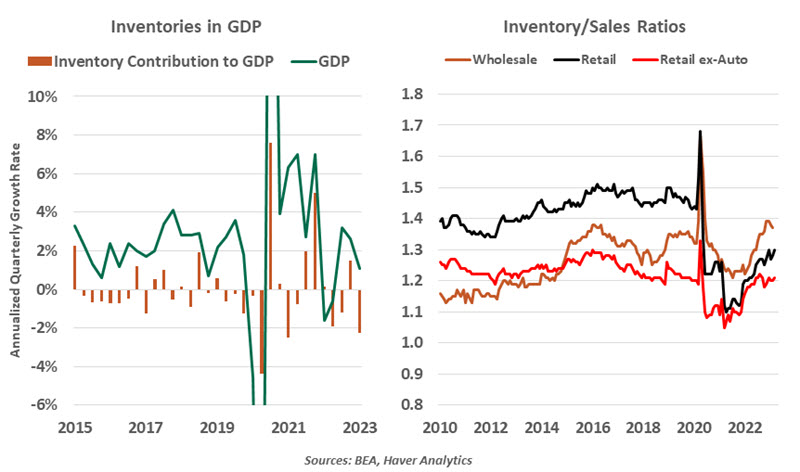

Private inventory growth is an important component of gross domestic product (GDP). Businesses adding to their inventories raises production levels and lifts overall GDP. Uniquely among GDP components, inventories are calculated using their second derivative, or how quickly their levels change. If inventories grow at a faster pace than they did in the prior quarter, GDP increases. Conversely, if the pace of growth is slower (even if still positive), GDP decreases.

The inventory calculation is fresh on our minds after a surprise in the first quarter reading of GDP. The level of inventories was essentially flat, falling by $1.6 billion quarter over quarter, a trivial change to a stock of nearly $3 trillion. However, this was a massive decline from the prior quarter’s growth of $137 billion. That stark difference caused inventories to subtract 2.3 percentage points from the overall rate of growth, leading to the lackluster headline real growth rate of 1.1%.

The approach to assessing inventories means they will always be a volatile component of GDP. Our concern is focused on whether they are poised to be a continued drag in coming quarters, or if they can contribute to a soft landing.

Inventories are an unpredictable component of GDP.

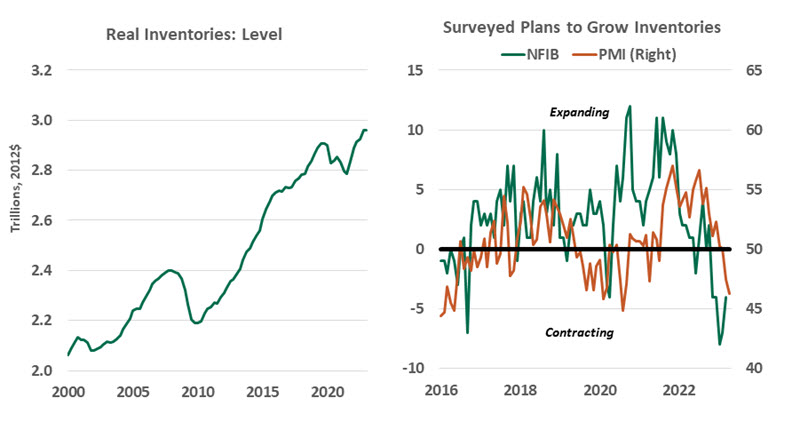

The other GDP components offer some reasons for optimism. First quarter consumption growth of 3.7% was the best rate seen since the reopening surge of 2021. Consumers are still spending; an inventory draw-down cannot last long in the face of steady demand. Adjusted for inflation, the overall stock of private inventories stands only 1.7% above its level observed at the end of 2019, while the overall economy has grown 5.3%. Put simply, there is still margin for inventory growth.

Auto inventories are especially low. The Bureau of Economic Analysis reports that stocks of domestically-produced autos stand 77% below their level at the end of 2019, while Ward’s reports a 39% decline in inventories of trucks. Perhaps the pre-pandemic business model left dealers oversupplied, but some recovery of inventories still seems plausible.

But there are reasons to doubt inventories will provide an enduring boost to output. The rebuilding phase is over; the pandemic supply crunch taught many businesses how to do more with less, and some of those lessons may endure. For five months in a row, the majority of small business owners surveyed by the National Federation of Independent Business (NFIB) indicate they plan to reduce inventories; the inventory component of the manufacturing Purchasing Managers’ Index (PMI) has also fallen into contraction.

Higher inventories can help insure against supply chain disruptions.

Further up the value chain, most wholesalers and manufacturers report they have sufficient supplies to conduct operations. Movements of goods are down, with the transportation sector signaling a “freight recession” is underway. These indicators are consistent with an overall expectation of slow growth for this year: amid uncertain sales prospects, managers are hesitant to commit to higher inventories.

On balance, my mind returns to the preppers. Black swan events since 2020—the pandemic, Ukraine invasion and rampant inflation—derailed many well-considered plans. Those who gave advance thought to outlier outcomes fared best. As businesses evaluate the risk in supply chains and value of resiliency, the case for larger inventories gets stronger. It may not make for exciting television, but a little more preparation can be the key to continued growth.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.