by Tony DeSpirito, CIO of U.S. Fundamental Equities, Blackrock

Stock returns have been driven by macroeconomic dynamics for over a year. Active investor Tony DeSpirito sees opportunity in focusing on the micro, or stock specifics, and prepares for fundamentals to reassert their importance.

When markets are in a tailspin, and an extended one at that, it can be hard to see beyond the immediate stresses. Macroeconomic dynamics, such as the highest inflation in decades and the fastest and most dramatic rate-hiking cycle since the 1980s, have been driving financial market returns for over a year ― and the portfolio pain has been far reaching.

As active stock pickers, we apply a “bottom-up” approach to look at underlying company fundamentals first, then expand our analysis to factor the bigger picture into our stock-selection process. We test our convictions from the top down as well, assessing how broader economic changes may potentially filter down to affect sectors, industries and companies. This is especially important as Fed actions, and the related macro reverberations, have mattered more.

This macro-driven phase may have further to go, yet we do expect attention to eventually turn to how individual companies are able to navigate a new environment of higher inflation and rates. We believe this is meaningful to long-term investors for several reasons:

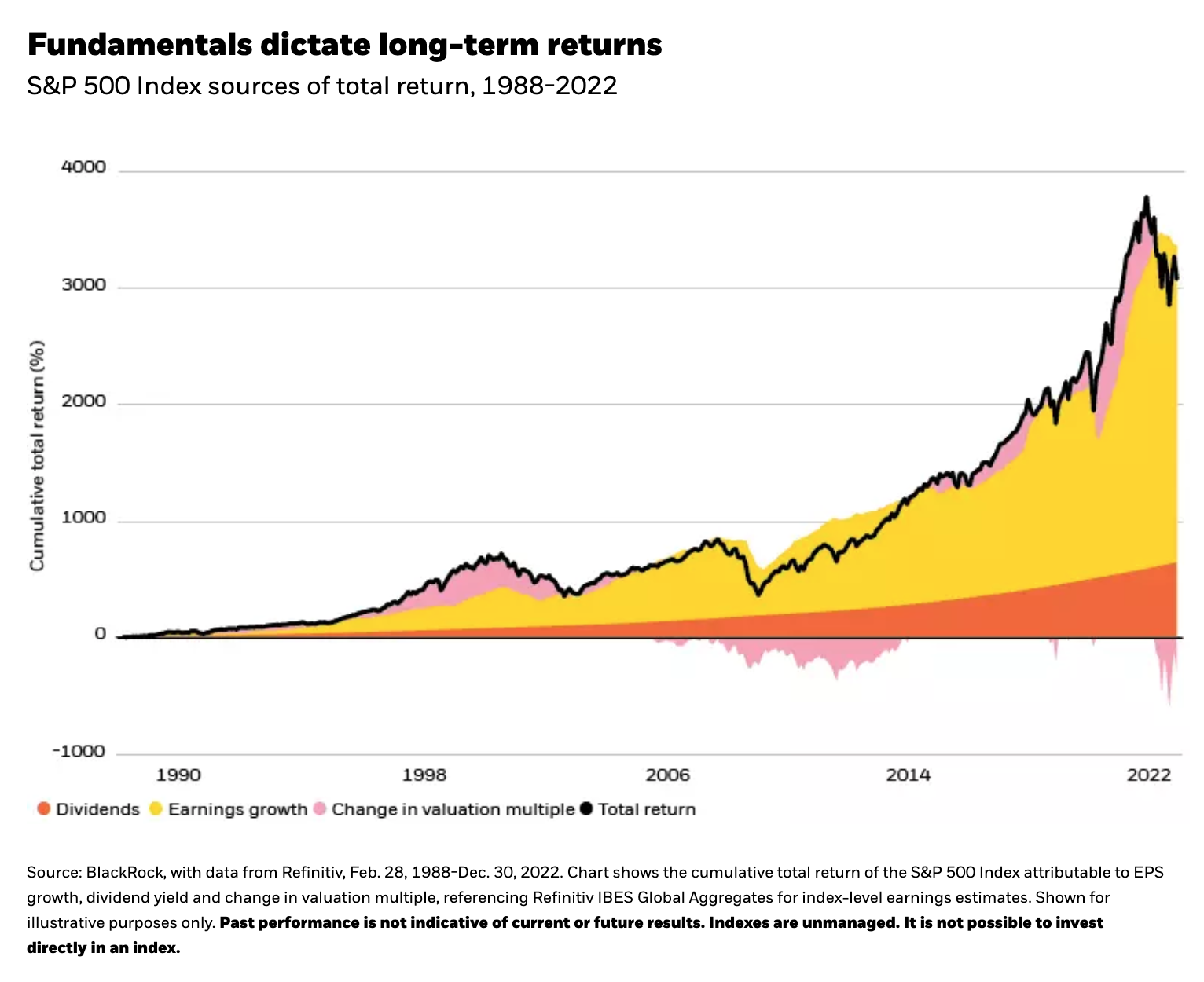

The micro matters more across time

As we discuss in our latest equity market outlook, macroeconomic influences can have an outsized impact on stock returns in the short run. Yet companies’ underlying fundamentals ― things like revenue, profitability, cash flow, assets and liabilities ― are the key determinants of stock returns across time. These are evidenced in a company’s earnings, the key contributor to total return, as shown in the chart below.

Companies that compound their earnings by reinvesting them into revenue growth, margin improvement or share count reduction are effectively compounding returns to shareholders. Even as uncertainty clouds the big picture, we believe companies that can maintain their earnings growth throughout market cycles will remain highly prized and their fundamental strength will be appropriately priced.

Stock price is more volatile than company fundamentals

A company’s stock price will change more frequently than its fundamentals. This is because, as we’ve recently seen, short-term price changes can be driven by external factors including monetary and fiscal policy influences, macro shocks, natural disasters or even demographic or technology changes.

When this happens, the stock price may be rendered incongruent with the company’s underlying worth based on its fundamentals. Often, this can represent a buying opportunity. If you believe in a company’s business model and long-term prospects, market pullbacks can present opportunities to buy shares at attractive prices. Over time, as illustrated above, stock prices will reflect fundamentals and reward investors accordingly.

Economies are not stock markets

Finally, it’s worth noting that economies are not markets and, as such, the fate of one does not offer a direct read-through to the other. Whereas economic data is backward-looking by its nature, the stock market is an anticipatory mechanism that looks to price the future prospects of companies.

Consider an investor who sold out of the world’s e-commerce giant on recession fears at the start of 2008, just as the Global Financial Crisis was gripping markets, and never re-established a position. That investor would have missed out on an eye-popping 2,130% return through March 31, 2023.* The company’s stock price was temporarily punished in the broad market downturn, but its underlying business model and fundamentals were sound, and this was acknowledged and rewarded across time.

The stock market has historically anticipated (and priced company shares for) improving economic conditions before they arrive. This makes market timing extremely difficult and reinforces the wisdom in weathering the downturns ― and allowing company fundamentals to do what they have historically done and guide stocks to their next destination.

*****

Tony DeSpirito, BlackRock Fundamental Equities,

Antonio (Tony) DeSpirito, Managing Director, is Chief Investment Officer of U.S. Fundamental Equities. He is also lead portfolio manager of the BlackRock Equity Dividend and value portfolios.

Copyright © Blackrock