by Tony DeSpirito, CIO of U.S. Fundamental Equities, Blackrock

Key takeaways

Between stocks and a hard place. The first quarter packed a full gamut of investor emotion, as early cheer gave way to fears over stubbornly high inflation and fallout from Fed rate hikes. As Q2 begins, we see:

- Equities maintaining their long-term appeal

- Returns increasingly driven by stock specifics

- A need to emphasize quality and stability

Equity market overview and outlook

An early-year stock rally fueled by hopes of a Fed pause proved short-lived. The first spoiler ― hotter-than-expected inflation data ― was followed by signs that rate hikes are having an economic impact as cracks emerged in the banking system. The two counterforces make the Fed’s job more complicated as it becomes increasingly clear that taming inflation might not only incite recession but could also rock financial stability.

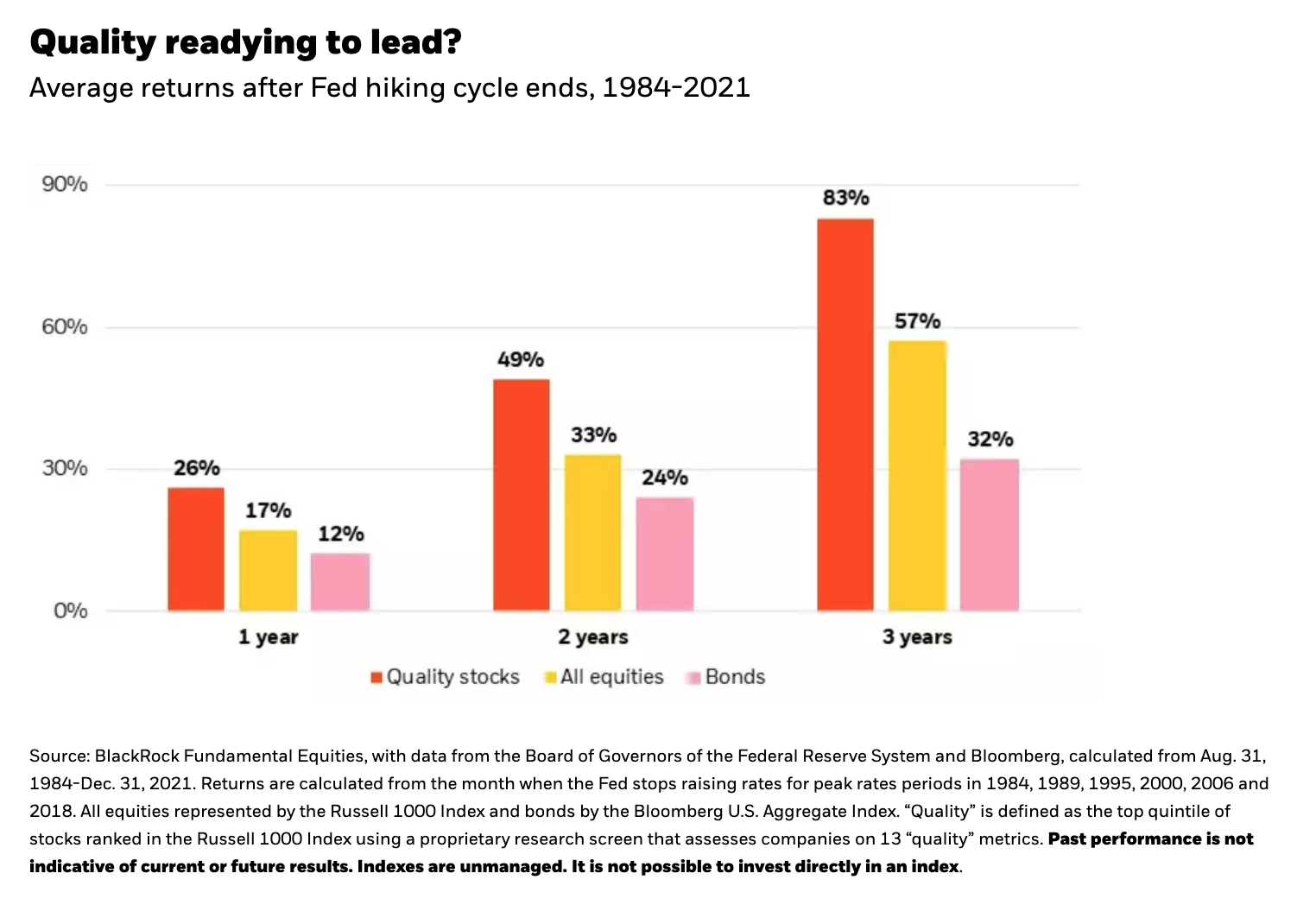

We remain selective in taking risk as macro factors continue to drive sentiment, but we do expect company specifics to grab the reins as the driver of returns once greater clarity emerges around inflation and the economy. Despite the uncertainties, investors should not lose sight of equities’ enduring role in a well-balanced portfolio. We advocate a near-term focus on resilience via quality stocks, which historically have outperformed both the broad market and bonds in the one to three years after the Fed stops hiking rates, as shown below.

Sticking with stocks

In a historically rare occurrence, both stocks and bonds delivered negative returns in 2022. The consensus view is that bonds now offer the best opportunity to invest at attractive prices since the global financial crisis (GFC). Yet stocks continue to play a critical role in a long-term investment plan and their “expensiveness” is partly a question of time horizon.

Perspective on price

A look at the equity risk premium (ERP) across nearly seven decades of data indicates current pricing is a fairly balanced proposition between the two assets ― with equities historically offering better long-term returns.

The ERP is a gauge of the relative risk-reward in stocks versus bonds, measuring stocks’ excess earnings yield over the “risk-free” rate. The ERP dropped recently after being abnormally elevated for 13 years as Treasury yields hovered near historic lows. Yet the S&P 500’s current ERP of 1.71% is still above the 1.62% average since the index’s inception in 1957.* This suggests that stock pricing relative to bonds is still slightly better than historical averages.

Perspective on performance

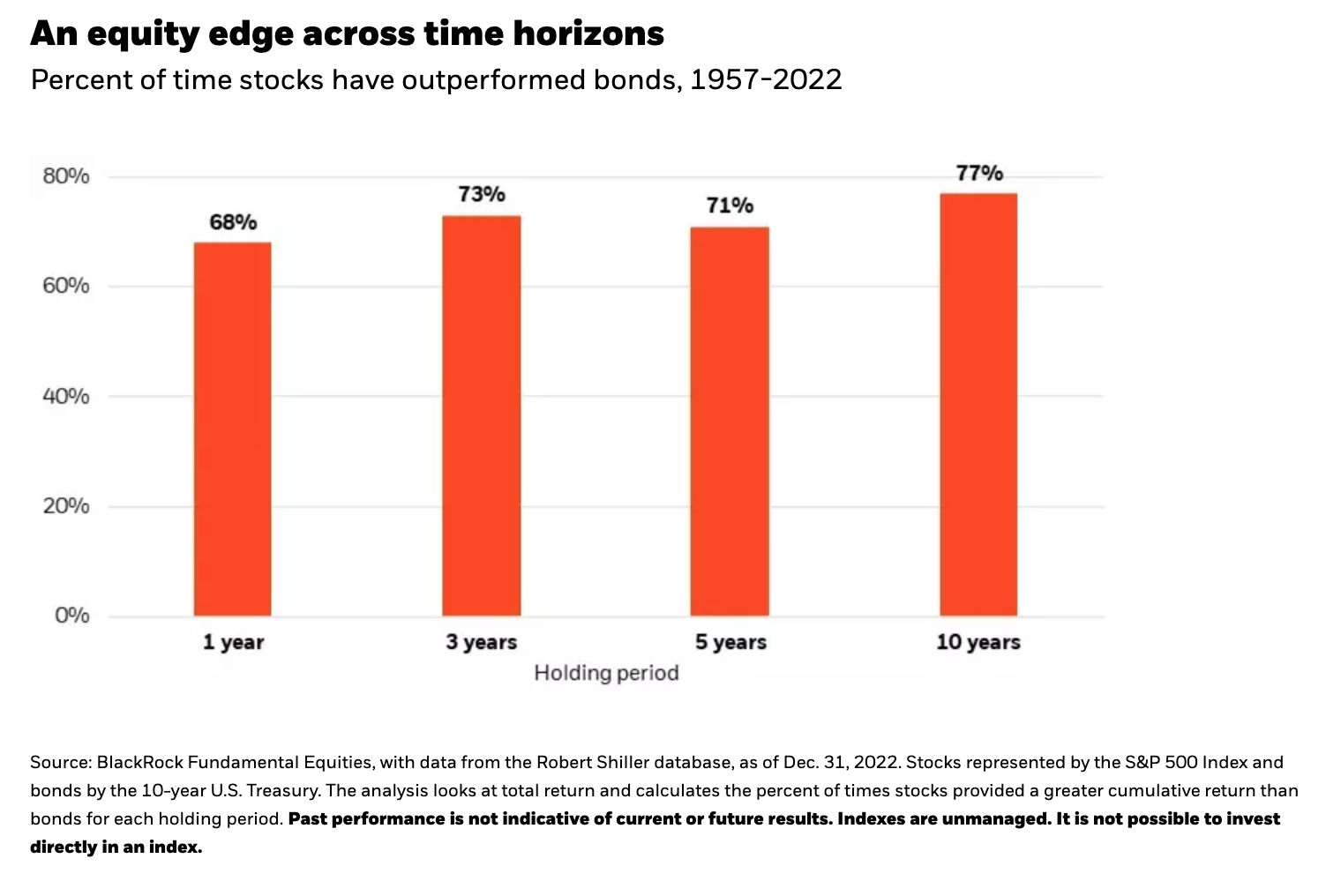

Equities entail greater risk for their potential greater reward and are broadly expected to outperform bonds, which have lower volatility, over time. As the chart below shows, equities have even provided a more favorable performance outcome over shorter time frames, besting bonds 68% of the time over one-year holding periods.

Actively keying in on quality

With recession a looming concern, investors understandably gravitate to the lower-risk asset. But equities are a critical long-term growth engine and can be built into portfolios with a focus on resilience. We believe this is best achieved through active selection with an emphasis on “quality” characteristics. Our Fundamental Equities portfolio management teams are adding quality through stock selection that emphasizes:

1. Earnings compounders

In the short run, macroeconomic influences can have an outsized impact on stock returns. This has been painfully evident in the past year amid high inflation and Fed rate hikes. Yet companies’ underlying fundamentals are responsible for the lion’s share of stock returns across time, and earnings growth is a dominant contributor.

We seek companies that can maintain their earnings growth throughout market cycles. Those that compound their earnings by reinvesting them into revenue growth, margin improvement or share count reduction are effectively compounding returns to shareholders. We look for solid balance sheets and positive free cash flow (essentially a buffer against any shortfalls) as additional key signposts.

2. Dividend growers

Dividend-paying stocks have outperformed non-dividend payers over the long term with less volatility, but companies that grow their dividends stand out most. Statistically, a company’s record of and commitment to paying a dividend has instilled a measure of resilience. We find their managements are loathe to cut a dividend and send a negative signal to the market, so dividend growers tend to be well-run companies built to weather diverse markets. Stocks with a history of dividend growth also have tended to fare better in a rising-rate environment versus the highest-yielding stocks (essentially “bond proxies”) that tend to follow bond prices down as rates rise.

3. Stability sectors

Healthcare was a favored stability sector across our global Fundamental Equities platform last year and remains so today. Company earnings in the healthcare sector have historically proved to be recession resilient, and we would expect that precedent to hold in the next recession. This is important in a year in which stock performance is more likely to be driven by earnings, versus last year when returns were driven by multiple contraction.

Pricing for healthcare stocks is compelling, with valuations below the market average. Other defensive sectors such as consumer staples and utilities were bid up in price last year as investors sought stability, and staples’ valuations still sit above the broad market. Healthcare also boasts a long-term tailwind as aging populations and increasing health-related needs worldwide set the stage for attractive growth prospects across the sector.

We see each of the above expressions of quality gaining in importance in 2023 as return outcomes rely less on broad market moves and more on individual selection.

Download full report

Copyright © Blackrock