Technical Notes

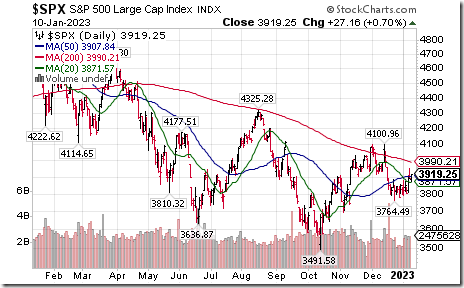

S&P 500 Index moved above its 20 and 50 day moving averages.

UnitedHealth Group $UNH a Dow Jones Industrial Average stock moved below $286.24 extending an intermediate downtrend.

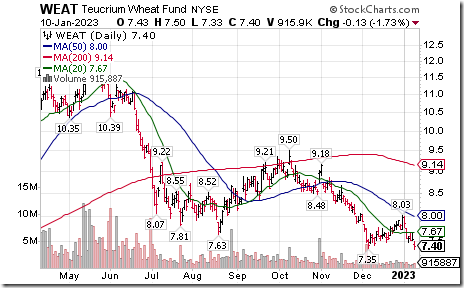

Wheat ETN $WEAT moved below $7.35 extending an intermediate downtrend.

Trader’s Corner

Equity Indices and Related ETFs

Daily Seasonal/Technical Equity Trends for January 10th 2023

Green: Increase from previous day

Red: Decrease from previous day

Commodities

Daily Seasonal/Technical Commodities Trends for January 10th 2023

Green: Increase from previous day

Red: Decrease from previous day

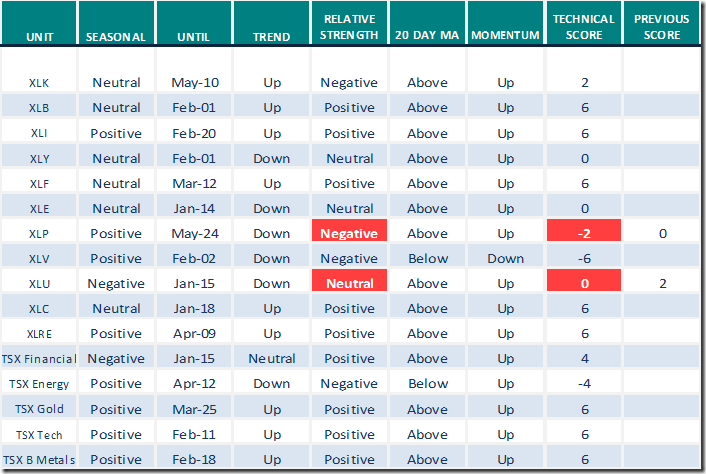

Sectors

Daily Seasonal/Technical Sector Trends for January 10th 2023

Green: Increase from previous day

Red: Decrease from previous day

Links offered by valued providers

John Kosar asks “Emerging markets Bottom: What to watch”.

Emerging Market Bottom? What To Watch | John Kosar, CMT | Your Daily Five (01.09.23) – YouTube

A note from Michael Campbell

“We are headed into a period of extreme volatility and geopolitical chaos for the first two quarters of 2023. So get ready.”

~ Martin Armstrong

The good news is that the world isn’t coming to an end but make no mistake – it is changing. Failing to understand the nature of those changes and failing to take action will be very costly. It already has been for anyone who didn’t appreciate that the reversal in the 12 year trend of accommodative fiscal and monetary policy that had propelled stock, bond and real estate prices to record highs occurred March 1, 2022.

We are no longer in a low inflation, low interest rate environment. A recession is likely, along with falling corporate earnings in a period of rising interest rates, which produced the biggest decline in the S&P 500 since 2008 with a loss of 18%.

Homeowners renewing their 5 year mortgages taken out in 2017 have seen their rates double while the bank rate jumped 1700% since March. With about half the outstanding 5 year mortgages coming due in the next two years many more people will feel the crunch.

As I said, the first step is to appreciate things have changed but here’s the thing I’ve noticed…

From the moment central banks declared their intention to raise rates in order to fight inflation the debate regarding when they’d stop and pivot began.

That suggests that a lot of people think the rate increases represent just a brief interlude in the major trend of declining rates and deficit spending that’s driven markets since the subprime credit crisis in 2008-09. I doubt they’re right. My bet is that the era of cheap money, cheap energy and cheap labour is over. And the consequences for both government and personal finances are profound, especially when coupled with the most precarious geopolitical environment in half a century along with record sovereign debt levels.

Whether we’re talking about massive problems in the UK pension system that required a central bank bail-out in late September or the massive intervention in the Japanese bond market – the financial stress in the system is obvious.

As we predicted at the World Outlook Financial Conference last year, 2022 would see the unusual situation of both stock and bond declines. That’s what happened. Yale economist Robert Schiller’s Index calculates that the performance of stocks and bonds was the worst since 1871.

The bottom line is that the first order of business is to protect yourself. It’s a defensive investment environment but that doesn’t mean there aren’t significant opportunities. That’s the focus on this year’s World Outlook Financial Conference to “survive and thrive.” It will be live and in person February 3rd and 4th at the Westin Bayshore in Vancouver.

It’s key to understand that what worked in the investment market in the last 12 years – e.g. leverage and aggressive growth – is not likely to yield similar results. But let me repeat, that’s doesn’t mean there aren’t opportunities, which the conference will explore with some of the top names in finance.

For the first time we will be joined by TG Macro founder Tony Greer, whose call on what he called the Great Rotation from tech stocks to energy and commodities through 2021 and into 2022 was as good as it gets. He’s out of tech but he’s also been on the sidelines for commodities since the 2nd quarter last year. He’ll tell us whether it’s time to pull the trigger on specific commodities at the Conference.

The Macro Tourist, Kevin Muir will also join us for the first time. Kevin correctly predicted the US markets dismal performance in 2022 and he’ll share why he thinks, “this is just the start of a trend that will see another year with American financial asset returns at the bottom of the pack.” And what to do instead.

The always thought provoking Martin Armstrong will join us to talk about geopolitical risk, sovereign debt and the impact on various markets. He’s always controversial but whether you like what he has to say or not, you can’t discount his model’s amazing track record of prediction. (By the way, his conference in November cost over $3,700 to attend.)

We’ll present our World Outlook Small Cap Portfolio with Keystone Financial’s Ryan Irvine and Aaron Dunn, which has never failed to yield double digit returns. Of course, that doesn’t guarantee future returns but I like our chances.

I won’t go on other than to say but that Greg Weldon will be there to talk about gold, silver and stocks. So will BT Global’s Paul Beattie who last year talked about his top 3 stocks to short – Peloton – ARC Innovation ETF and Rivian Automotive interactive. All big winners as they dropped 70% plus from their highs.

Wellington-Altus chief strategist James Thorne will be with us. At last year’s Conference he accurately forecast we’d head down into June, then recover only to decline further. He’ll give us his map for stocks in 2023 and 2024. Josef Schachter will also be there to explain why he thinks oil is setting up for the buy of a lifetime.

Finally, it’s a great weekend. Come and chat with the whole MoneyTalks team – Victor, Michael and Ozzie, who will tell us why he thinks the real estate market decline is the time to consider buying.

I‘m absolutely sincere when I say that I’d pay to hear the recommendations of any one of our analysts – let alone the whole group. I know what some of them get paid to privately consult for mutual funds, investment firms and pension funds and I can say with 100% certainty that the World Financial Conference Outlook is a heck of a deal.

But you decide. After decades of broadcasting I certainly understand that a lot of people aren’t interested in economics or even their personal finances, (too bad so many work in the media.) As the old saying goes – “change brings opportunity” but it sure as heck helps to know what’s coming.

I hope you and your family are doing as well as can be expected in what author, Christopher Kock describes as “the year of living dangerously.”

My sincere best wishes,

Mike

P.S. To reserve your tickets right away CLICK HERE

P.S. There are still some special discount rooms available at the Westin Bayshore. Treat yourself to a weekend at one of Canada’s most picturesque venues on Coal Harbour right next to Stanley Park. And walk straight from your room to the World Outlook Conference hall.

P.P.S. We are excited to be back live and in-person for the first time since 2020. But I know that it is sometimes impossible to physically attend the event. Don’t worry. We will provide access to a HD streaming video archive that can be viewed on an unlimited basis from any device, from anywhere in the world that has internet access. The archive will be available 48 hours after the Conference ends and includes all our mainstage speakers plus a select set of the workshop presentations. CLICK HERE to subscribe.

S&P 500 Momentum Barometers

The intermediate term Barometer added 3.20 to 67.80. It remains Overbought. Short term trend is up.

The long term Barometer added 3.60 to 60.80. It changed from Neutral to Overbought on a move above 60.00. Short term trend is up.

TSX Momentum Barometers

The intermediate term Barometer added 4.24 to 69.49. It remains Overbought. Short term trend is up.

The long term Barometer added 1.69 to 55.93. It remains Neutral. Short term trend is up.

Disclaimer: Seasonality ratings and technical ratings offered in this report and at

www.equityclock.com are for information only. They should not be considered as advice to purchase or to sell mentioned securities. Data offered in this report is believed to be accurate, but is not guaranteed