by Larry Adam, Chief Investment Strategist, Raymond James

The U.S. economy continually showed its resiliency through a challenging year.

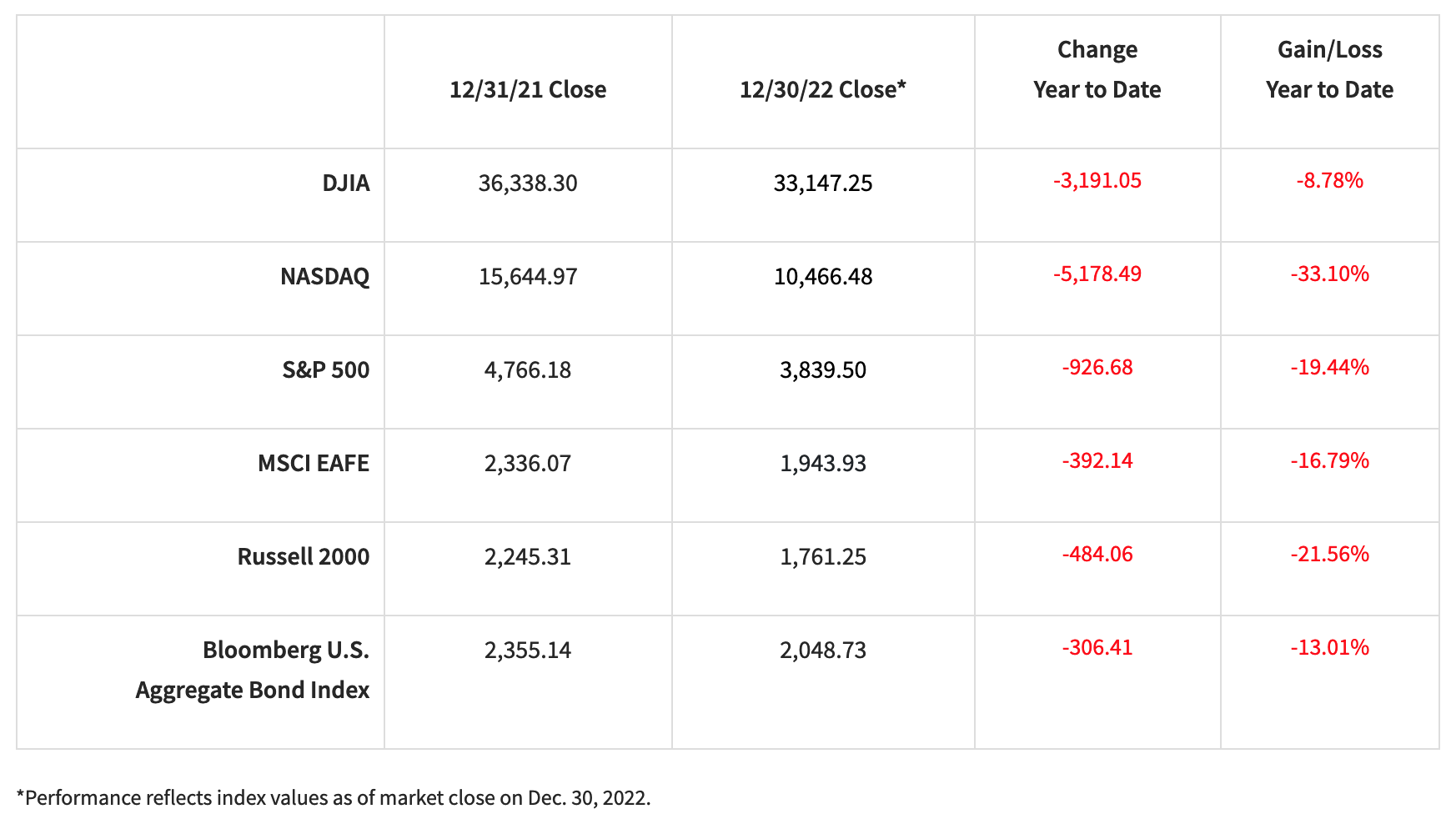

December did not bring the good tidings investors wished for – and typically see in the final month of the year – as most major asset classes struggled at the end of an especially volatile year for the capital markets.

December is historically the third-strongest month for the S&P 500 Index, but the blue-chip stock index declined 5.9%, among its worst December returns since the early 1930s. For the year, the Index was down 19.4%.

Fixed income offered little reprieve from equity struggles. Given the sharp rise in yields, the bond market experienced its worst year since 1975. It was a rare synchronized drop for equities and bonds, which are typically noncorrelated.

“Hopefully, this poor performance for both markets will be isolated to 2022,” Raymond James Chief Investment Officer Larry Adam said. “Our forecasts and outlook for 2023 reflect more positive, albeit more muted returns.”

There are signs inflation is slowing, though some indicators suggest stubborn resilience to efforts by the U.S. Federal Reserve (Fed) to cool the economy. Despite seven rate hikes for a total of 4.25% in 2022, inflation remains elevated.

Before we get into other noteworthy topics, let’s take a look at how we ended the year.

U.S. economy remains resilient

Inflation has continued to slow, with the U.S. Consumer Price Index beating consensus expectations with an increase of only 0.1% in November. The housing market and demand for goods have also slowed as the effects of higher financing costs have affected consumers. The service sector, however, has continued to defy attempts by the Fed to cool overall economic activity. Employment data also remains strong, with an unemployment rate of 3.7% in November approaching historical lows.

Policy debate await newly split Congress

The year-end passage of key defense and funding bills removed a degree of uncertainty around U.S. fiscal policy for the year ahead, though the bigger story could be which policy priorities were not addressed. The omnibus government funding bill did not include riders for technology/antitrust scrutiny, energy permitting reform, cannabis legislation, accelerated research and development expenses or the potential extension of a modified child tax credit – leaving these issues without a clear path forward. Headwinds for near-term Congressional action will further increase with the power shift in the House to a Republican majority, which will narrow the legislative pathway to must-pass consensus policies.

Renewed support for Ukraine

Ukrainian President Volodymyr Zelensky’s visit to Washington, D.C., underscored that U.S. support for Ukraine’s defense will continue for the foreseeable future as the conflict with Russia shows no signs of a shift toward a peace settlement. As such, risks of escalation will persist and global macro headwinds will continue to be a significant overhang, at least into the first half of 2023.

Europe keeps the heat on

Europe is avoiding the worst-case scenario of the energy crisis: there are no natural gas shortages this winter. After starting the heating season with average European Union gas storage at 95% capacity, reserves remained at 83% in late December, roughly the midpoint of winter. The relief from having enough gas to get through the winter is reflected in, among other things, the euro’s partial recovery versus the dollar: the EUR is at 1.07 USD, up from 0.95 USD just a few months ago.

China shifts from strict COVID stance

China’s National Health Commission issued updated guidelines in late December, significantly easing the country’s strict pandemic measures as they relate to both domestic infections and inbound international travelers. The challenge facing the country’s medical services increased at a time when infection rates are soaring. Temporary labor shortages, coupled with supply chain disruptions, seem likely to hamper China’s economic recovery after a subdued 2022.

Strikes disrupt United Kingdom economy

The United Kingdom is thought to have entered a recession. The country is experiencing labor unrest as workers push for higher wages as a result of soaring inflation and squeezed household incomes. More than 300,000 union workers, roughly 1% of the workforce, walked out in December during a series of strikes across a range of significant sectors. The loss of roughly 1.5 million working days could amount to as much as 0.5% off gross domestic product in a worst-case scenario.

The bottom line

Additional interest rate increases likely will occur early in 2023. While inflation is expected to moderate over the coming year, it will take time for the Fed’s actions to take full effect. Once they do, indicators point toward a mild recession in the latter half of the year. While much of this discomfort has already been priced into the markets, headwinds could persist.

By the end of 2023, the outlook for economic growth is expected to improve.

If you have any questions, please do not hesitate to reach out to your financial advisor.

Investing involves risk, and investors may incur a profit or a loss. All expressions of opinion reflect the judgment of the authors and are subject to change. There is no assurance the trends mentioned will continue or that the forecasts discussed will be realized. Past performance may not be indicative of future results. Economic and market conditions are subject to change. The Dow Jones Industrial Average is an unmanaged index of 30 widely held stocks. The NASDAQ Composite Index is an unmanaged index of all common stocks listed on the NASDAQ National Stock Market. The S&P 500 is an unmanaged index of 500 widely held stocks. The MSCI EAFE (Europe, Australasia and Far East) index is an unmanaged index that is generally considered representative of the international stock market. The Russell 2000 is an unmanaged index of small-cap securities. The Bloomberg Barclays US Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market. An investment cannot be made in these indexes. The performance mentioned does not include fees and charges, which would reduce an investor’s returns. Bond prices and yields are subject to change based on market conditions and availability. If bonds are sold prior to maturity, you may receive more or less than your initial investment. Holding bonds to term allows redemption at par value. There is an inverse relationship between interest rate movements and bond prices. Generally, when interest rates rise, bond prices fall and when interest rates fall, bond prices generally rise. Investing in the energy sector involves special risks, including the potential adverse effects of state and federal regulation, and may not be suitable for all investors. Investing in commodities is generally considered speculative because of the significant potential for investment loss. Those markets are likely to be volatile, and there may be sharp price fluctuations even during periods when prices overall are rising. International investing involves special risks, including currency fluctuations, differing financial accounting standards, and possible political and economic volatility.