by Rick Rieder, CIO, Global Fixed Income, Blackrock

An astounding $200 million dollars per day, every day, is spent gambling in Las Vegas casinos. Each day this year, there have been an average of 104,000 visitors to the city, about 75% of whom try their luck in some form or other, each spending about $2,000 a day. Still, these numbers are dwarfed by the wagers that are being made in today’s financial markets. That raises the question: has the gambling capital of the United States moved?

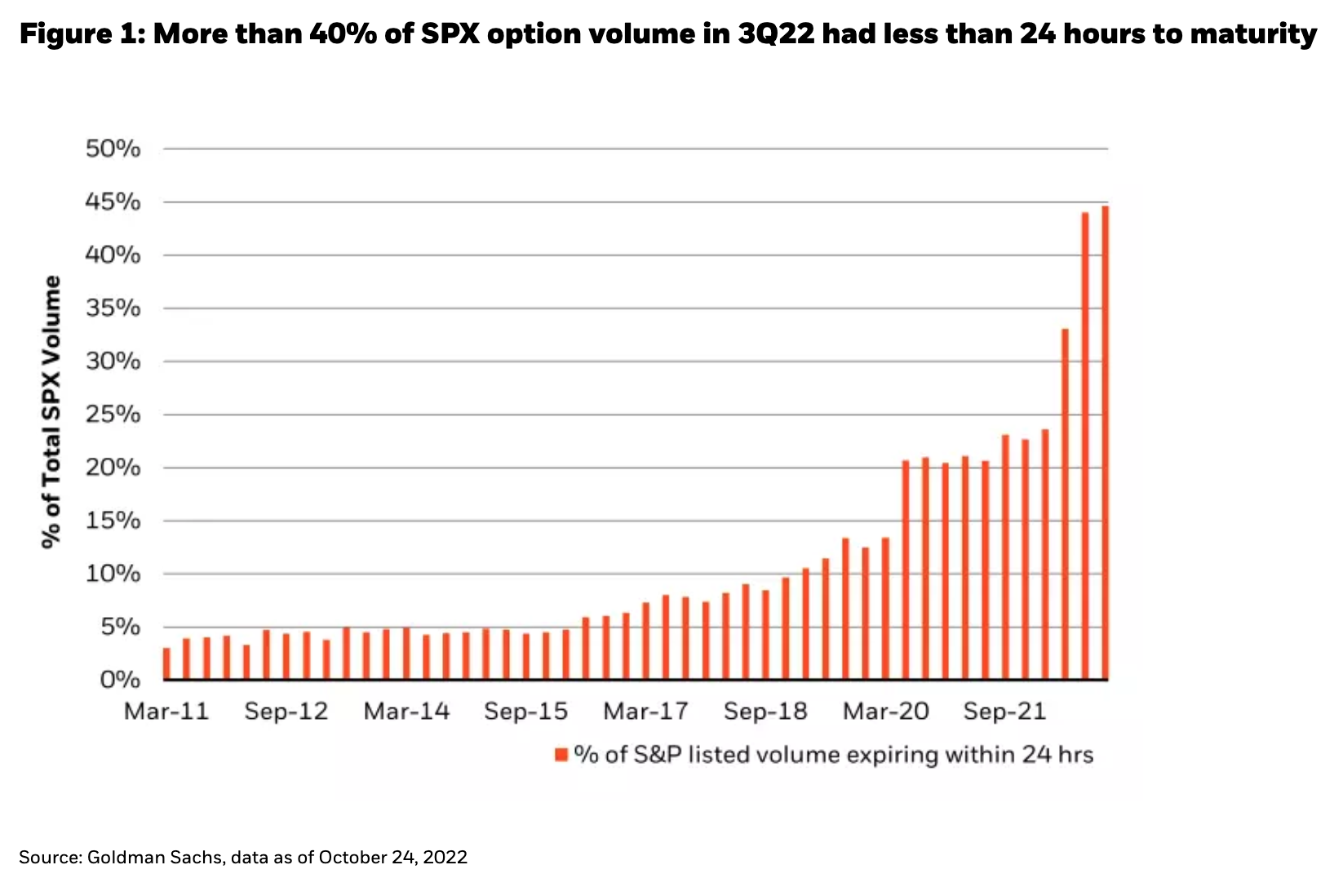

Almost half of the option contracts being traded on the S&P 500, to the tune of $300 billion of notional each day, have one-day expiries or less (see Figure 1). These bets that pay out if the stock market closes above, or below, a particular level are up from 10% of volume as recently as 2019, and less than 5% of volume in all the years prior to 2017. Across all listed ETFs and indices, an astounding $1 trillion of notional value in put options (bets that an index or ETF will close below a particular level) get traded each day. The influence of the “Gamma Gamblers” is one that market participants have never encountered before, and it comes at a time when the aggregate equity short position is the largest on record.

Against such a backdrop, an investor trying to hold any long-term investment view has been severely tested this year unless they were sitting in cash. While the trend in financial asset prices has been unequivocally lower, the most violent moves have been overwhelmingly higher. In October, the velocity of daily moves to the upside dwarfed moves to the downside – almost like coming out of a severe recession, like in April 2020.

Against such a backdrop, an investor trying to hold any long-term investment view has been severely tested this year unless they were sitting in cash. While the trend in financial asset prices has been unequivocally lower, the most violent moves have been overwhelmingly higher. In October, the velocity of daily moves to the upside dwarfed moves to the downside – almost like coming out of a severe recession, like in April 2020.

Liability managers have had a particularly difficult year, as typically “low risk” U.S. investment grade bond indices have had their greatest drawdown ever, losing almost as much money as the S&P 500 (more than 20%). And in the U.K., the safest of domestic assets – U.K. government bonds – have introduced the most volatility to portfolios this year.

Will investing ever be attractive again?

We think so, but it will require some evidence of change in the inflation paradigm – evidence we think we will see in the coming months. Inflation is much too high today, and guessing the policy response to each incremental data point has dominated markets in recent months. Outsized option premiums can be seen around events that contain new inflation, employment, or policy information, while little else is ascribed much event risk premium. Thus far, inflation has trended the wrong way – toward becoming more ingrained, and less about idiosyncratic pandemic shocks, while the labor market remains too strong.

Yet, there is reason to believe some disinflation could start seeping into the data post-Halloween: used car prices are 15% below their January peak, which is not yet reflected in official inflation data. Also, energy commodities have come off the boil and with no further change will show a 21% decline by next June. Retail inventories are at record highs as companies overstocked in response to unsustainable pandemic demand, and supply chain pressures, freight and logistics are no longer inflationary, and could soon be a source of deflation.

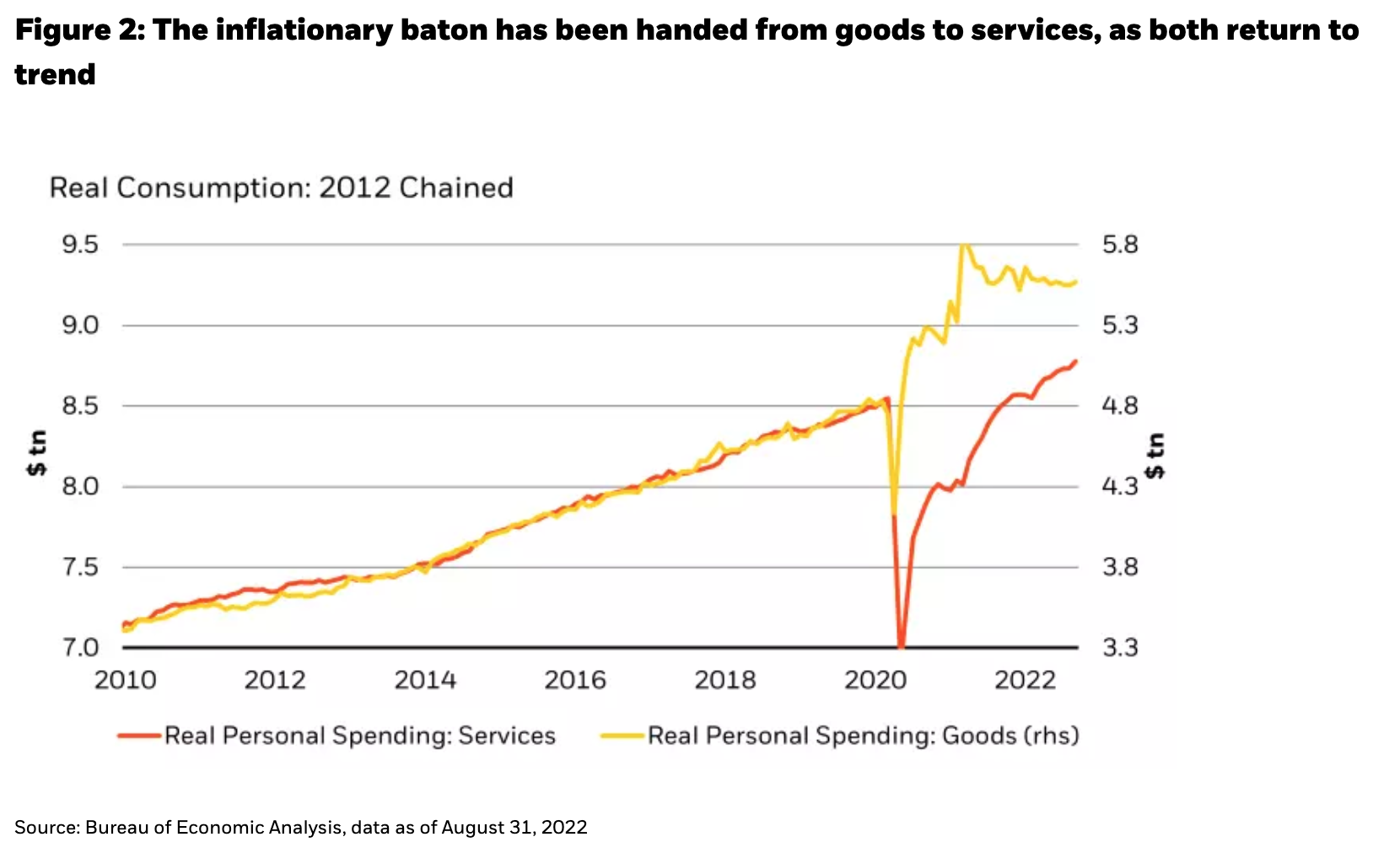

So, with goods prices set to decelerate from here, core services are the source of today’s inflation uncertainty. Prices have been appreciating on the back of pent-up demand, creating a post-pandemic boom. While the rate of price increases should slow from their frenetic pace, there is still room for services demand to grow back to its pre-pandemic trend, suggesting that prices will stay stubbornly high for a while (see Figure 2).

The single biggest component in core services is shelter, and it is running hot, but data around house prices and rents comes with a lag due to a methodology that purposefully smooths noisy data, and delays such as the time between listing, reducing a price and closing. So, despite the strength in shelter inflation, based on what is happening “on the ground,” we expect it to slow over the next 12 months. That’s particularly due to the fact that as higher mortgage rates deter new home buyers, allowing prices to drop, it will eventually allow would-be homebuyers who were forced into the rental market to give up renting once their starter home (or dream home) becomes affordable again, thereby alleviating pressure on the rental market. Once this self-reinforcing wheel starts turning, disinflation can play out quickly, as housing has an outsized influence on the U.S. economy – and one that has often been underestimated by policymakers (for example, in the runup to the Global Financial Crisis, or GFC).

With such a big influence on the economy, could a housing slowdown cause a repeat of the GFC?

Housing’s economic influence cannot be overstated. For one, higher house prices have created positive wealth effects, especially for lower income cohorts. Given the leverage embedded in the housing market, especially amongst lower income cohorts who are more likely to need a mortgage, it is important that loan to value ratios remain reasonably supported. Yet, the leverage in the housing market today is much less concerning than it was in 2007. In fact, household liabilities are at the lowest levels they’ve been in four decades, while household cash balances and homeowners’ equity are near 30-year highs. Further, the last decade of low rates has allowed most homeowners to lock in extremely low mortgage rates, meaning household interest payments in the 2020s are taking up a smaller share of disposable income than in any decade prior (it’s certainly not pleasant being a new buyer, though).

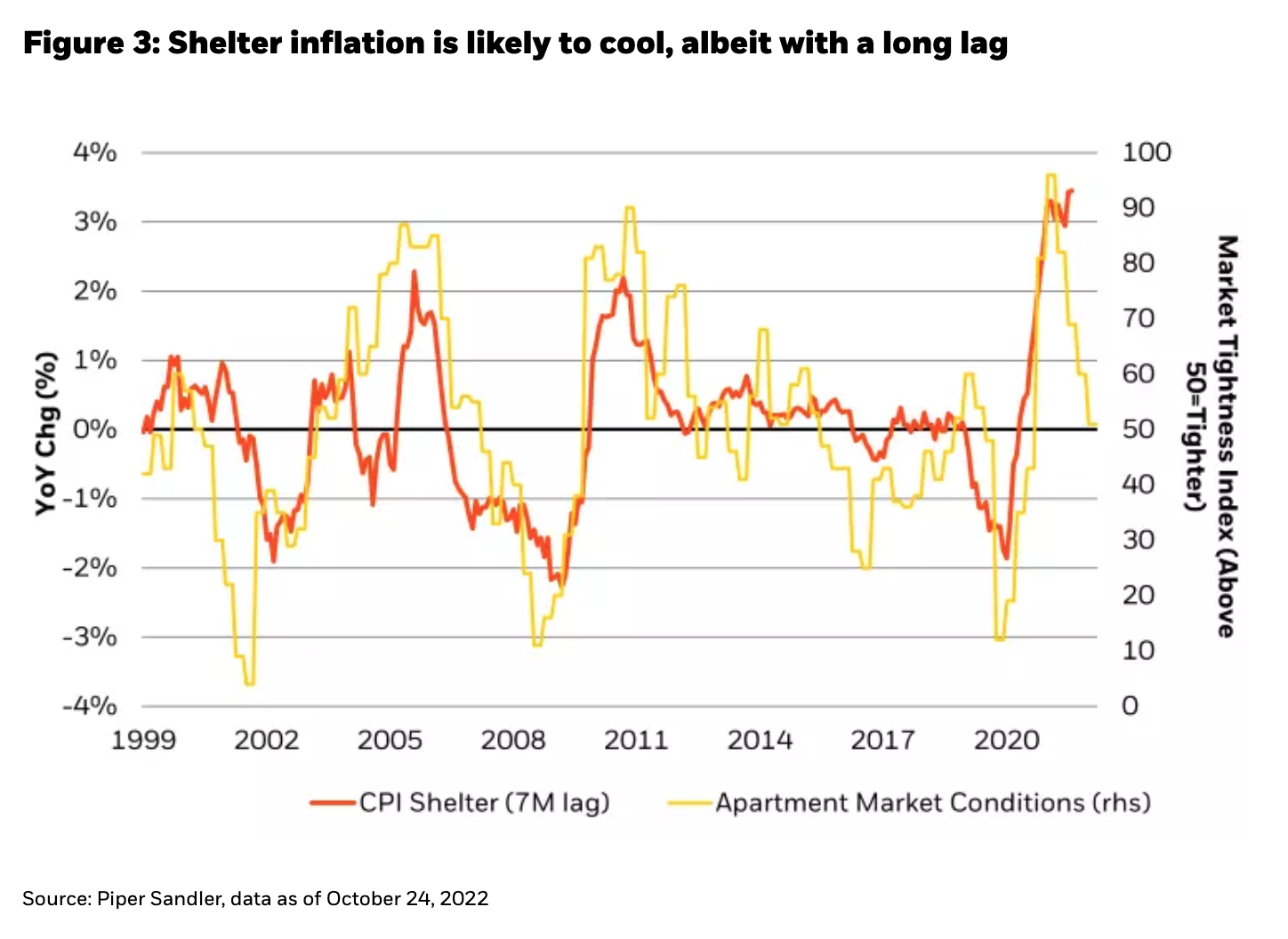

Apart from wealth effects and leverage, housing also has an outsized influence on employment. About nine jobs are indirectly created for every direct real estate job, one of the highest employment multipliers of any sector, according to Economic Policy Institute data as of January 2019. Thus, the 2.4 million people employed directly in the real estate industry would equate to about 21.6 million people whose fortunes are indirectly tied to the real estate sector. A slowdown in real estate accompanied by a small loss in employment could apply substantial brakes to the economy, helping to cool inflation from multiple angles (see Figure 3).

From the perspective of tightening financial conditions, there are sectors more vulnerable than the residential housing market that warrant closer observation. Commercial real estate (CRE) is one of them – with more leverage and facing pressure from both higher financing costs and higher cap rates (lower valuations) going forward, discretion needs to be applied when investing in CRE. Just a 150-basis point increase in financing rates and the exit cap rate of a CRE investment can more than halve the return on equity of that investment. It would require outsized rent growth to preserve the investor’s original rate of return – a degree of pricing power that not every CRE landlord holds.

Internationally, we have already seen vulnerabilities play out in the U.K., Europe and China. All three are energy importers that have suffered to varying degrees from the financial tightening in the U.S. In the U.K. and Europe, inflation is running even higher than in the U.S., in part due to a strong U.S. dollar, and their economic prospects could boil down to the severity of weather this winter. China is still struggling to emerge from zero Covid policies that have held the economy back, while the latest leadership transition leaves major uncertainties around economic policy and the regulatory framework. The yuan has weakened, as has consumer confidence, along with the confidence of international investors (as evidenced by China credit default spreads that have tripled this year).

So, how can the Fed set one single interest rate to account for all the excesses (such as inflation), and all the risks (financial leverage, international risks) in the system today without “’breaking something” from here? And perhaps more importantly for investors, how should risk and reward be assessed in portfolios?

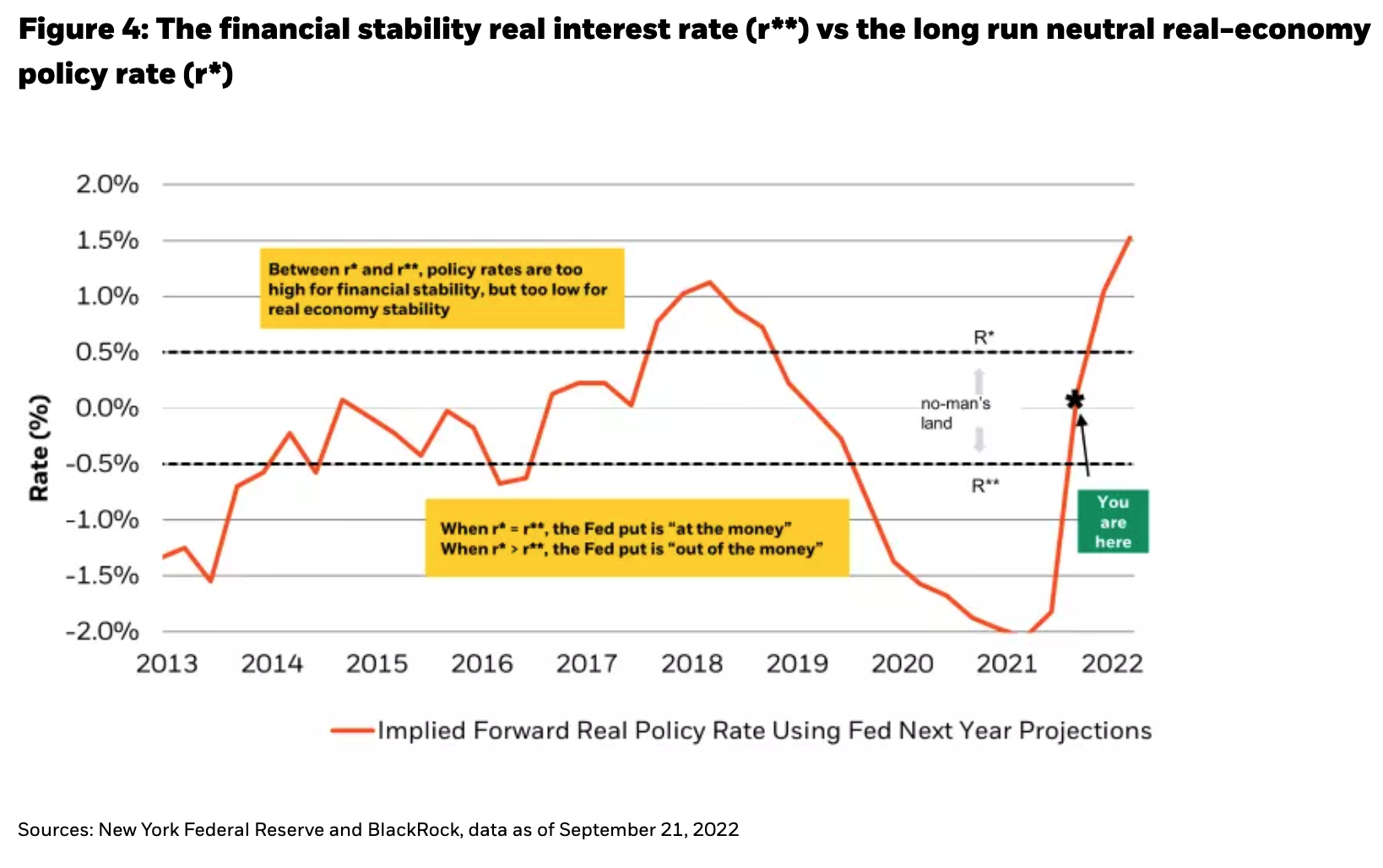

A study by the New York Fed suggests that the interest rate level that slows down aggregate demand in the U.S. real economy is indeed likely to be too high for the financial economy, and for the rest of the world (see Figure 4). To date, real interest rates as measured in financial markets have reached decade highs (using breakeven inflation expectations as the deflator). However, if real interest rates were to be measured using a more realistic measure of costs for a company in the real world, such as wage inflation, then real rates would remain at multi-decade lows. In a regime of hot inflation in the real economy, amidst a highly levered financial economy, there is likely massive dissonance associated with finding a harmonious equilibrium through a single policy rate setting.

A policy rate that is between r* and r** will not slow the real economy nearly enough, but it will damage the financial economy substantially. It is no wonder then, that financial market indices have had their worst year since 2008 – U.S. Treasuries and equities alike, and every asset in between. No index of stocks or bonds has been able to meet a wealth or liability manager’s benchmark. In an environment where r* is greater than r**, being tactical and aggressive in asset allocation may be hugely accretive, certainly more so than sitting back and hoping that indices outperform benchmarks, like they did during QE years.

Yet, for the astute investor, opportunities for upside do exist even among underperforming indices. Equity dispersion is at its highest since the GFC, a phenomenon that rewards active managers and punishes indices. Even in the Treasury market, with its record-breaking losses, outsized returns might be found if operating in the right part of the curve.

Across markets, value seems to be less apparent the lower down the capital stack one goes. Equities, at the bottom of the capital stack, are offering less risk premium than at the beginning of the year, whereas the risk premium in credit has expanded substantially. In fact, for equity returns to match the implied returns in the high yield market over the next two years, all else equal, the equity P/E multiple would need to expand by over 3 turns, to a very full 20x (see Figure 5).

Markets are driven by valuation over the medium to long-term, but by technicals over the short-term. One must be a student of both today. Leverage in financial markets is much more often applied to fixed income rather than equities, hence loss-induced de-risking tends to impact fixed income securities more than equities. Furthermore, equities are frequently used as a hedge (via a short position), to the extent that a persistent short-covering bid seems to be lurking in the market, ready to pounce on the slightest sell-off.

Investors with longer horizons should view bear market rallies that are founded on technicals with the appropriate degree of skepticism. We are still in the midst of the fastest hiking cycle since at least 1994, with no clear sign of when it will end. Over the last year, financial conditions have tightened as quickly as they did at the height of the GFC. Many of the ramifications of such quickly tightening policy are still rippling through the financial system, much less the real economy.

Follow Rick Rieder on Twitter

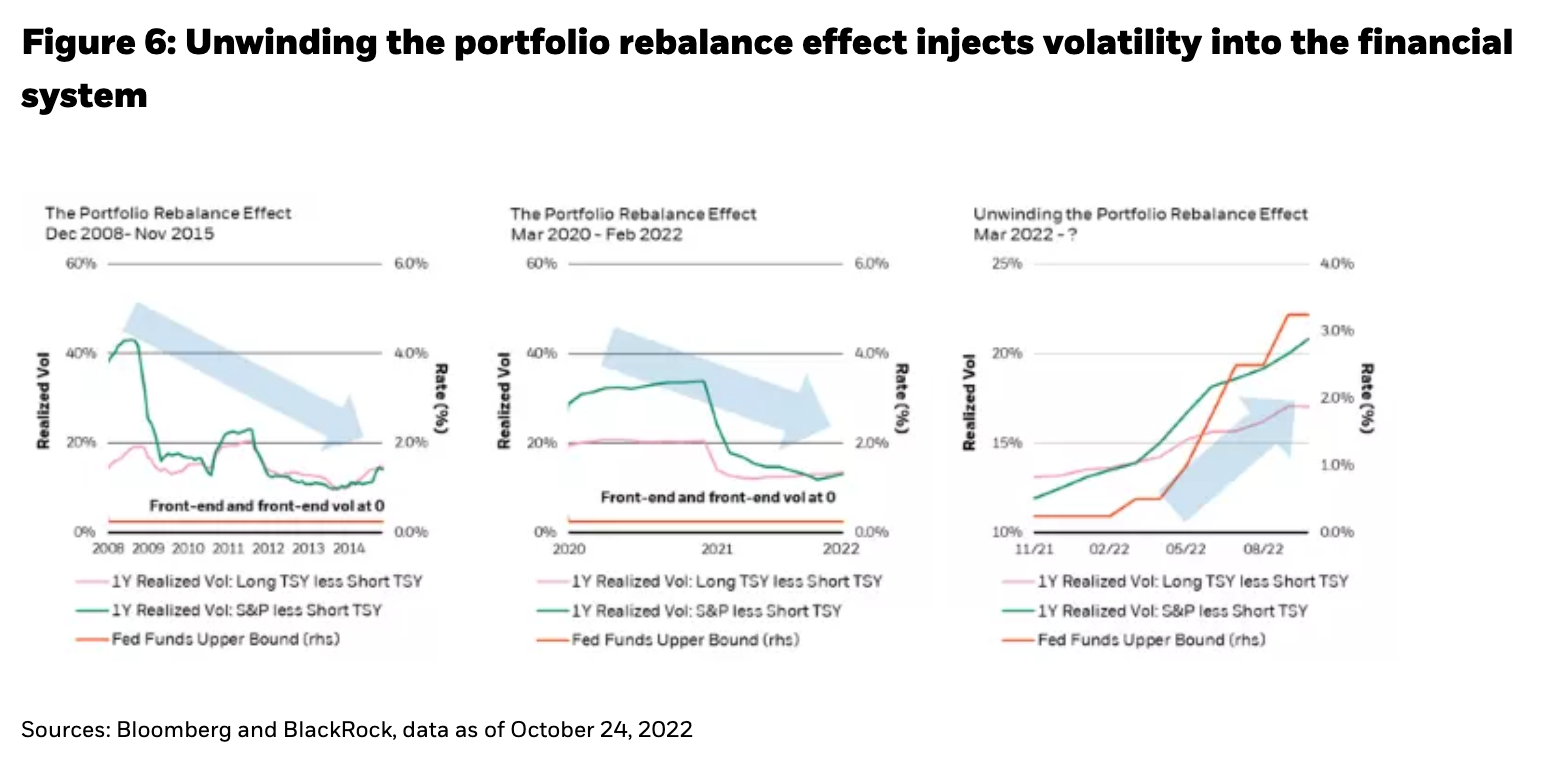

One such ripple: the portfolio rebalance channel that was so powerfully evident during deflationary episodes is now working in reverse. Instead of suppressing volatility in financial assets by holding rates at 0% and buying assets through QE programs, the Fed is actively injecting volatility back in. Recall that the Fed never needed to keep cutting rates below 0% to squash volatility out the yield curve and down the capital stack – it just needed to hold rates there. Likewise, today the Fed does not need to keep hiking into infinity to inject volatility back into the bottom of the capital stack and out the curve, it just needs to hold rates at restrictive levels (see Figure 6).

The investment opportunity set becomes materially different from what most market participants have gotten used to during QE environments, especially if one were to believe that the Fed could pause after reaching a sufficiently restrictive policy rate – and keep rates high for a long time. If the Fed were to simply follow the policy path outlined by the market, reach the market-implied terminal rate, and then stand pat for some time, wouldn’t this create an environment where front-end assets offered even less volatility while other assets continued to endure the higher-volatility environment caused by the long and variable lags of policy tightening?

Front-end high-quality bonds would become very interesting from a total return, Sharpe ratio, and carry breakeven perspective, without much duration or credit risk. In both the U.S. and Europe, the 1-2 year bonds of household names regularly yield 6%. Such bonds would need to yield more than 8% after a year before an investor would start losing money. The same is true for high quality securitized assets, where AAA securitized bonds yield up to 7%.

On the other end of the fixed income spectrum, long duration investment grade bonds have become so beaten down in price by this year’s interest rate widening that many are closer to recovery-on-default levels than to par. In fact, last year one had to pay up to $12 to move from the 5-10 year part of the investment grade curve to the 20-30 year part. Today, one can collect $7 to do such a trade – effectively raising cash without giving up any yield or spread. One used to have to “go out the curve” to pick up yield – today, one can go out the curve to pick up cash.

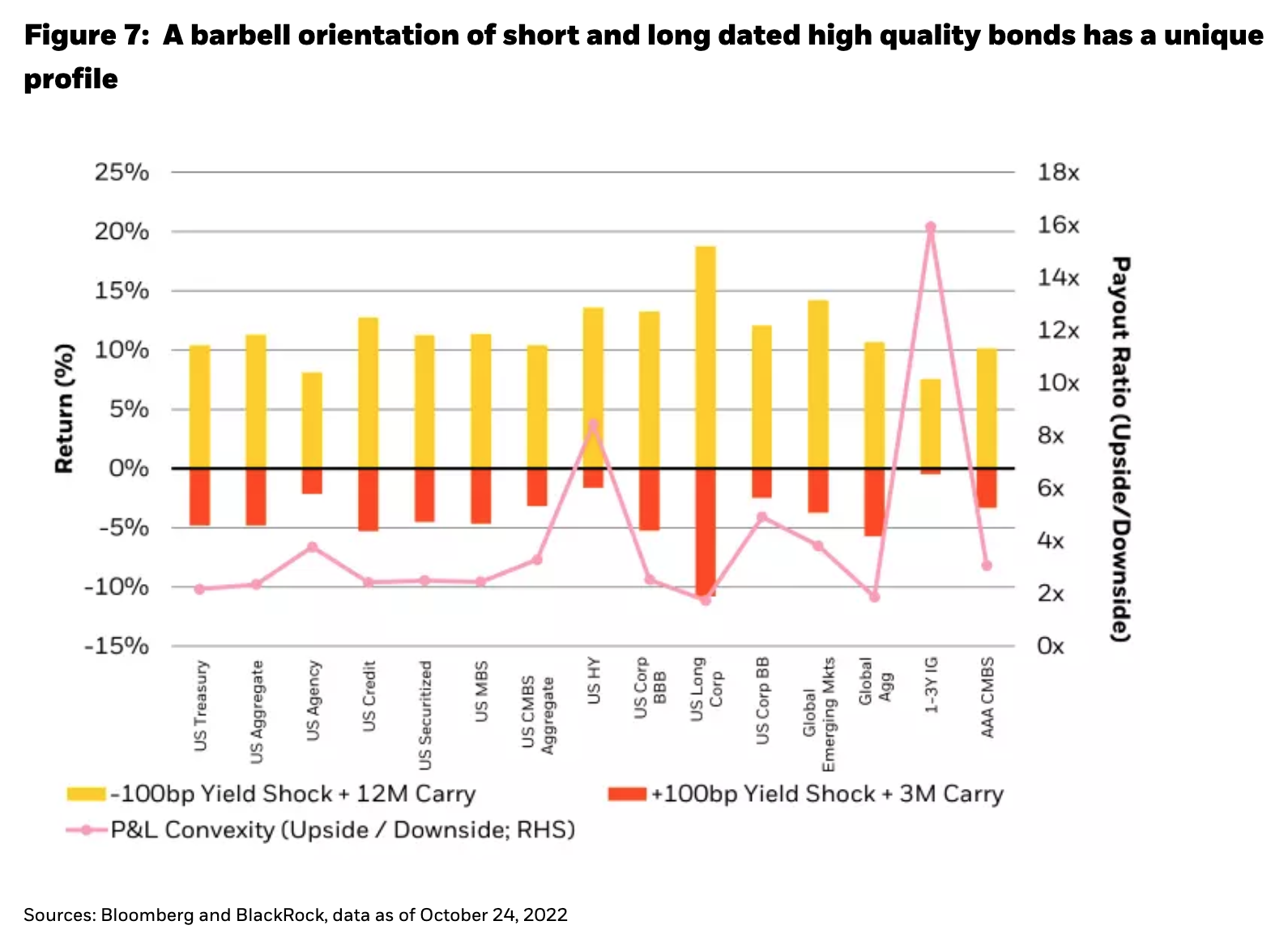

This repricing in yields and prices has profound implications for portfolio convexity. Normally, creating a convex return profile in a portfolio (where there is more to be gained than lost) requires the use of complex and expensive options. It has almost never involved using a high-quality bond. Yet today, gamma gambling has driven the price of call options to the richest they’ve ever been (relative to puts). Convexity through options is as expensive as it has been rewarding this year.

Instead, consider two scenarios: 1) investors’ worst fears are realized into year-end, and yields continue marching upward by 100 bps for the next 3 months, forcing further de-risking/stop-outs; and 2) yields peak and rally 100 bps over the next 12 months (remember that since we are not holding an option, we are not constrained by an expiry). Despite the perfectly symmetric yield outcomes, most fixed income sectors show an extraordinary degree of positive payout convexity to these scenarios. Indeed, the bull case for U.S. long corporates looks more like an equity market return in a good year, while the 16-to-1 payout ratio at the front-end of the investment grade curve rivals that of exotic options (see Figure 7).

We are at a unique point of time where portfolio convexity can be created more cheaply and creatively in fixed income than by solely using options (and competing with the gamma gamblers on price), while simultaneously conserving cash, earning carry (rather than paying decay), and keeping beta moderate. The world could get less scary in 2023, but it may not. Either way, we believe that by using the full spectrum of assets at our disposal, we have the ability to build a much less risky portfolio today than in the past, while still creating a very “gamma-investor” like convexity to it.