by AllianceBernstein Multi-Asset Research

Equity valuations have fallen substantially as central banks hike interest rates to combat inflation. History suggests that unless rates rise dramatically from here, valuation compression may have nearly run its course in the US stock market.

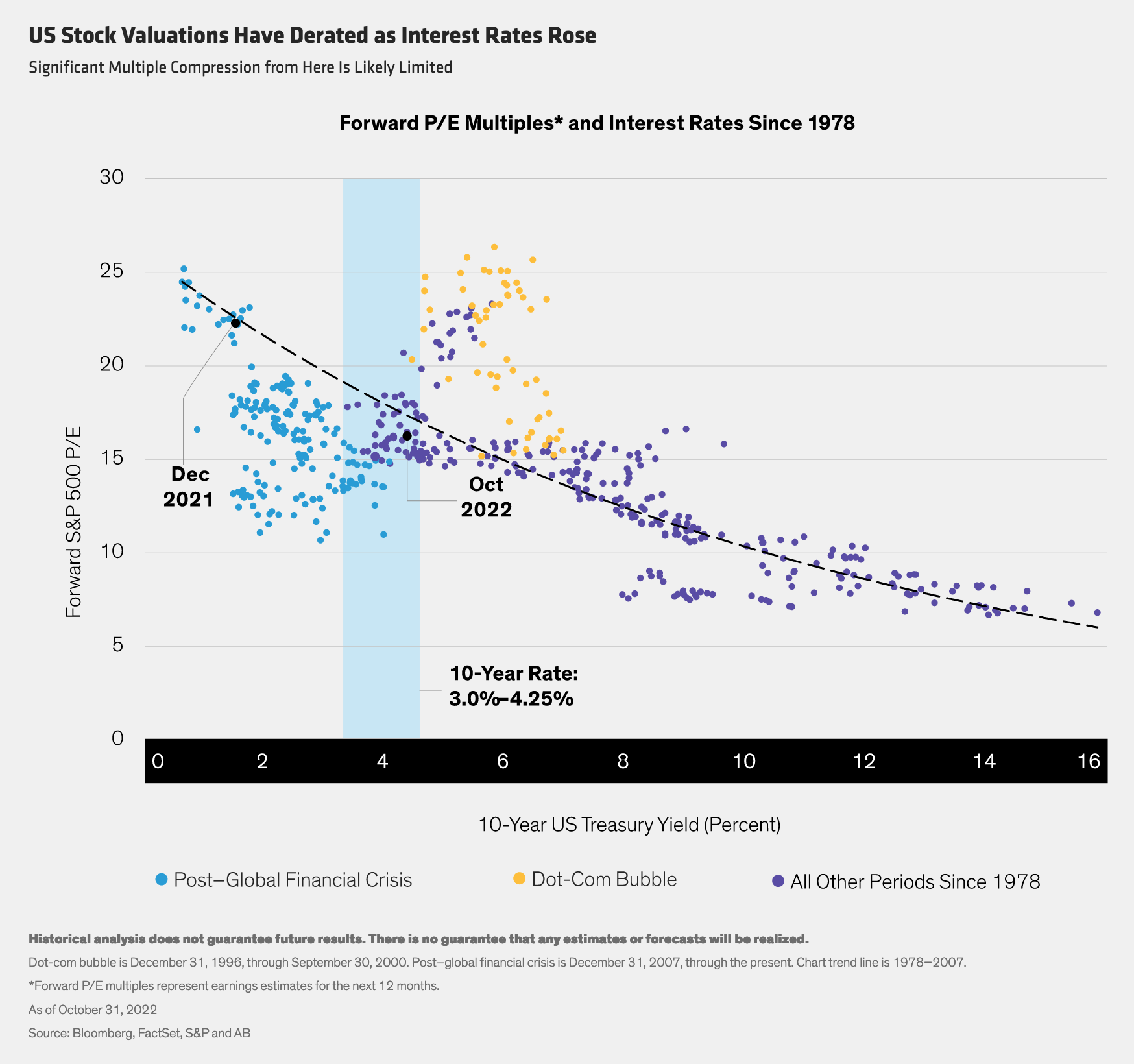

Rising interest rates have dominated this year’s macroeconomic and market agenda. The 10-year US Treasury yield jumped from 1.51% to 4.05%, from the beginning of 2022 through the end of October. Over the same period, the forward price/earnings ratio of S&P 500 stocks fell from 22.3x to 16.7x—a 25% decline. Rising rates push up the discount rate used to value stocks, which tends to push valuations down. Growth stocks with cash flows that are further out in the future often get disproportionally hurt by rising rates—a trend that has played out this year.

Searching for the Bottom

Are we nearing an end to valuation compression? It’s still hard to say, because a company’s P/E ratio is determined by both its share price and earnings per share. In many cases, earnings forecasts haven’t come down enough to reflect the potential business decay ahead. Given uncertainties about inflation, rates and growth, some investors are concerned that share price declines and current valuations don’t yet reflect the deteriorating environment.

However, there are some indications that market valuations are unlikely to fall much further from here. Looking at the relationship between interest rates and equity valuations since 1978, a clear pattern emerges: In most periods when yields were between 4%–6%, P/E valuations didn’t fall much below 15x (Display). P/Es only fell below significantly below that level when rates exceeded 8%. The main exception was in the period after the Global Financial Crisis, when a deep recession prompted both low rates and low P/Es—a very different mix of conditions than we are experiencing today, especially if a deep economic downturn can be avoided.

Positioning for a Recovery in Individual Stocks

Of course, past performance doesn’t guarantee future results. And with inflation still raging in many parts of the world, interest rates may climb further. But if inflation begins to ease, rates should stabilize. In fact, Fed funds futures imply that the US Federal funds rate will peak at nearly 5% by early 2023. We think it’s unlikely that rates will climb to extremely high levels seen in the early 1980s.

Beneath the aggregate market valuation, we believe investors can find individual opportunities, for example, in companies and sectors that have proven earnings resilience during past recessions. In today’s uncertain environment, investors should search for stocks of select companies whose earnings outlooks are stronger than implied by their low share prices. Building a portfolio of companies with high-quality businesses trading at attractive valuations is a good strategy for positioning for a recovery that should deliver rewards after valuations hit an inflection point.