by Lance Roberts, RIA

The massive debt levels provide the single most significant risk and challenge to the Federal Reserve. It is also why the Fed is desperate to return inflation to low levels, even if it means weaker economic growth. Such was a point previously made by Jerome Powell:

“We need to act now, forthrightly, strongly as we have been doing. It is very important that inflation expectations remain anchored. What we hope to achieve is a period of growth below trend.”

That last sentence is the most important.

There are some important financial implications to below-trend economic growth. As we discussed in “The Coming Reversion To The Mean Of Economic Growth:”

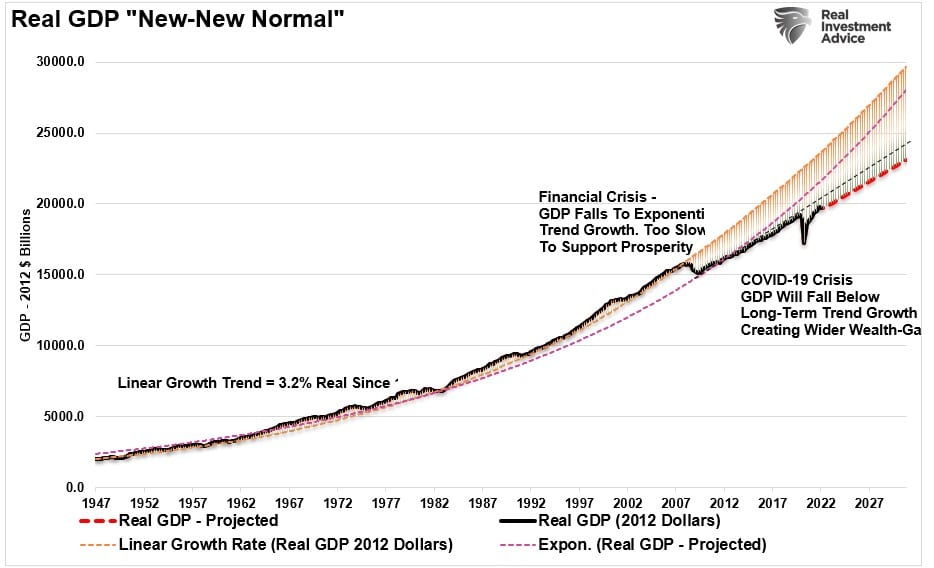

“After the ‘Financial Crisis,’ the media buzzword became the ‘New Normal’ for what the post-crisis economy would like. It was a period of slower economic growth, weaker wages, and a decade of monetary interventions to keep the economy from slipping back into a recession.

Post the ‘Covid Crisis,’ we will begin to discuss the ‘New New Normal’ of continued stagnant wage growth, a weaker economy, and an ever-widening wealth gap. Social unrest is a direct byproduct of this “New New Normal,” as injustices between the rich and poor become increasingly evident.

If we are correct in assuming that PCE will revert to the mean as stimulus fades from the economy, then the ‘New New Normal’ of economic growth will be a new lower trend that fails to create widespread prosperity.”

As shown, economic growth trends are already falling short of both previous long-term growth trends. The Fed is now talking about slowing economic activity further in its inflation fight.

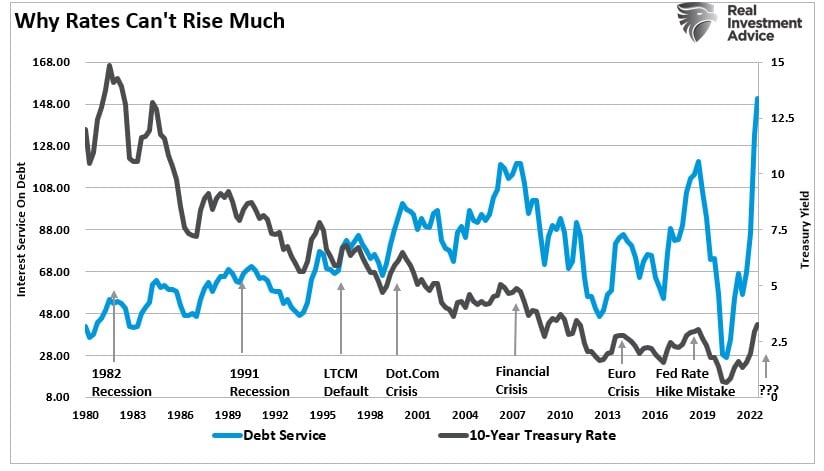

The reason that slowing economic growth, and killing inflation, is critical for the Fed is due to the massive amount of leverage in the economy. If inflation remains high, interest rates will adjust, triggering a debt crisis as servicing requirements increase and defaults rise. Historically, such events led to a recession at best and a financial crisis at worst.

The problem for the Fed is trying to “avoid” a recession while trying to kill inflation.

Recessions Are An Important Part Of The Cycle

Recessions are not a bad thing. They are a necessary part of the economic cycle and arguably a crucial one. Recessions remove the “excesses” built up during the expansion and “reset” the table for the next leg of economic growth. Without “recessions,” the build-up of excesses continues until something breaks.

In the current cycle, the Fed’s interventions and maintenance of low rates for more than a decade have allowed fundamentally weak companies to stay in business by taking on cheap debt for unproductive purposes like stock buybacks and dividends. Consumers have used low rates to expand consumption by taking on debt. The Government increased debts and deficits to record levels.

The assumption is that increased debt is not problematic as long as interest rates remain low. But therein lies the trap.

The Fed’s mentality of constant growth, with no tolerance for recession, has allowed this situation to inflate rather than allowing the natural order of the economy to perform its Darwinian function of “weeding out the weak.”

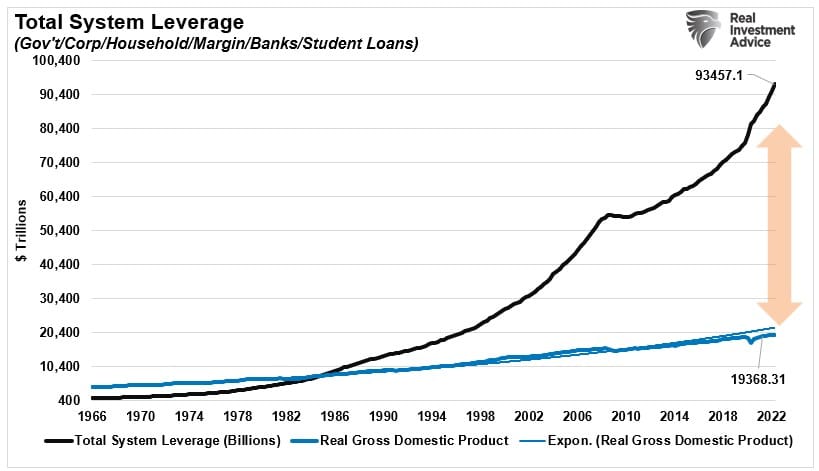

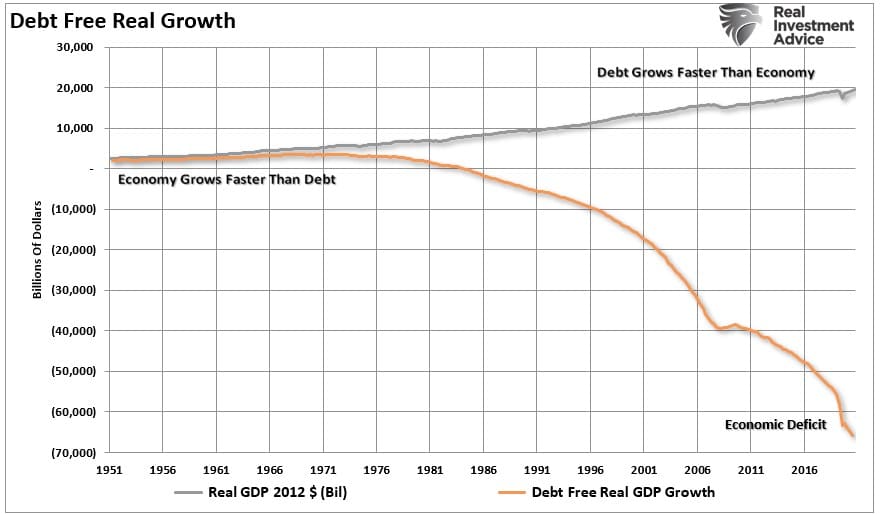

The chart below shows total economic system leverage versus GDP. It currently requires $4.82 of debt for each dollar of inflation-adjusted economic growth.

More Debt Doesn’t Solve Problems

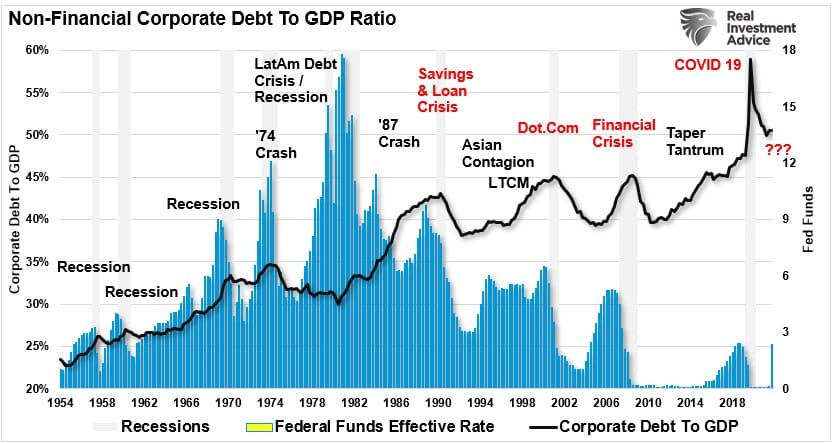

Over the past few decades, the system has not been allowed to reset. That has led to a resultant increase in debt to the point that it impaired the economy’s growth. It is more than a coincidence that the Fed’s “not-so-invisible hand” has left fingerprints on previous financial unravellings. Given that credit-related events tend to manifest from corporate debt, we can see the evidence below.

Given the years of “ultra-accommodative” policies following the financial crisis, most of the ability to “pull-forward” consumption appears to have run its course. Such is an issue that can’t, and won’t be, fixed by simply issuing more debt. Of course, for the last 40 years, such has been the preferred remedy of each Administration. In reality, most of the aggregate growth in the economy was financed by deficit spending, credit creation, and a reduction in savings.

In turn, this surge in debt reduced both productive investments and the output from the economy. As the economy slowed and wages fell, the consumer took on more leverage, decreasing the savings rate. As a result, increases in rates divert more of their disposable incomes to service the debt.

A Long History Of Terrible Outcomes

After four decades of surging debt against falling inflation and interest rates, the Fed now faces its most difficult position since the late 70s.

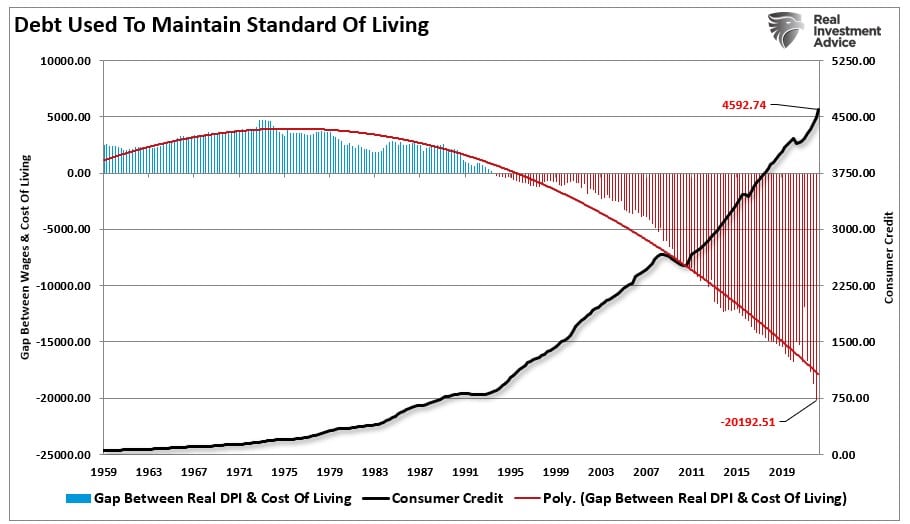

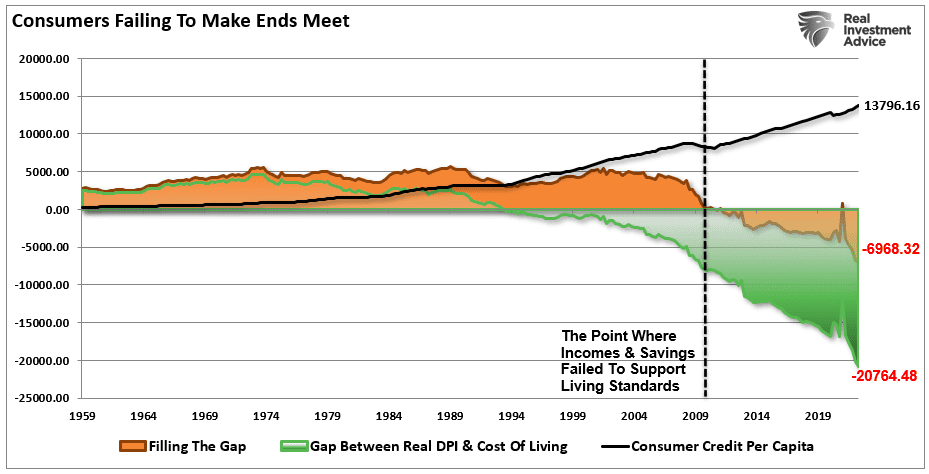

The U.S. economy is more heavily levered today than at any other point in human history. Since 1980, debt levels have continued to increase to fill the income gap. Bigger houses, televisions, computers, etc., all required cheaper debt to finance them.

The chart below shows the inflation-adjusted median living standard and the difference between real disposable incomes (DPI) and the required debt to support it. Beginning in 1990, the gap between DPI and the cost of living went negative, leading to a surge in debt usage. In 2009, DPI alone could no longer support living standards without using debt. Today, it requires almost $7000 a year in debt to maintain the current standard of living.

The rise and fall of stock prices have little to do with the average American and their participation in the domestic economy. Interest rates are an entirely different matter. Since interest rates affect “payments,” increases in rates quickly negatively impact consumption, housing, and investment, which ultimately deters economic growth.

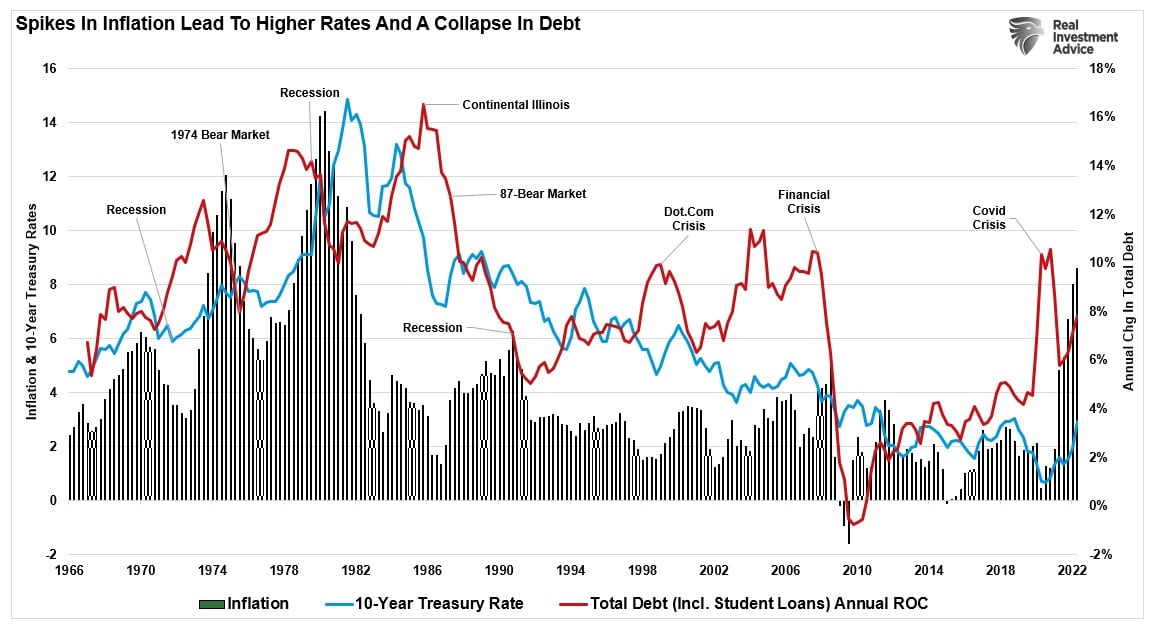

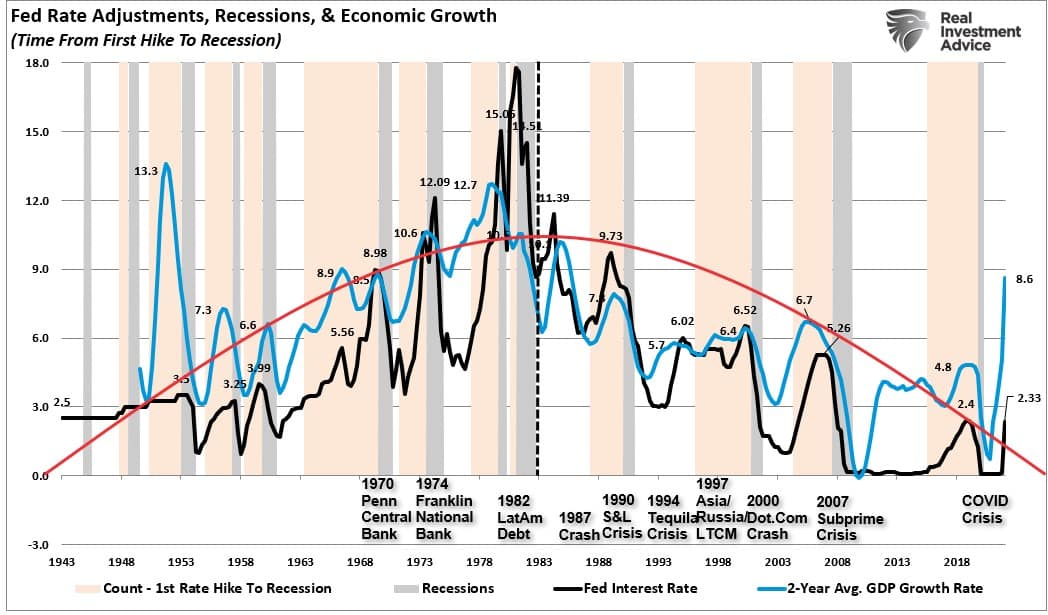

Since 1980, every time the Fed tightened monetary policy by hiking rates, inflation remained “well contained.” The chart below shows the Fed funds rate compared to the consumer price index (CPI) as a proxy for inflation. The current bout of inflation is entirely different, and as the Fed hikes interest rates to slow economic demand, it is highly probable they will over-tighten. History is replete with previous failed attempts that created economic shocks.

The Fed’s Challenge

The Fed has a tough challenge ahead of them with very few options. While increasing interest rates may not “initially” impact asset prices or the economy, it is a far different story to suggest that they won’t. There have been absolutely ZERO times in history the Federal Reserve began an interest-rate hiking campaign that did not eventually lead to a negative outcome.

The Fed is now beginning to reduce accommodation at precisely the wrong time.

- Growing economic ambiguities in the U.S. and abroad: peak autos, peak housing, peak GDP.

- Excessive valuations that exceed earnings growth expectations.

- The failure of fiscal policy to ‘trickle down.’

- Geopolitical risks

- Declining yield curves amid slowing economic growth.

- Record levels of private and public debt.

- Exceptionally low junk bond yields

Such are the essential ingredients required for the next “financial event.”

When will that be? We don’t know.

We know that the Fed will make a “policy mistake” as “this time is different.”

Unfortunately, the outcome likely won’t be.