by Brian Resnick, CFA, Director and Senior Investment Strategist—Alternatives and Multi-Asset, AllianceBernstein

While 2022 has been a challenging year for nearly every segment of the capital markets, it comes with a silver lining for income investors: higher yields. Yields on high-yield bonds, for example, surged from 4.3% at the start of the year to 8.3% at the end of August. History suggests that starting yield has been a fairly reliable gauge of high yield returns over the ensuing five years.

But there’s likely to be a lot of policy uncertainty and interest-rate volatility over the visible horizon, so it’s critical to source income efficiently—generating an attractive income level while also cushioning against the inevitable declines in down markets. The keys: careful asset selection and thoughtful portfolio construction.

The Income Investor’s Dilemma

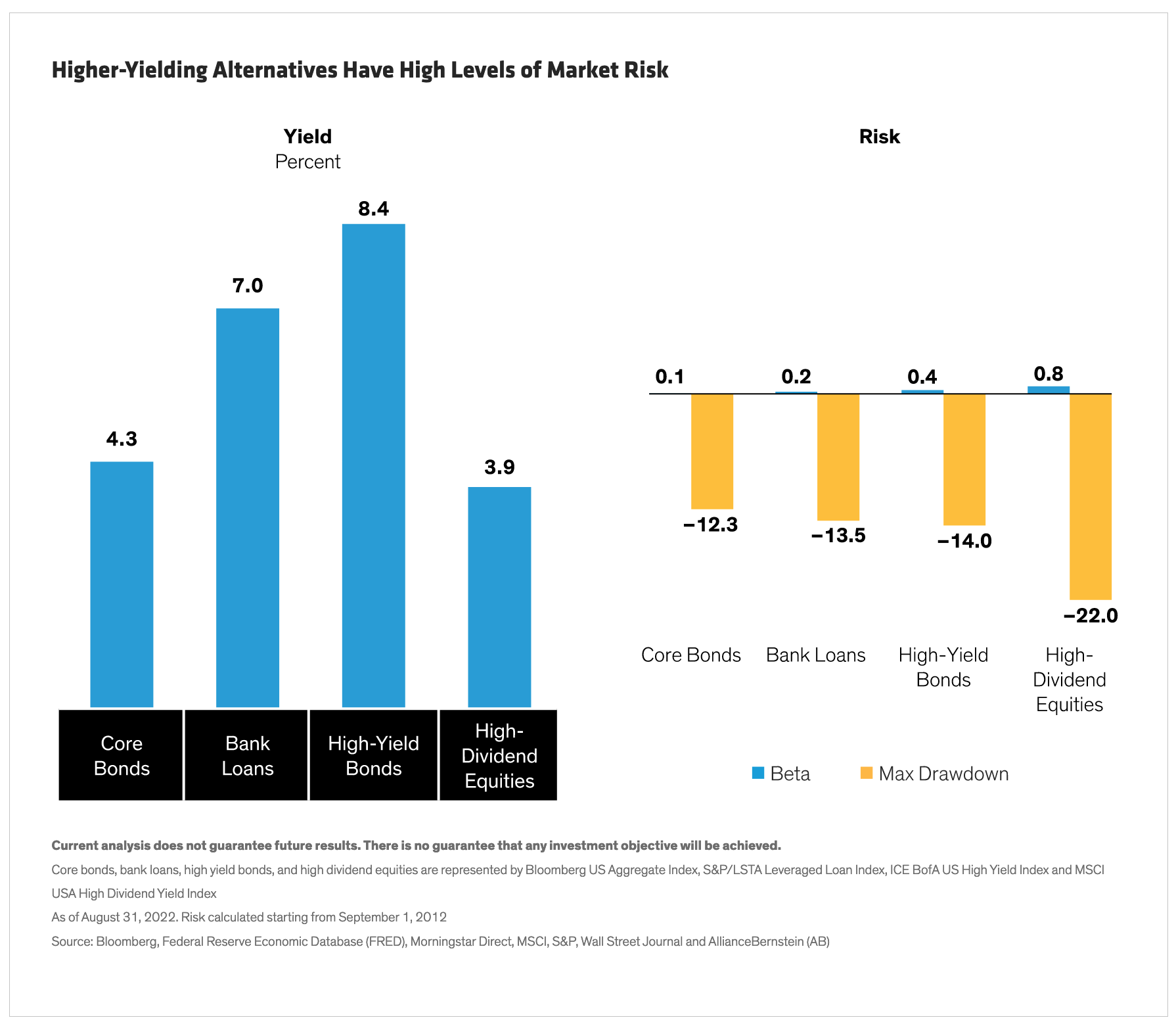

Income investors seeking to boost yields often find themselves depending on higher-yielding investments such as bank loans, high-yield bonds and dividend-paying equities. While these investments can play a valuable role in a portfolio, they carry more risk than core bonds—as seen in their higher equity market beta and bear market drawdowns (Display).

To make matters worse, those drawdowns are likely to happen during an equity downturn, so if investors also include traditional equities in their overall portfolio, it compounds the pain.

Reaching for yield can be especially dangerous for income investors because of sequence risk—the risk of a significant drawdown within 10 years of retirement. After such large market declines, investors’ fixed withdrawal amounts tap a larger percentage of remaining portfolio assets. This predicament can shrink the portfolio at the very time it needs asset growth to recoup losses, permanently impairing income investors’ resources. Even if investors don’t fully deplete their funds, they might need to curtail their lifestyles and downsize or eliminate philanthropic and legacy plans.

Building a More Efficient Income Portfolio

How can investors generate income without taking on too much downside risk? The key to an efficient income portfolio is selecting the most impactful building blocks and assembling them with the proper risk balance.

High-quality core bonds still play an essential role. When stocks and high-yield bonds are selling off during a bear market, high-quality bond prices tend to rise, acting as ballast for the portfolio and smoothing the ride. Given the expected volatility in interest rates over the foreseeable future, many investors seem leery of taking on duration exposure. We think this poses a sizable risk: the rates building block performs a critical function as a countercyclical asset that rallies when risk assets are tumbling.

Rates can provide a downside cushion, but investors must embrace credit to generate income. While some investors focus on US high yield alone, we believe this segment should be part of a diversified allocation to global multisector credit. Investing in a strategy like this—combining global high-yield, emerging-market (EM) debt, securitized credit, and bank loans—gives investors a much broader set of opportunities to generate excess income and alpha. Most important, global multisector bonds have outperformed US high-yield bonds over the past 20 years or so, winning 62% of the time based on three-year rolling periods.

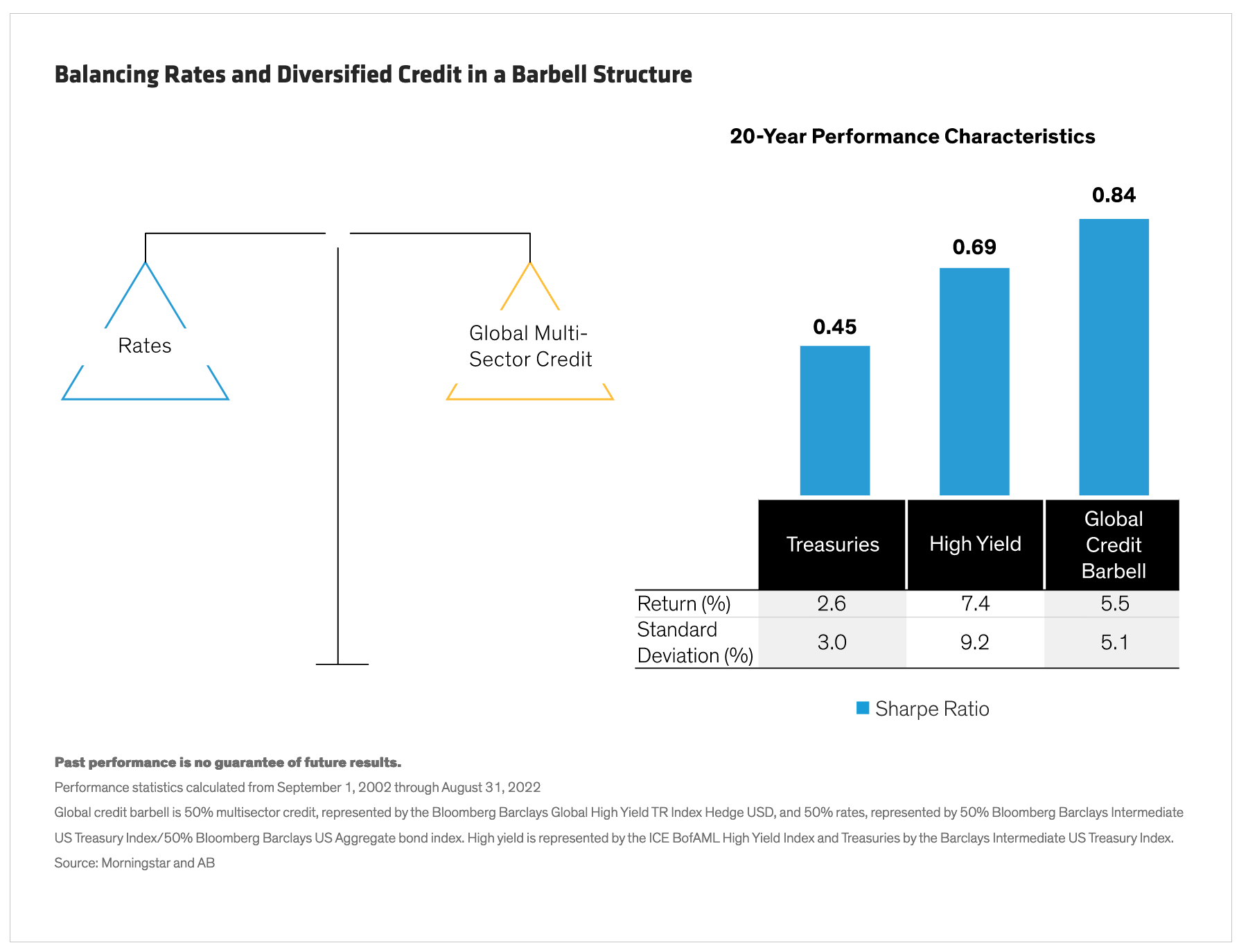

A Barbell of Rates and Credit Exposure

Pairing high-quality bonds with global multisector credit in a risk-balanced allocation creates an effective credit barbell that can generate efficient income throughout the market cycle.

How does this approach work? Historically, there’s a negative or low correlation between high-quality core bonds and high- yield bonds. When the price of one goes up, the other tends to go down, keeping the portfolio value relatively stable. Meanwhile, both sides of the barbell generate income. In our view, a credit barbell with global multisector bonds on one side and core bonds on the other embodies an efficient income portfolio.

Over the past 20 years, a simple credit barbell, split evenly between core bonds and global multi-sector credit, has delivered a higher return than a rates-only portfolio, as represented by Treasuries, and much less risk than a credit portfolio, represented by high yield. Together, these attributes produce the highest risk-adjusted return of the three approaches, with a Sharpe Ratio of 0.84 (Display).

Income—with a Dose of Growth Potential

Income investors who want more growth potential might consider bringing stocks into the mix. However, a traditional equity allocation lowers a portfolio’s yield and increases risk in exchange for that growth. Investors looking to add growth without sacrificing income should consider global high-dividend stocks, global real estate, and EM equities as building blocks with growth potential.

These investments have supplied high income, strong total return and diversification benefits over the long run. While these asset classes increase potential growth and deliver income, they also have more risk than the barbell structure, so investors should ensure that adding these assets to a portfolio aligns with their risk preferences.

We believe investors can get the efficient income they need by combining global multisector credit and core bonds in a balanced credit barbell. This strategy also can incorporate building blocks with more growth potential to suit individual needs and risk tolerances.

About the Author Brian Resnick, CFA

Brian Resnick, CFA

Brian Resnick is Director and Senior Investment Strategist for Fixed Income and Multi Asset. Prior to joining AB, he was a vice president and account manager at PIMCO, where he worked closely with financial intermediaries serving the private wealth marketplace. Previously, Resnick was a director of institutional services at Lord Abbett, working with institutional investment consultants, foundations and sub-advised funds-of-funds. He has been an investment professional since 2004. Resnick holds a BS in economics from Carnegie Mellon University and an MS in financial engineering from Baruch College, and is a CFA charterholder. Location: New York

Copyright © AllianceBernstein