Dev Chakrabarti| Co-CIO—Concentrated Global GrowthJames T. Tierney, Jr.| Chief Investment Officer—Concentrated US Growth

With the world facing inflationary and geopolitical hurdles, economic growth is poised to slow. In this environment, investors in growth stocks must identify companies with the right features to overcome headwinds to earnings.

Equity markets are coping with multiple challenges. Russia’s invasion of Ukraine has added oil to the inflationary fire and most central banks are tightening monetary policy to quench the flames. Given the fragility of the post-pandemic world economy, fears are mounting that efforts to combat inflation could lead to a GDP growth slowdown, stagflation or worse.

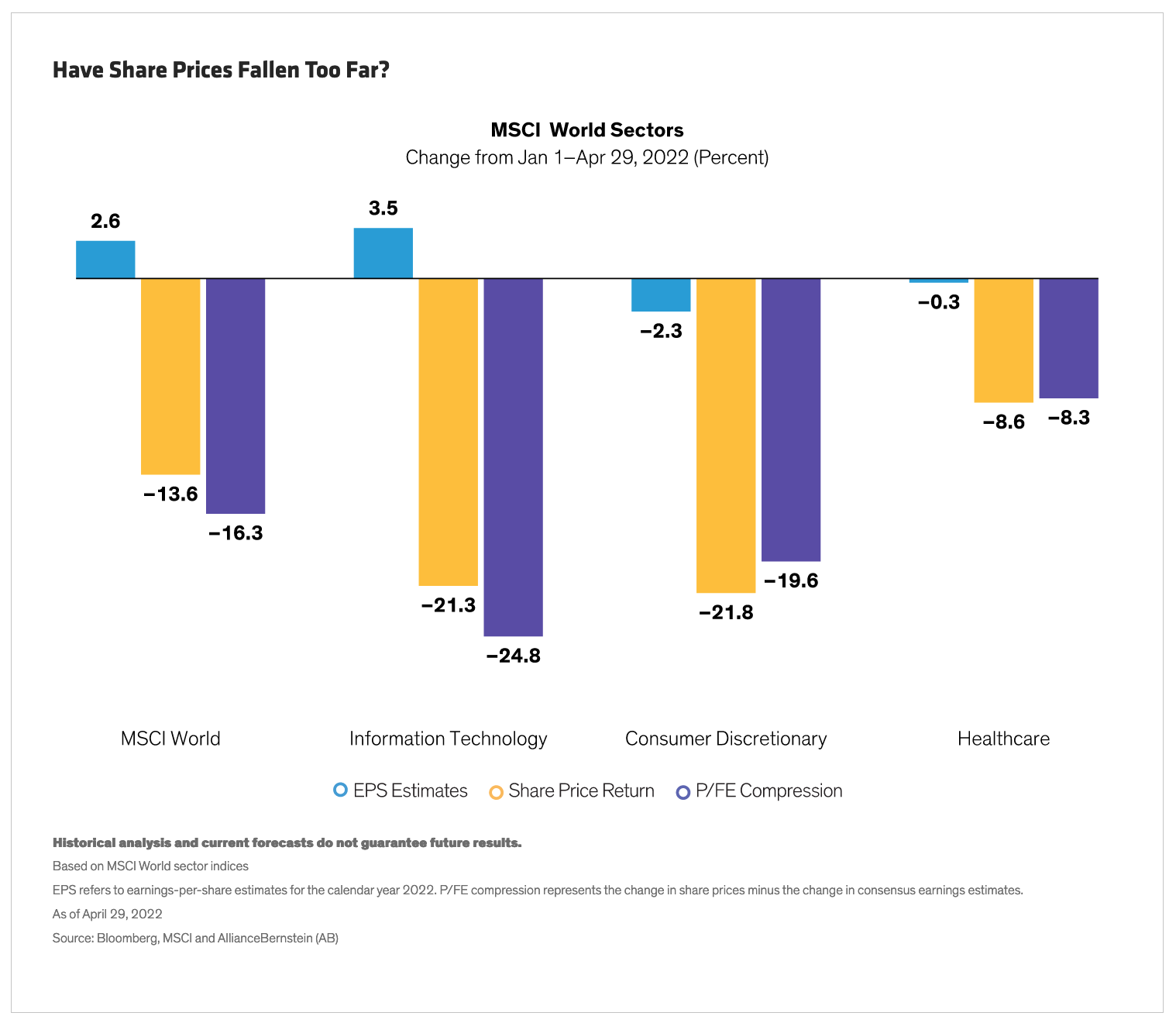

Shares in many sectors have been hit hard. Yet our research indicates that in some cases, sharp declines have dramatically exceeded the change in consensus earnings estimates. For example, the MSCI World Information Technology Index fell by 21.3%, while earnings estimate revisions for the sector advanced by 3.5%, representing a –24.8% difference between the two (Display). In the consumer-discretionary sector, the delta was –19.6%.

But aren’t valuations in growthy sectors still high? We agree that sectors such as technology and consumer discretionary aren’t especially cheap at 23.4x and 20.4x price/forward earnings, respectively, at the end of April. And rising interest rates will pressure multiples of higher-growth stocks. However, the gulf between share declines and earnings estimates suggests that select companies have been unfairly punished in the recent volatility. To find those with solid earnings prospects and attractive valuations, here’s what active investors should look for.

Find Companies with Their Own Growth Drivers

Investors can’t depend on cyclical growth these days. And China’s role as a driver of global economic growth is in being challenged amid COVID-19-related shutdowns. But some business trends are more resilient to a slowdown, especially those that benefit from long-term secular growth trends with long runways.

Consider the cloud in the technology sector. Companies around the world and across sectors are migrating data to the cloud. This need is becoming more acute as labor costs and security concerns grow, and it’s unlikely to be derailed by an economic slowdown. Companies like Microsoft, which are integral to the cloud migration, are likely to benefit from this shift, in our view.

Look Beyond a Company’s Home Base

The location of a company can be misleading. In Europe, where the economy and consumer spending are relatively weak, some companies don’t depend on regional customers and benefit from trends overseas. For example, US infrastructure spending is continuing despite growth pressures, and some non-US companies have a role to play in major projects. Ashtead, a UK equipment-rental company, derives most of its income from the US and benefits from tight supply in equipment, which is accelerating demand for rentals.

Identify Beneficial Post-COVID-19 Trends

Travel, leisure and retail are among the industries likely to enjoy a boost from post-pandemic pent-up spending. Catering companies are a good example. Many food services companies got hit hard during the pandemic, as contracts were lost to a shutdown of business, education, and sports and other events. As more people return to offices and live events return to favor, demand for outsourced catering services is rising. Companies like Compass Group, a UK-based contract caterer, should benefit from these trends.

Avoid Leverage

Companies with heavy debt burdens could be vulnerable if growth slows while interest rates rise. The low-rate environment of recent years encouraged companies to take on additional debt as the cost was so low. But as the pendulum swings back, lower leverage is back in vogue. We believe companies with solid growth drivers and low debt levels should command a premium.

Put Management Under the Microscope

As the macro environment creates new micro challenges for businesses, skilled management will be especially valuable to make the right strategic decisions.

Remember Pets.com? It was a poster child for the indulgences of the late 1990s, when companies squandered IPO proceeds on advertising to build a brand. To a degree, a similar worry exists today, given the surplus of money sloshing around in recent years. In biotech, for example, some smaller clinical trial providers are under pressure amid concerns that funding will dry up. But quality management teams don’t chase business fads like Pets.com. IQVIA, a data analytics provider to the life sciences industry, is a case in point. The company’s CEO recently said IQVIA will scrutinize potential new business for viability rather than welcome any client that walks through the door. Management commitment to disciplined and sustainable business practices is an essential ingredient for success in today’s more challenging macro backdrop.

Following these guidelines can help equity investors identify business models and competitive advantages that can withstand heightened external pressures. Companies that are profitable today and can maintain that profitability are more likely to withstand the effects of rising interest rates, which tend to push down share prices of stocks that have more cash flows coming in the distant future. Eventually, when volatility subsides, we believe markets will refocus on fundamentals and give credit where it is due to companies that can deliver growth against the odds.

The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.

About the Authors Dev Chakrabarti

Dev Chakrabarti

Dev Chakrabarti is a Senior Vice President and Co-CIO for Concentrated Global Growth. Prior to joining AB in December 2013, he was a portfolio manager/analyst on the global equity research and portfolio-management team at WPS Advisors. Chakrabarti joined W.P. Stewart in 2005 as a member of the European equity research and portfolio-management team, and moved to New York in 2008 to focus on global portfolios. Earlier in his career, he worked as an M&A analyst at Merrill Lynch, a financial analyst at Unilever and an equity analyst at J.P. Morgan Securities, where he specialized in European technology stocks. Chakrabarti holds a BSc (Hons) in economics from the University of Bristol and an MSc in finance from London Business School. Location: London

James T. Tierney, Jr. is Chief Investment Officer of Concentrated US Growth. Prior to joining AB in December 2013, he was CIO at W.P. Stewart & Co. Tierney began his career in 1988 in equity research at J.P. Morgan Investment Management, where he analyzed entertainment, healthcare and finance companies. He left J.P. Morgan in 1990 to pursue an MBA and returned in 1992 as a senior analyst covering energy, transportation, media and entertainment. Tierney joined W.P. Stewart in 2000. He holds a BS in finance from Providence College and an MBA from Columbia Business School at Columbia University. Location: New York