by Avi Lavi, Chief Investment Officer—Global and International Value Equities, AllianceBernstein

Value stocks outperformed through mid-February as investors repriced expensive growth stocks. Now, mounting inflation and rising interest rates are creating conditions for a broader value recovery, particularly for companies that have solid business fundamentals.

Style return patterns have been erratic over the last year. During 2021, returns of global value and growth stocks flip-flopped, and both cohorts ended the year with similar gains. Then, in the January 2022 sell-off, value stocks outperformed by a wide margin. The MSCI World Value Index fell by 0.6% this year through February 15, in US-dollar terms, while the MSCI World Growth Index dropped by 10.1%.

Inflation is the game changer. With investors and central banks now acknowledging that inflation will stay higher for longer than initially expected, interest rates are poised to continue rising. This should be beneficial for value stocks, even as it raises challenges for equity investors. Rising rates tend to compress valuation multiples of all stocks, but growth stocks are particularly vulnerable, while value stocks are generally more resilient.

Big Value Discount Persists

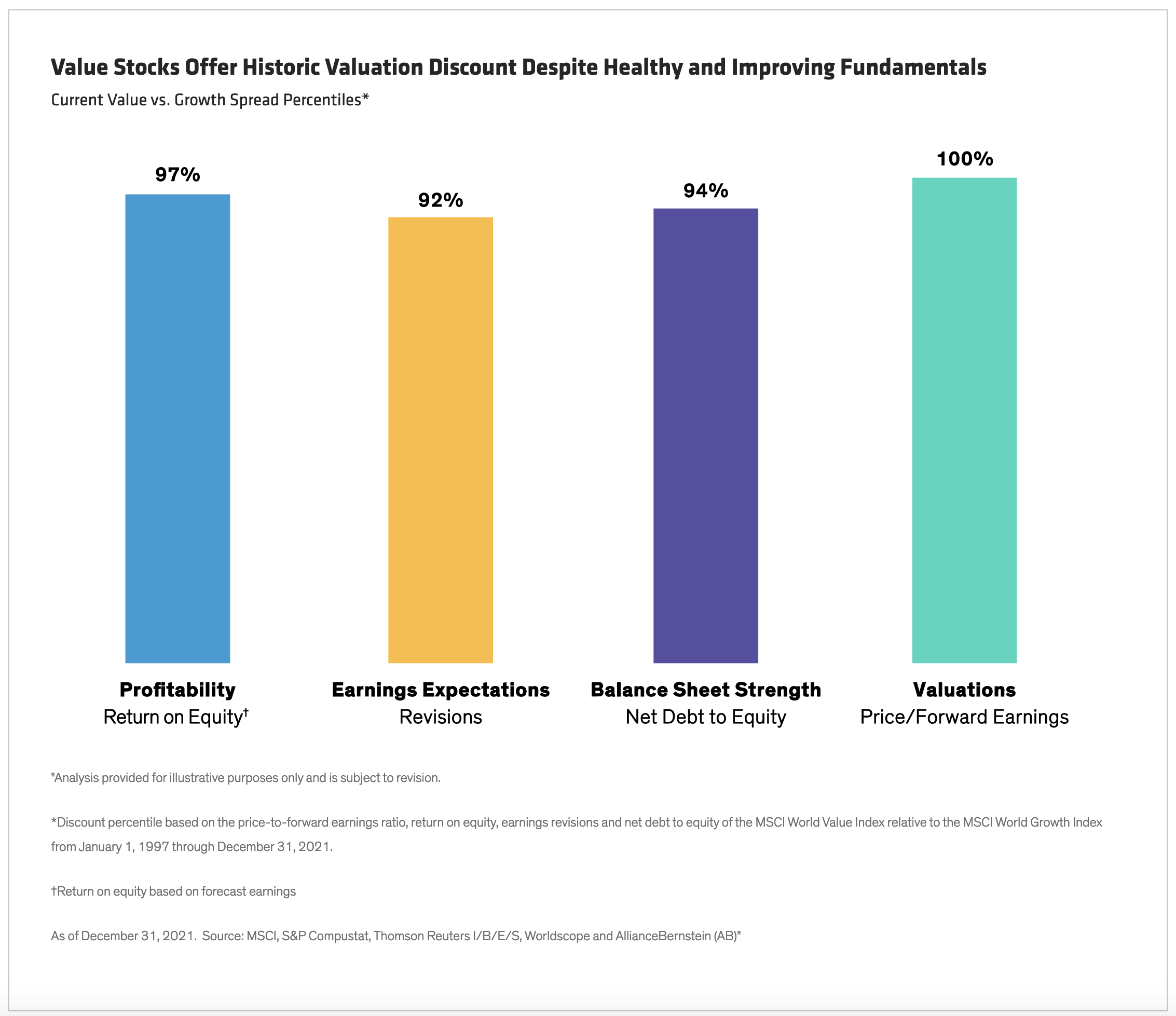

Despite the recent outperformance, value stocks still trade at a near record discount to growth peers. By the end of January, the MSCI World Value’s price-to-forward-earnings ratio was 50% lower than that of the MSCI World Growth. Investors might think this discount implies that value stocks are impaired. In fact, three important indicators—profitability, earnings expectations and balance sheet strength—show that value stock fundamentals rank near historic highs relative to growth stocks (Display).

In recent years, multiples of growth stocks have benefited from the falling rate environment as well as investor demand for high-flying growth companies. Many of these companies have long-term potential but little in the way of current cash flows. This, together with fears of a prolonged economic slump, fueled a massive valuation gap between growth and value stocks.

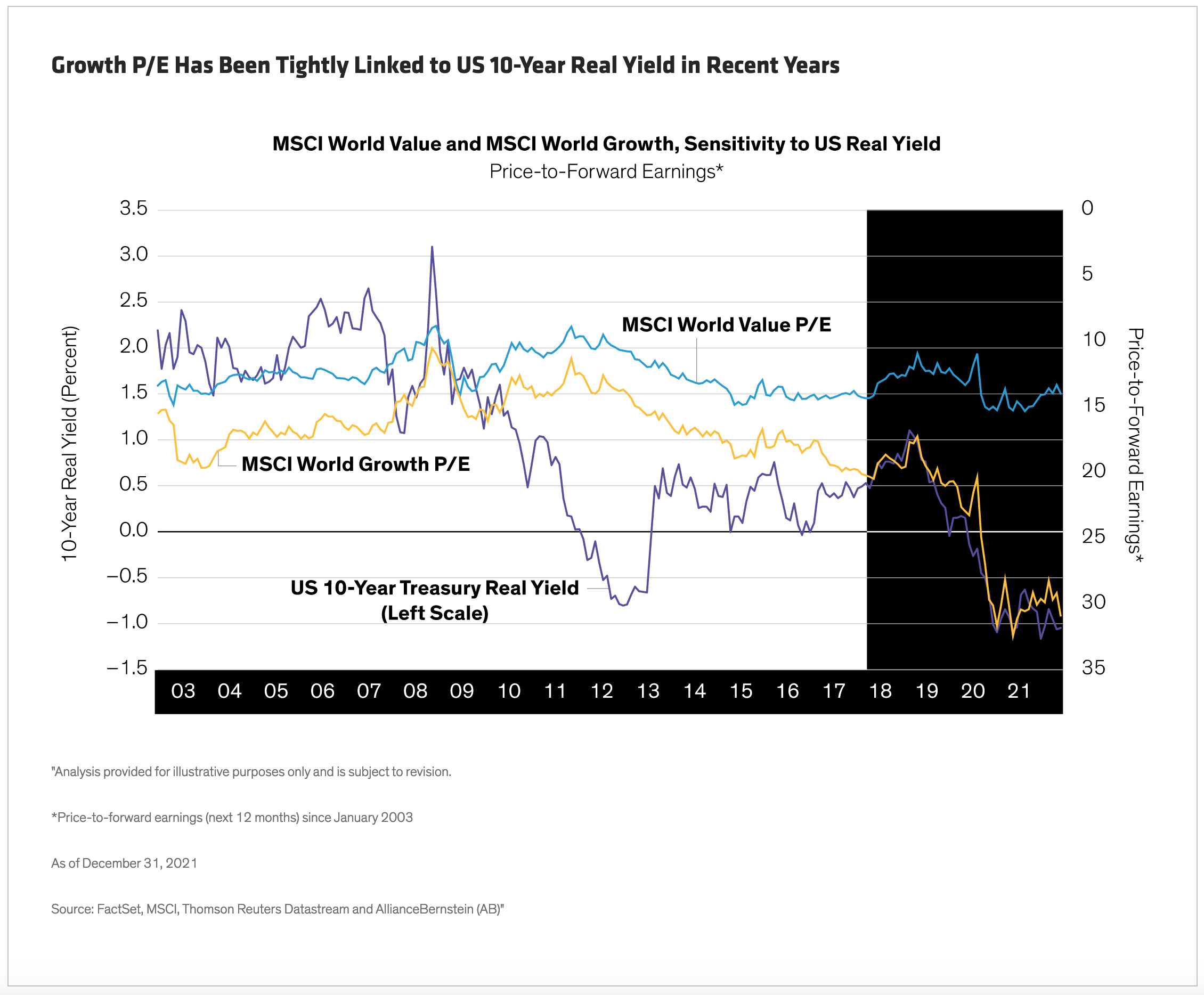

Rising Rates Should Turn the Tide

These trends are ripe for reversal. Since 2019, valuations of growth equities have been tightly linked to the real yield of the 10-Year US Treasury. As real yields fell—and even turned negative during the pandemic—growth stock valuations rose in near lockstep, shown in this display as a declining yellow line against an inverted price-to-forward-earnings (P/E) axis. Over the same period, valuations of global value stocks were relatively stable (Display).

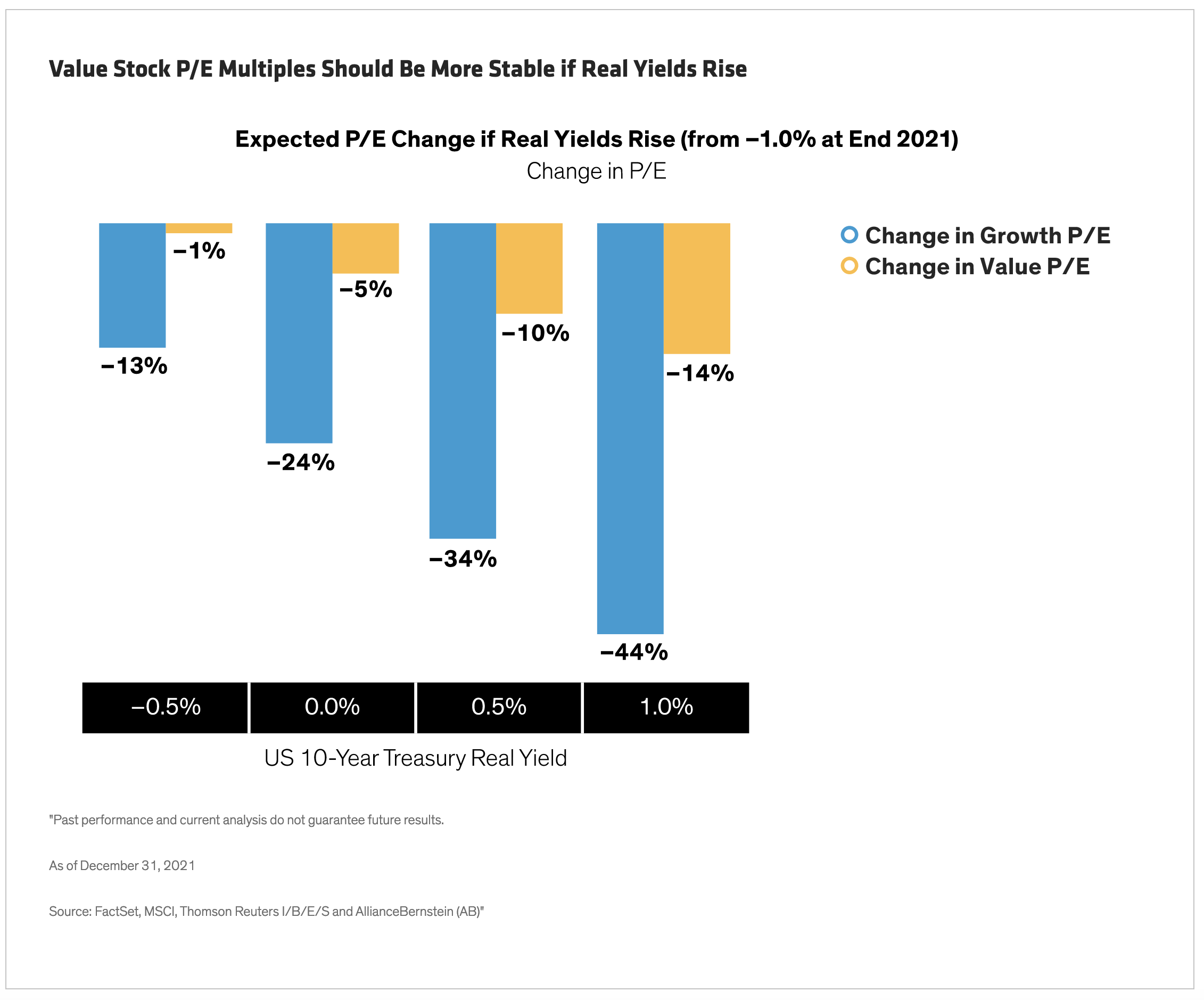

As a result, we expect rising rates to have a disproportionately large impact on valuations of expensive growth stocks. This reversal is already underway in early 2022. In contrast, our research suggests that value P/Es ratios would compress more modestly. For example, if real yields reach 0.5% (from –1.0% at the end of 2021), growth P/Es would fall by 34%, while value multiples would compress by 10% (Display).

Of course, some growth stocks will generate earnings growth of at least 30% to compensate or offset for a multiple decline of 30%, but most will not. But for value stocks, this hurdle is much lower. We expect many value companies will generate earnings growth to overcome a 10% multiple compression and outperform.

Be Selective and Diversify

Investors must be selective. If value stocks stage a big recovery, it won’t be enough to simply pile into sectors such as financials and energy that are large components of the value universe. Concentrating into just a few high-octane value sectors is an unnecessarily risky strategy, in our view. Value opportunities can be found today across a wide range of industries. In an environment of macroeconomic uncertainty and market volatility, diversifying exposure makes sense.

In any sector, investors should look for value stocks with solid and sustainable cash flows. Attractively valued candidates with robust-but-misunderstood businesses and sturdy balance sheets will be best placed to deliver strong performance as the inflation wave buoys stocks that have long been out of favor. For investors concerned about higher inflation and interest rates, initiating or increasing exposure to value equities can provide access to stocks that should benefit in this environment. And since value stocks are still very cheap by historical standards, it’s not too late to capture the recovery potential and add an important element of diversification to your allocation.

The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.

About the Authors

Avi Lavi was appointed Chief Investment Officer of Global and International Value Equities in March 2016 and has also been Portfolio Manager for Global Research Insights since May 2016. He has been a member of the Cross Border team since early 2012. Previously, Lavi served as co-CIO of Global Value Equities (since July 2014) and global director of Value Research (since early 2012). From 2006 to 2012, he was CIO of UK and European Value Equities, and director of research for UK and European Value Equities from 2000 to 2006, during which time he helped establish AB's first research operation based outside the US. Lavi joined the firm in 1996 as a research associate for utilities and expanded his coverage in 1998 to include oil and gas, covering these industries on a global basis. He subsequently became a senior analyst and sector leader for energy research. Lavi was previously an assistant controller at the State of Israel Economic Offices in New York. Prior to that, he was an accountant with Kesselman & Kesselman, PwC's Israeli affiliate. Lavi holds a BA in accounting and economics from Bar-Ilan University in Israel and an MBA from New York University. Location: London

Copyright © AllianceBernstein