by Yasmin Meissner, Co-Head of Sustainable Investing, Multi-Asset Strategies & Solutions, and Alastair Bishop, Head of Sustainable Core Investing, Fundamental Equities, Blackrock

Achieving “net zero” by 2050 will require a shift in the global energy mix, from both a supply and consumption perspective. This has implications for portfolio allocations and alpha generation but there are diverse perspectives on the emergent risks and opportunities related to this shift. We recognize leveraging those diverse perspectives, deep market expertise, and collaborative intelligence across multiple disciplines are essential to forming differentiated investment insights. As such, we convened a group of energy experts from BlackRock’s active investing platform across multi-asset, equities, fixed income, and alternatives to discuss the intersection of energy, investing, and ESG.

Contrary to the notion that tackling climate change comes at a net cost to the global economy, we expect that mitigating climate-related damages will help prevent economic deterioration and improve risk-asset returns. We see the “green” transition to a carbon-neutral world rewarding companies, sectors and countries that adjust and penalizing others.

We therefore advocate a nuanced approach to investing in both traditional oil and gas and renewable energy companies, with opportunities and risks varying over different time horizons. We note that commodity fundamentals play an important role at the macro level, while the unique asset portfolios and quality of individual companies’ transition plans are essential at the micro level.

Powering ahead

Traditional energy has been an unloved sector in recent years. 2020 was particularly challenging as COVID-19 lockdowns drove the sharpest decline in oil demand since World War II. While the rebound in oil demand and associated performance of energy stocks has lagged the broader market recovery, we believe short- to medium-term demand for oil will recover as the global economy returns to “normal”. We also note that Chinese demand has not yet peaked, and demand from India is expected to grow as its economy industrializes and its population grows.

From a supply perspective, we note that overinvestment in shale in the last decade and rising investor focus on the energy transition has created pressure on oil companies to limit reinvestments and pay cashflows to shareholders. This has meant that supply remains limited even as demand is expected to grow. This imbalance may create a positive tailwind for oil companies over the medium-term, despite the clear long-term structural challenges facing oil companies.

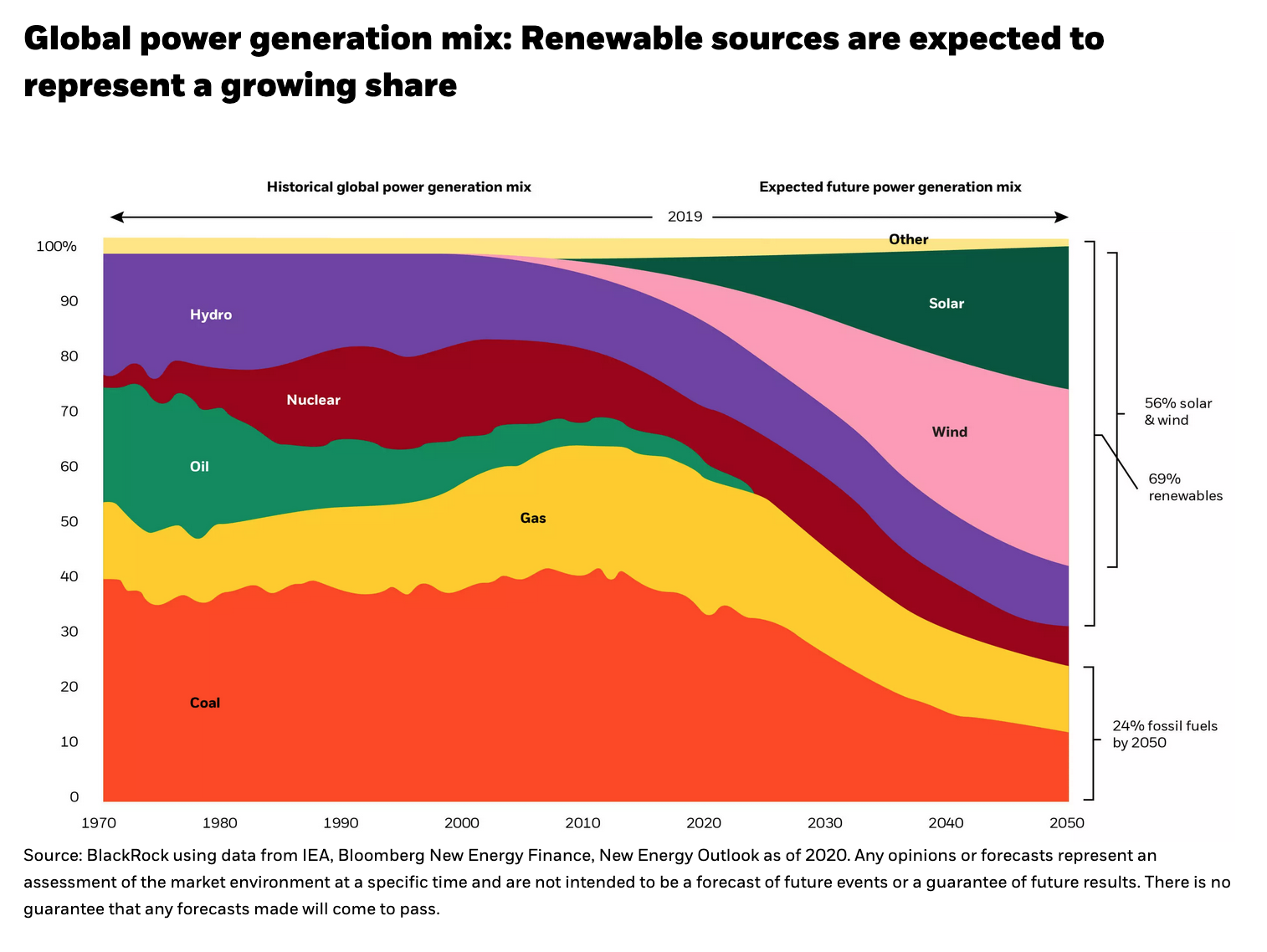

Most participants in our discussion agreed demand for oil is likely to peak in the current decade while demand for renewable projects will continue to grow. Importantly, we expect technological innovation to increase the scalability and reduce the cost of renewable energy sources over time. As alternative energy sources become more affordable, we expect demand for traditional energy to wane considerably, though not disappear.

From deliberating the supply/demand outlook, the dialogue turned to market dynamics. Renewable energy stocks posted strong returns in 2020, especially in the run up to the US Presidential election. Performance in 2021, however, has reversed with renewables underperforming traditional energy. Does this mean that the Paris-aligned scenario has already been priced into the market? We note that performance of traditional vs. renewable energy can be influenced by multiple drivers: the macroeconomic backdrop, policy, technological innovation, and valuations all play a role. Participants agreed that recent divergence can be largely attributed to the value vs. growth factor dynamic that has played out in markets this year. In other words, we believe traditional energy stocks have benefitted from the rotation towards value and that the short-term underperformance of renewable energy is dominated by its exposure to the growth factor rather than sector-specific concerns.

Tracking the transition

We anticipate oil and gas will play a role – albeit a significantly more limited one – in a Paris-aligned world, coexisting with renewable energy sources as well as decarbonization technologies. And we are not the only ones. A growing number of traditional energy companies have signaled an adaptation of their business models and developed decarbonization plans, which highlights they too anticipate a material change in the energy mix and recognize the need to adjust in order to ensure their long-term value proposition. However, the path to decarbonization is not necessarily linear. Some transitions will require significant upfront investment that would be associated with higher emissions in the near-term – think of building new turbines as an example here. As all energy companies assess the risks and opportunities unique to their business operations and decide where to invest their resources, investors play an important role in allocating capital.

We also observe that European and US traditional energy companies are taking divergent approaches: European companies have been more likely to invest in renewable energy projects while their American counterparts have generally focused on reduction of carbon intensity associated with oil projects. Valuations reflect that growing competition for renewable projects has made them more expensive, drawing some energy investors towards US oil and gas companies that are positioned to benefit from near-term tailwinds.

There is indication, however, that US companies are reshaping their business models and shifting their capital allocation plans to low-carbon opportunities, including renewables. Some of this has been in response to shareholders’ increasing interest in understanding the long-term risks and opportunities of oil and gas companies in the context of the energy transition.The proposals voted on, and the outcome of those votes, at the annual general meetings of oil and gas companies in the 2020-2021 proxy year illustrate this.

BlackRock believes energy companies can play an integral role in unlocking the full potential of the transition to a low carbon economy, but they must be prepared to adapt, innovate, and pivot their business models. This underscores the need to remain engaged with management and assess company-specific plans. As a long-term investor on behalf of our clients, our BlackRock Investment Stewardship (BIS) team encourages energy companies to have appropriately factored climate risk into their strategy development and be able to articulate a long-term value proposition to shareholders. (For a more detailed look, see BIS’s published vote bulletins.)

Conclusion

At BlackRock, we empower better investment decisions by viewing sustainability as a persistent – and increasingly important – driver of returns. Our active investment teams seek to identify ESG issues that expose potential risks and uncover idiosyncratic opportunities. This demands that we look across multiple time horizons, geographies, and specific companies, rather than relying on broad assumptions at the industry level. Discussions like the one we highlighted here stem from our core belief in the dual benefit of doing good for the environment and doing what’s best for our clients’ portfolios. Visit our sustainable investing hub to learn more about our endeavor to deliver greater ESG outcomes, portfolio resiliency, and durable alpha over time.

Copyright © Blackrock