by Jennifer DeLong, AllianceBernstein

As people live longer, they need their retirement income to last longer, too. Plan sponsors are increasingly seeking solutions that provide enough retirement income for the most participants, but powerful forces can sidetrack progress toward that goal. Even if participants make years of steady contributions and maintain thoughtful asset allocations, an ill-timed market downturn or change in interest rates when approaching retirement can be devastating.

But there’s an effective solution to these pitfalls. It starts with securing a guaranteed income stream earlier—and systematically—while still working, and not shifting the bulk of savings to a purchase at a single point in time on the threshold of retirement.

Avoiding (Or Embracing) Risk with the Help of Time

People can’t predict market or interest-rate movements, but they can plan and protect against uncertainties. The goal is to minimize the volatility of future income, and the key is to secure it by purchasing guaranteed income a little at a time.

Steadily buying guaranteed income, ideally starting 10 to 15 years before retirement, does three important things. First, it gradually ensures an income level by locking it in, which eliminates exposure to a narrow set of market conditions (especially poor ones). Next, it adds downside protection, which allows for more equity exposure—and growth potential—closer to retirement, when most investors typically seek to reduce equities. Finally, it delivers real-time feedback to participants well before retirement, so they have the time to plan and adjust.

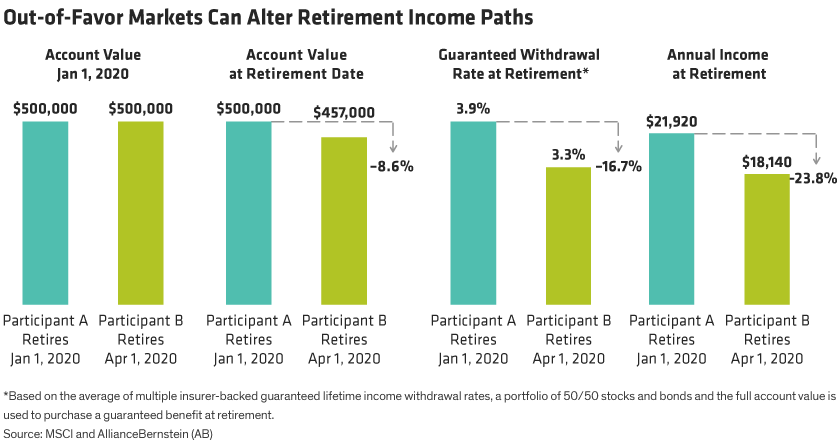

Retirement assets also face sequence-of-returns risk, when account balances suffer losses in participants’ final working years. Without a secured income, sequence risk is magnified by point-in-time risk, which leaves behind a smaller stake to buy guaranteed retirement income at the pivotal moment right as retirement arrives.

Point-in-time risk was especially painful for investors amid the more iconic market downturns, such as the global financial crisis and most recently during the early months of the COVID-19 pandemic. As markets dropped, they took retirement savings down with them, leaving a lot less participant buying power while guaranteed rates dropped, too—lowering guaranteed income for life (Display).

Avoiding the Interest-Rate Timing Game

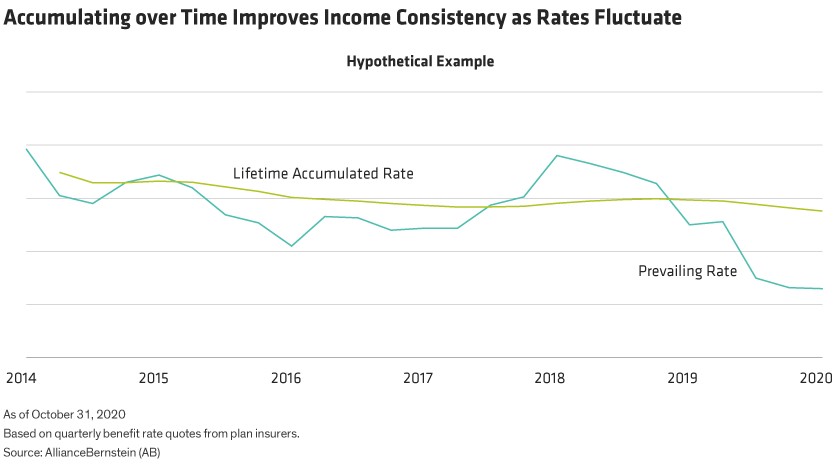

Interest rates are the cornerstone of just about everyone’s income calculus, and they’re alarmingly unpredictable. By purchasing guaranteed income systematically—across different rate environments—participants avoid risking a lower rate (and lower income), which frequently happens in a one-and-done purchase. That risk is made worse when lower guaranteed income rates correspond with a sell-off in asset prices.

Systematic purchasing of guaranteed income works much like dollar cost averaging (DCA), which entails buying investments at different prices gradually over time. In the case of retirement income, participants purchase insurer-backed income guarantees at different prevailing rates over time. The advantage: income for life is based on a cumulative rate, rather than rates at a single point (Display).

‘Steady as You Go’ Also Builds Trust

Protecting retirement income from market and interest rate setbacks is a strong start, but the nature of buying insurer-backed income offers benefits, too.

For example, buying in to guaranteed income over time also builds trust and confidence. Emotion-based biases seem to get swept away: for example, a 5% annual allocation to gradually buy a guaranteed income solution may feel more psychologically and financially feasible than the prospect of cashing out and annuitizing a full account balance at 65.

It also helps that the buying-in process rings familiar with other programs participants use. Many participants rely on periodic investing into their DC plan, and they trust how target-date portfolios slowly de-risk as they approach retirement. Guaranteed income solutions, especially those offered as in-plan QDIAs, are aligned at heart with these other time-tested savings regimens.

For a worry-free retirement, we believe that planning guaranteed income for life makes sense. Methodically securing that income during the working years is even more prudent, because it resolves common tail risks: experiencing poor markets near or at retirement and “living too long.” With these problems in check, and depending on the type of income option, other impactful issues can be addressed, like preserving retirement account value upon a retiree’s death or benefiting from market gains.

Jennifer DeLong is Managing Director, Head—Defined Contribution at AB.

Andrew Stumacher is Product Director—Custom Defined Contribution Solutions at AB.

Howard Li is Research Analyst for Multi-Asset Solutions at AB.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.

This post was first published at the official blog of AllianceBernstein..