by Talley Léger, Invesco Canada

The answer to that question depends on the reason why interest rates are rising. If it’s because real economic growth is picking up, that should be good for stocks through the earnings channel. If it’s because inflation is getting out of control, that should be bad for stocks through the valuation channel.

While I wouldn’t rule out an inflation “scare” altogether, I believe such concerns may ultimately prove overblown. In my view, the selloff in stocks is simply a pause that refreshes, not a sinister change of trend.

The U.S. Federal Reserve is committed to low policy rates for longer

In my opinion, the lagged impact of past interest rate cuts has yet to fully work its way through the system, with positive knock-on effects for stocks.

In fact, history argues that higher bond yields aren’t something we should seriously worry about until early 2023. In Figure 1, the dark blue area represents changes in bond yields (inverted and pushed forward by two years) and the light blue line captures fluctuations in stock prices over the past decade.

Figure 1: The lagged effect of past interest rate cuts raises the floor under stocks

Sources: Bloomberg, L.P., FRED, Invesco. 1/31/21. Notes: The year-over-year percentage change in U.S. government bond yields has been inverted and advanced by two years. A lower discount rate in the present points to higher corporate cash flows in the future. An investment cannot be made in an index. Past performance does not guarantee future results.

Sources: Bloomberg, L.P., FRED, Invesco. 1/31/21. Notes: The year-over-year percentage change in U.S. government bond yields has been inverted and advanced by two years. A lower discount rate in the present points to higher corporate cash flows in the future. An investment cannot be made in an index. Past performance does not guarantee future results.

Moreover, the U.S. Federal Reserve (Fed) has renewed its commitment to keeping interest rates low for longer, thereby defending this fledgling economic recovery, while allowing the U.S. dollar to flatten, inflation expectations to rise, and the bull market in stocks to continue.

To be clear, I do acknowledge some intentional, near-term reflationary pressures from policymakers and see a little bit of inflation as a good thing, meaning deflation risks are subsiding.

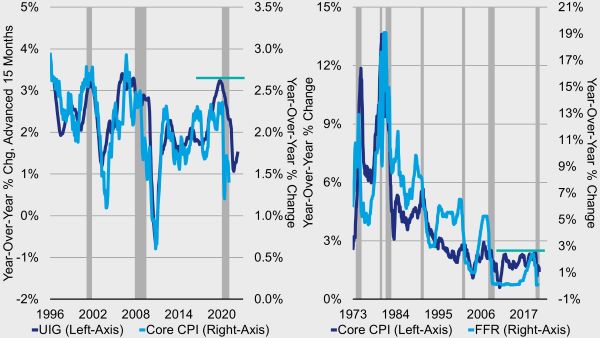

Indeed, leading indicators of core inflation suggest underlying consumer prices are expected to recover modestly through 2021, but undershoot the Fed’s 2% average inflation target (Figure 2).

In turn, below-plan inflation trends imply the Fed should stay dovish and policy rates may remain low in an effort to push inflation above target for some time to compensate.

Figure 2: Leading economic and inflation indicators imply the Fed should stay dovish and policy rates may remain low

Sources: Federal Reserve Bank of New York, FRED, Invesco, 1/31/21. Notes: CPI = Consumer Price Index. Core = All items less food and energy. UIG = Underlying inflation gauge. The UIG captures sustained movements in inflation from information contained in a broad set of price, real activity and financial data. The UIG estimates trend inflation, derived from a large number of price series in the CPI as well as macroeconomic and financial variables. FFR = U.S. Federal funds rate. Dark gray areas denote NBER-defined U.S. economic recessions.

Sources: Federal Reserve Bank of New York, FRED, Invesco, 1/31/21. Notes: CPI = Consumer Price Index. Core = All items less food and energy. UIG = Underlying inflation gauge. The UIG captures sustained movements in inflation from information contained in a broad set of price, real activity and financial data. The UIG estimates trend inflation, derived from a large number of price series in the CPI as well as macroeconomic and financial variables. FFR = U.S. Federal funds rate. Dark gray areas denote NBER-defined U.S. economic recessions.

Disinflationary pressures remain

Looking further ahead, long-term disinflationary pressures remain in place — interest rates could stay pinned by the Fed, a global savings glut, an aging population, productivity-enhancing technological innovation and the “Amazonification” effect, which refers to consumers’ present ability to get lower prices from online retailers like Amazon.

The bottom line is that I believe low interest rates for longer are the starting point for the “recovery” trade that I expect to continue for some time. Historical recovery trends have typically included a modestly positively-sloped yield curve, flat to slightly weaker U.S. dollar, stronger commodity prices, corporate bond outperformance relative to government bonds, and stock market outperformance relative to government bonds.

This post was first published at the official blog of Invesco Canada.