by James MacGregor, CIO—US Small and Mid Cap Value Equities; Head—US Value Equities, AllianceBernstein

Small-cap US stocks powered back in the fourth quarter after trailing large-caps for several years. Even after the strong recent performance, the recovery may still be in its early stages—particularly for smaller-cap value stocks—as pandemic risks recede and earnings drivers kick in during 2021.

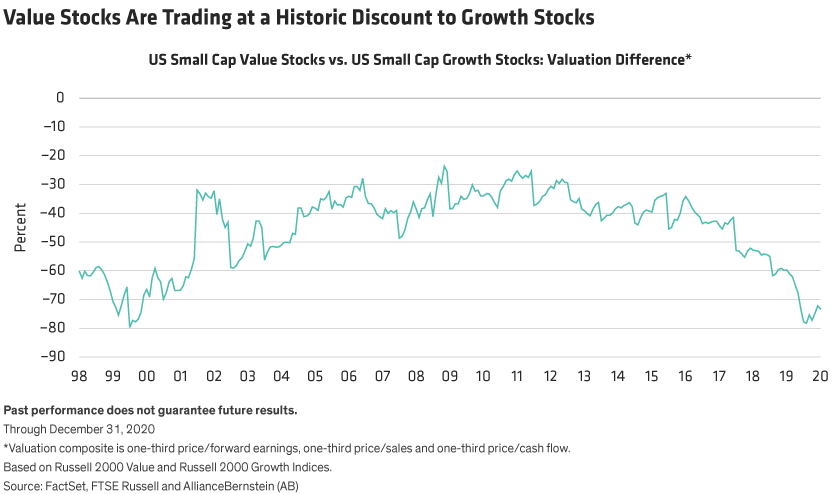

Both small-cap stocks and value stocks have underperformed the broader market by extremely wide margins in recent years. From 2017 to September 2020, the Russell 2000 Value Index of small-cap stocks trailed the Russell 2000 Growth Index by 58% and underperformed large-cap growth stocks by more than double that (Display, left).

Things started to change in the fourth quarter of 2020 (Display above, right). As news of COVID-19 vaccine successes raised hopes of a broader economic recovery in 2021, investors started to move back into stocks that are considered more sensitive to the economic cycle. As a result, US small-cap value stocks advanced by 33% in the fourth quarter, outperforming growth stocks and the broader market.

Is the Small-Cap Value Rally Over?

After such a sharp recovery, have investors missed the opportunity? We don’t think so. By understanding why small-cap stocks underperformed over the past four years and what’s changed, we believe investors can gain confidence in the recovery potential. Since the small-cap slump of recent years was so dramatic, the late 2020 rebound has only recovered a small amount of the underperformance. And there are good reasons to expect smaller, attractively valued companies to do well as the macroeconomic recovery progresses this year.

Growth companies outperformed over the last four years as the challenging economic climate made earnings growth exceptionally scarce. Low interest rates also helped growth companies, which tend to generate cash flows in the more distant future and benefit as lower discount rates make the valuation of those cash-flow streams more attractive today.

Even the uncertainty of the pandemic led investors to continue flocking to larger, growth-oriented companies for their perceived safety. But risk appetites seem to be changing with the improving economic climate, and we believe investors are just beginning to reward smaller value stocks with solid businesses showing real earnings power.

Earnings power helps explain the recovery of small-cap value stocks in late 2020. Earlier in the year, investors shunned these stocks amid fears that they were more vulnerable to the pandemic’s consequences. In fact, many navigated the crisis better than expected. Sales and earnings in many of these companies recovered more quickly than expected after the initial pandemic shutdown panic abated.

Smaller Businesses Adapted Well to COVID-19

For example, as shutdowns began in April, it was feared that small-cap banks’ provisions for bad debts would overwhelm their earnings and perhaps even force them to raise equity. Yet six months later, many of those banks were beating quarterly earnings expectations on lower-than-expected loan losses.

Small value companies have also been more flexible and adaptable to the recessionary environment than expected. Of course, some industries such as restaurants and airlines have faced intense pressure. But in general revenues and profits for consumer cyclicals and industrials, among others, have bounced back better than expected, even though investors gave them no credit for potential resilience during the downturn.

And even with fourth quarter’s beginning of a bounce back, small value stocks are still as cheap as they have been since the height of the tech bubble 20 years ago (Display).

Overcoming the Sum of All Fears

What will it take for small-cap value stocks to close the performance gap? An improvement in risk appetite is key—and the outlook is encouraging. In 2020, investors were mostly concerned about policy risk from the presidential election, the pandemic and the impact of the ensuing recession on corporate profits. All of these are now starting to recede. COVID-19 vaccines are being distributed globally. And company earnings appear to be bouncing back from the worst of the recession. While the year ahead will face many challenges, 2021 is looking like a much better year for humanity and stocks alike.

Even in an improved environment, small-cap value investors must be disciplined and selective. In value, investors seek stocks that have underperformed due to a controversy that creates uncertainty about the sustainability and value of a company’s cash flows—such as a pandemic. The challenge is to correctly identify which companies have been unfairly punished and can eventually show strong and sustainable cash flows, and then determine when to get in position.

For over 25 years through 2016, smaller-cap stocks with attractive price-to-free-cash-flow multiples in the top quartile outperformed the rest of the small-cap market by over 10% per year. But in the last four years, stock prices haven’t followed cash flow, and multiples have contracted for smaller-cap stocks. We believe this is an irrational market reaction that will eventually correct, especially as company fundamentals have continued to improve during this period of underperformance.

Compelling Catalysts for Recovery

In smaller-cap value stocks, we think a combination of strong fundamentals and compelling catalysts spells opportunity. Attractive valuation, based on metrics such as the free cash flow a company generates, is only part of the story—it’s just as important to look deeper into the fundamental story of each company to understand its competitive landscape, business environment and management capabilities. Then, investors should identify a catalyst such as a management change, stock buyback or other improvements that can drive a reassessment of the valuation of the company.

On all these fronts, the journey out of the pandemic will require heightened scrutiny. In many industries, the business environment has been permanently changed and earnings guidance is muddled at best. Investors who develop insightful, independent forecasts can gain an edge on a company’s recovery path.

As the extreme risks of 2020 recede and normalization begins, we think it’s not too late to reassess equity allocations. In fact, in baseball terms, we believe small-cap value stocks have just finished warm-ups and the national anthem, and the real game is just beginning. For investors with appropriate risk appetites, we think increasing exposure to small-cap value stocks can provide access to pent-up recovery potential in an asset class that should thrive as economies heal from the pandemic.

James MacGregor is Chief Investment Officer—US Small and Mid Cap Value Equities; Head—US Value Equities at AB

Erik Turenchalk is Portfolio Manager—US Small and Mid Cap Value Equities at AB

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.

This post was first published at the official blog of AllianceBernstein..