by Daryl Clements, AllianceBernstein

After 2020, a year for the ages, 2021 should bring a mixed bag for the muni market. We expect rates and yields to increase moderately during the year, and munis to remain as resilient as ever, offering select opportunities for active investors.

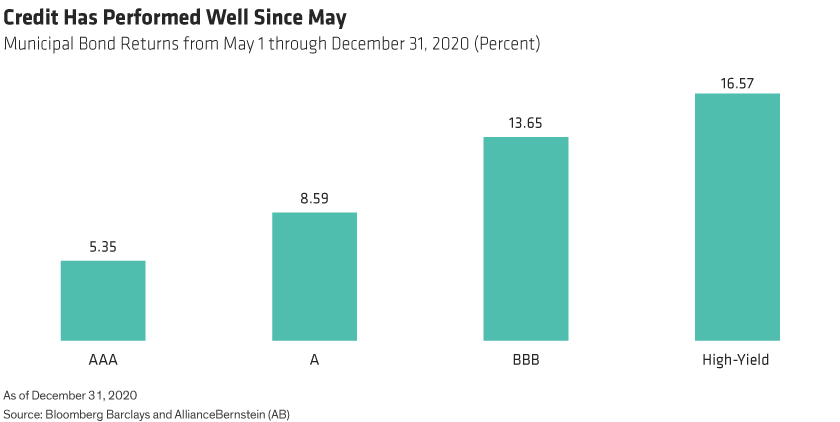

Despite 2020’s many challenges, the Bloomberg Barclays Municipal Bond Index was up 5.2%, with returns that were even more compelling for the second half of the year, across the credit spectrum (Display).

Going forward, favorable conditions should help munis continue to perform well, including helpful monetary and COVID-19 stimulus, ongoing vaccine distribution, better-than-expected tax collections, and a beneficial muni supply picture.

Stimulus and Vaccines Bode Well for Munis

Supportive federal stimulus will likely continue in 2021, keeping the fed funds rate at zero and quantitative easing (QE) in place. The Federal Reserve (Fed) is currently buying $120 billion in securities monthly, split between US Treasuries and mortgage securities. Assuming the Fed stays its course, QE will likely restrain yields from rising to a level that makes the central bank uncomfortable, so we expect any increases in 10-year US Treasury yields to be moderate.

The passage of a $900 billion fiscal stimulus package should help jump-start the US economy. Now that Democrats are the controlling party, more stimulus is expected, and it likely will directly benefit states and municipalities. Moreover, the Democrats’ slim majority puts President-Elect Biden’s proposal for higher taxes in closer reach. If achieved, a higher top marginal tax rate for both individuals and corporations would increase demand for tax-exempt municipal bonds.

Finally, with more COVID-19 vaccines being distributed, a return to normalcy is closer, along with further improvements in employment and tax collections. Although there is still some wood to chop, an extended recovery should lay solid groundwork for continued improvement in municipal credit.

Low Supply Should Support Muni Prices

Muni market supply and demand conditions also contribute to our optimism. During the year, we expect net supply to turn negative as more bonds mature or more bonds than were issued are called away. This creates a scenario with a lot of cash chasing very few bonds, thus supporting bond prices.

State tax revenues have remained surprisingly steady, too. The broad expectation in March 2020 was for tax revenues to drop 25% year over year, but they fell just 1% on average, according to a JPMorgan Chase study.

Moreover, the Fed set up a first-ever municipal liquidity facility to protect all issuers, but only two entities drew from it: the state of Illinois and New York’s Metropolitan Transportation Authority. This speaks to the financial integrity of the thousands of other muni issuers that could have used it but didn’t need to.

Munis Have Survived Tough Times

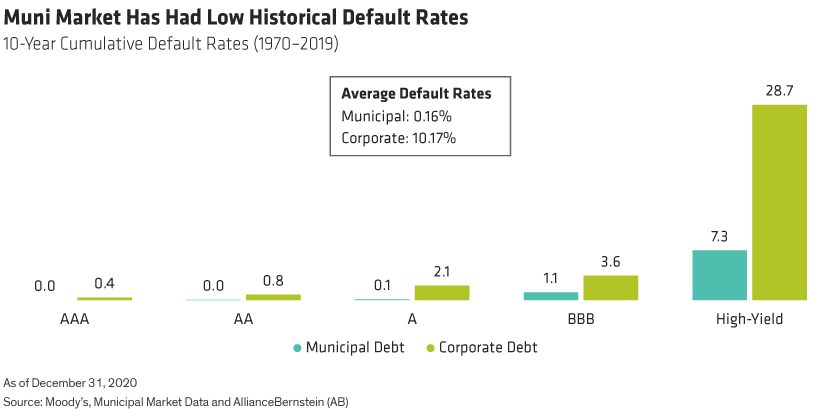

Contrary to dire headlines, muni bond issuers still have the wherewithal to handle the lingering fiscal challenges of COVID-19. And the general financial health of states has been steady—even among those with large debt burdens. It’s no coincidence that default rates remained consistently flat during the pandemic, considering how well they weathered the sometimes-tumultuous half century before it (Display).

Ratings downgrades ticked up in 2020, as we expected, averaging 51% through September 30, compared to 33% for 2019. Yet, downgrades historically have not translated into negative returns. In fact, they often can signal value opportunities for investors who stay alert to them and to the issuer’s underlying fundamentals.

Muni Credit Should Outperform

In this environment, we expect municipal credit—particularly debt rated A and BBB—to outperform higher-rated bonds.

At the pandemic’s start, market participants had expected lower-rated credits to experience more stress. Instead, mid-grade issuers held up especially well throughout the crisis, particularly airports, toll roads and hospitals—buoyed by reserves and continued monetary and fiscal stimulus. These conditions—as well as better-than-expected tax revenues—remain supportive for muni credit.

In addition, yields on AAA-rated munis are still low, and credit spreads remain above pre-pandemic levels. If yields rise, we would still expect muni credit to continue to outperform, since credit spreads will likely narrow as the economy recovers.

Markets and outlooks can change quickly. Investors need to be active and flexible to navigate myriad challenges. Portfolio managers need deep research to unearth opportunities, and state-of-the-art technology to pursue them, in an increasingly fragmented market in which some 80,000 muni bonds trade daily. In our view, the muni market will move toward normal as 2021 progresses, and investors who stay sharp should benefit.

Daryl Clements is Portfolio Manager of Municipal Bonds and Terrance Hults and Matthew Norton are Co-Heads of Municipal Portfolio Management at AllianceBernstein (AB).

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

This post was first published at the official blog of AllianceBernstein..