For global investors looking for strong growth profiles at attractive multiples, the Japanese market merits a fresh look. Portfolio Manager Shuntaro Takeuchi offers his outlook.

by Shuntaro Takeuchi, Portfolio Manager, Matthews Asia

As U.S. equity prices continue their multiple expansion, Japanese equities continue to offer attractive valuations, with considerable upside potential. Disruptive technologies and services in Japan are addressing long-term trends, including an aging population and shrinking labor force. Portfolio Manager Shuntaro Takeuchi discusses these secular growth drivers and shares his views on current investment opportunities.

Why are Japanese equity valuations significantly lower than those for U.S. equities?

For the past 25 years, Japan has traded at a discount versus the U.S., both in terms of price-to-earnings and price-to-book. In the first 15 years of this period, the discount was justified given Japan’s poor return on equity (ROE) and return on invested capital (ROIC). For the past decade, however, the market hasn’t been pricing in the positive changes achieved by Japanese companies. ROE and ROIC of Japanese companies are now within a few points of other markets, and, if you look at median ROIC, Japan was higher than the U.S. and Europe between 2016 and 2018. Although Japan’s profit profile is improving, we have yet to see a multiple expansion. In fact, multiples have shrunken in certain instances—and that’s where we see opportunities.

What are some secular growth drivers in Japan that might be underrepresented in the benchmark MSCI Japan Index?

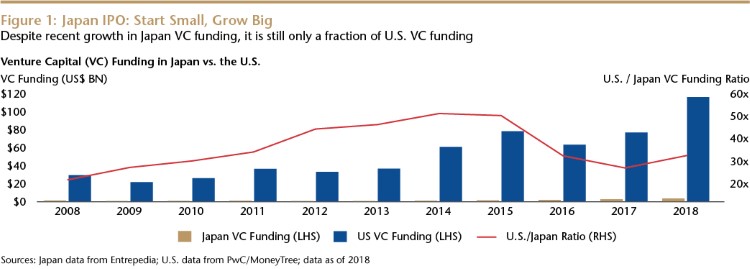

Many index-based investors are missing opportunities in small caps. Japan offers a unique opportunity for investors to access growth at a very early stage, given there are about 70-90 Japanese IPOs each year.

A few factors are behind this environment. Venture capital (VC) funding in Japan totaled $2.5 billion in 2018, approximately one-thirtieth of the U.S. total. For additional context, VC funding in China surpassed $100 billion in 2018. Compared to the U.S. and China, Japanese start-ups are practically forced to go public at a very early stage. IPOs in Japan are often comparable to series B or series C funding in the U.S.

Additionally, the absence of mega-cap high-growth companies in Japan structurally supports Japanese small-cap companies, which could copy what successful start-ups are doing. To the contrary, many of the larger companies in Japan are in legacy, slower-growth areas, and it is the smaller growth companies that take market share from the larger players.

What opportunities can investors find in Japan that aren’t available in the U.S., Europe or emerging markets?

First, compared to Europe and emerging markets, Japan is geared toward technology, industrials, and, to a certain extent, health care. It has a lower exposure to interest-rate sensitive sectors, such as financials, energy and materials. As a result, investing in Japan is essentially participating in the innovation areas of economic activity, not the fluctuation of interest rates.

Second, Japanese small-cap stocks are liquid compared to other international markets. For example, Japan’s small caps trade more than many of the emerging market countries as a whole, and trade more than all frontier markets combined. Furthermore, Japanese small caps as an asset class have a low correlation to the S&P 500 Index.

Third, Japan’s benchmark index, the MSCI Japan Index, has a lower concentration than benchmarks for other international regions, which creates opportunities for active investors.

What can other countries learn from Japan’s experience with an aging population? And what investment opportunities does it create?

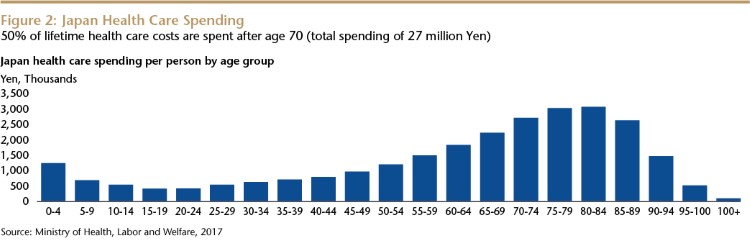

Japan has experienced an aging society earlier than many other countries and 50% of lifetime health care costs are being spent after age 70. With baby boomers now reaching this age, we think companies that tackle the issue of rising health care costs is a growth area and potential investment opportunity. These opportunities range from pharmaceuticals that cure or prevent diseases, to medical devices or equipment for minimally invasive surgeries that enable patients to have shorter hospital stays. It also covers health care platforms that rationalize the marketing costs of pharmaceutical companies.

Japan is also dealing with a decline in labor population, which creates a need for improved labor productivity—especially in white collar jobs. This is an area in which many software and IT service companies are operating, working to improve labor productivity and drive profit growth.

With a new prime minister in Japan, what’s on the horizon from a government policy perspective that might promote economic growth?

We see several positive developments, including Prime Minister Suga’s willingness to expand fiscal stimulus to offset the negative consequences of COVID-19 and boost domestic consumption.

Another positive we’ve seen from the government is its policy flexibility.

The Bank of Japan (BOJ) bought ETFs to provide market liquidity and has the option to buy more. How do you think the BOJ will manage its large ETF portfolio when it comes time to slow down its purchases or wind down its holdings?

When the BOJ said it would double ETF purchases, a key part of the messaging pertained to its option to do so; it did not make an outright commitment to double the amount. Going forward, we think the BOJ can essentially carry out stealth tapering. As long as fundamentals remain sound and the market reflects the earnings potential of Japanese corporate profits, the BOJ can preserve its option to buy ETFs but reduce its pace of purchases. This would happen before outright selling.

How much would a resurgence in global trade benefit Japan? And how much of that benefit is driven by export-related earnings and profits?

From a cyclical perspective, about 60% of Japanese corporate profits come from the export sector. It is a beneficiary when global trade bottoms out and starts to improve. That’s one of the reasons why Japanese equity markets have performed well year-to-date.

Structurally, growth in Japan is driven by both the export sector and the domestic sector. Over the past decade, there has been a 10 percentage-point decline in share of profits from export sector, which has mainly been achieved by profit growth in the domestic services sector. In terms of investments, the Japanese domestic market is still the third-largest market in the world.

What is the case for investing in growth companies in Japan today?

Now is a good time to own Japanese growth equities, in our view. Japan’s market is a beneficiary of the bottoming out of global trade and subsequent improvements. Furthermore, a constant decline of interest rates generally favors growth stocks due to increased profits and multiple expansion. As global investors look for strong growth profiles at attractive multiples, the Japanese market comes into play: Japanese companies are seeing profit growth but haven’t yet seen multiple expansion.

Shuntaro Takeuchi

Portfolio Manager

Matthews Asia