by Kathy Jones, Senior Vice President, Head of Fixed Income Strategies, Schwab Center for FInancial Research

As 2020 draws to a close, most of us will be happy to see it end. From the global pandemic to the large number of natural disasters around the world, it has been a tough year.

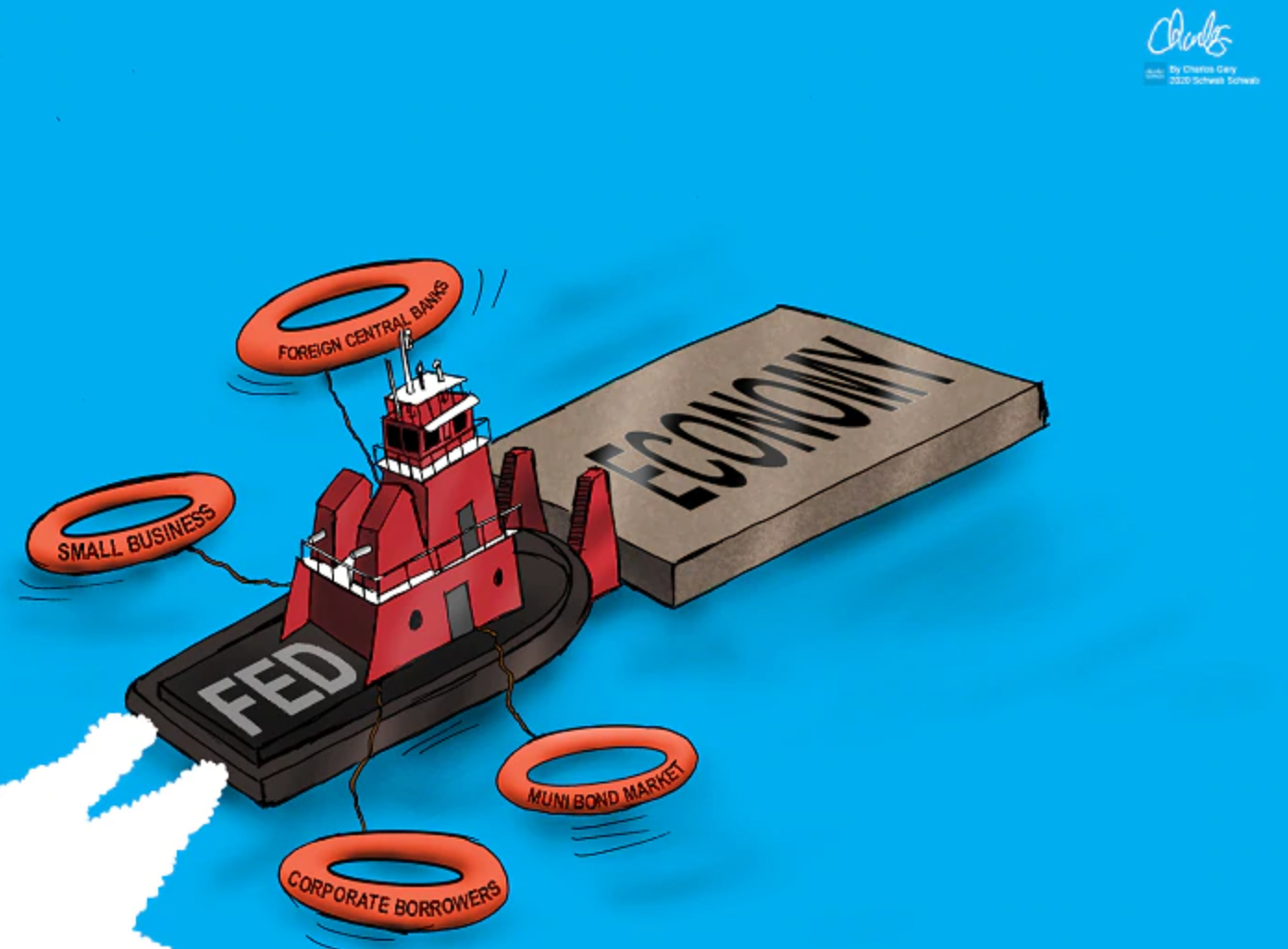

Federal Reserve officials will no doubt be among the happiest to say good-by to 2020. It was a year in which the Fed led the response to the COVID-19 crisis, pushing interest rates lower and rolling out a variety of programs to help support the economy. There was fiscal action at the beginning of the COVID-19 crisis, but for much of the year, the Fed has been the major force pushing the economy forward, throwing lifelines to corporations, foreign central banks and municipalities through its special facilities and programs.

As a result of the Fed’s steep interest rate cuts and bond buying programs, returns for fixed income investments have been strong.

As we look into 2021, we see a different outlook. With the likelihood of vaccines for the coronavirus becoming widely available by mid-year, the economy should get a boost as sectors that have been held back by the health crisis recover. There is also the possibility of more fiscal relief for the economy coming late this year or early next year. A fiscal aid package as large as $2 trillion has been discussed and would provide a boost to the economy.

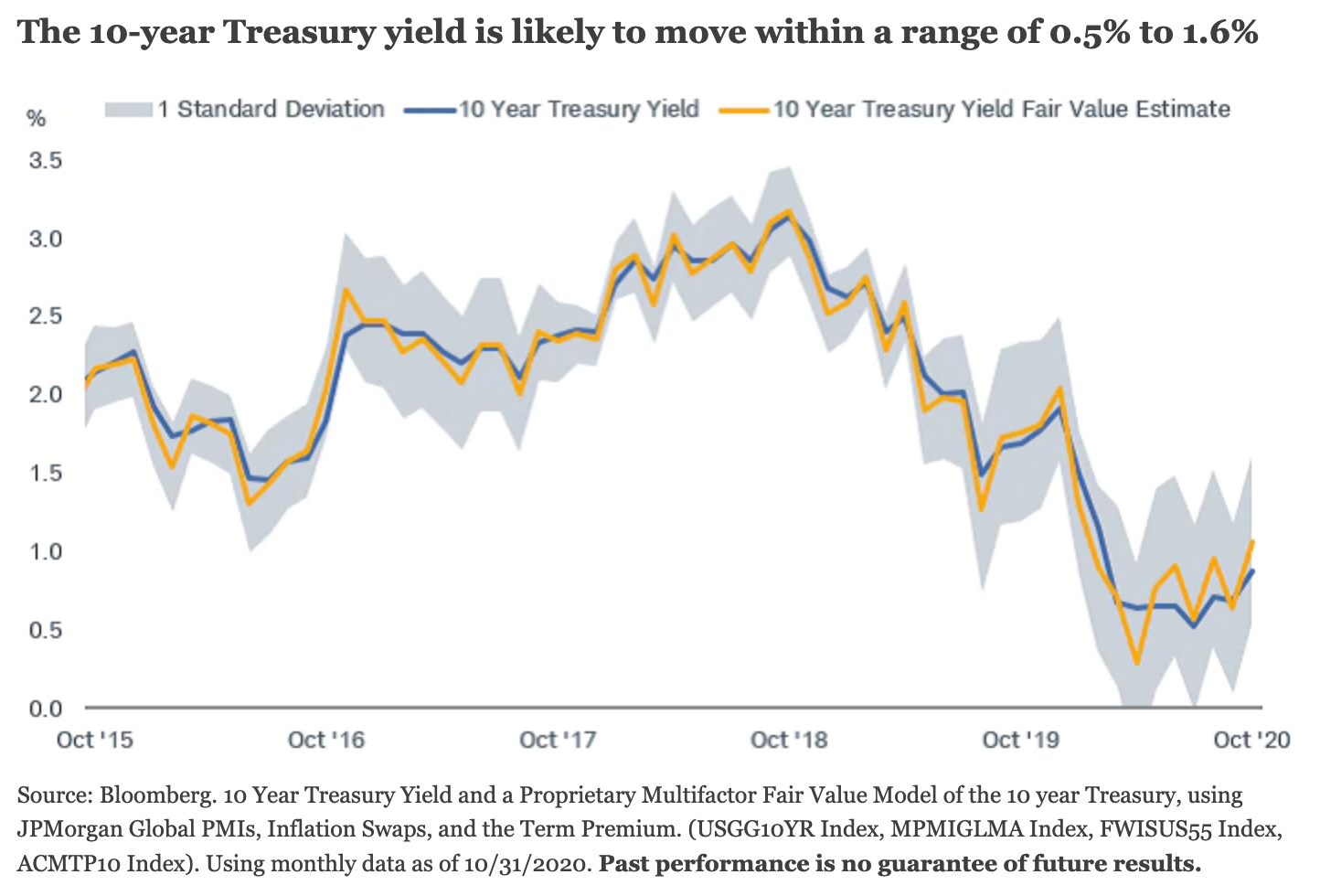

Consequently, we see the potential for 10-year Treasury bond yields to trade in a range of 1% to as high as 1.6% in 2021, reflecting the prospects for real economic growth to recover at a faster pace. Our estimates come from our fair value model, which currently shows that the 10-year yield is fairly valued at about 1%, with a potential range of about 0.5% to 1.6%. As we are expecting a more positive economic scenario, we wouldn’t be surprised to see yields move to the upper end of that range if the economy posts a solid recovery in the second half of next year. Meanwhile, short-term interest rates are likely to remain pinned near zero throughout the year as the Fed waits to “normalize” interest rates until inflation rises. Consequently, the yield curve should steepen as the difference between short and long-term yields expands.

For investors, that suggests that returns in 2021 will likely come from the coupon income earned on their holdings rather than price appreciation. In fact, long-term bonds could experience price declines if interest rates rise too much.

What will the Federal Reserve do?

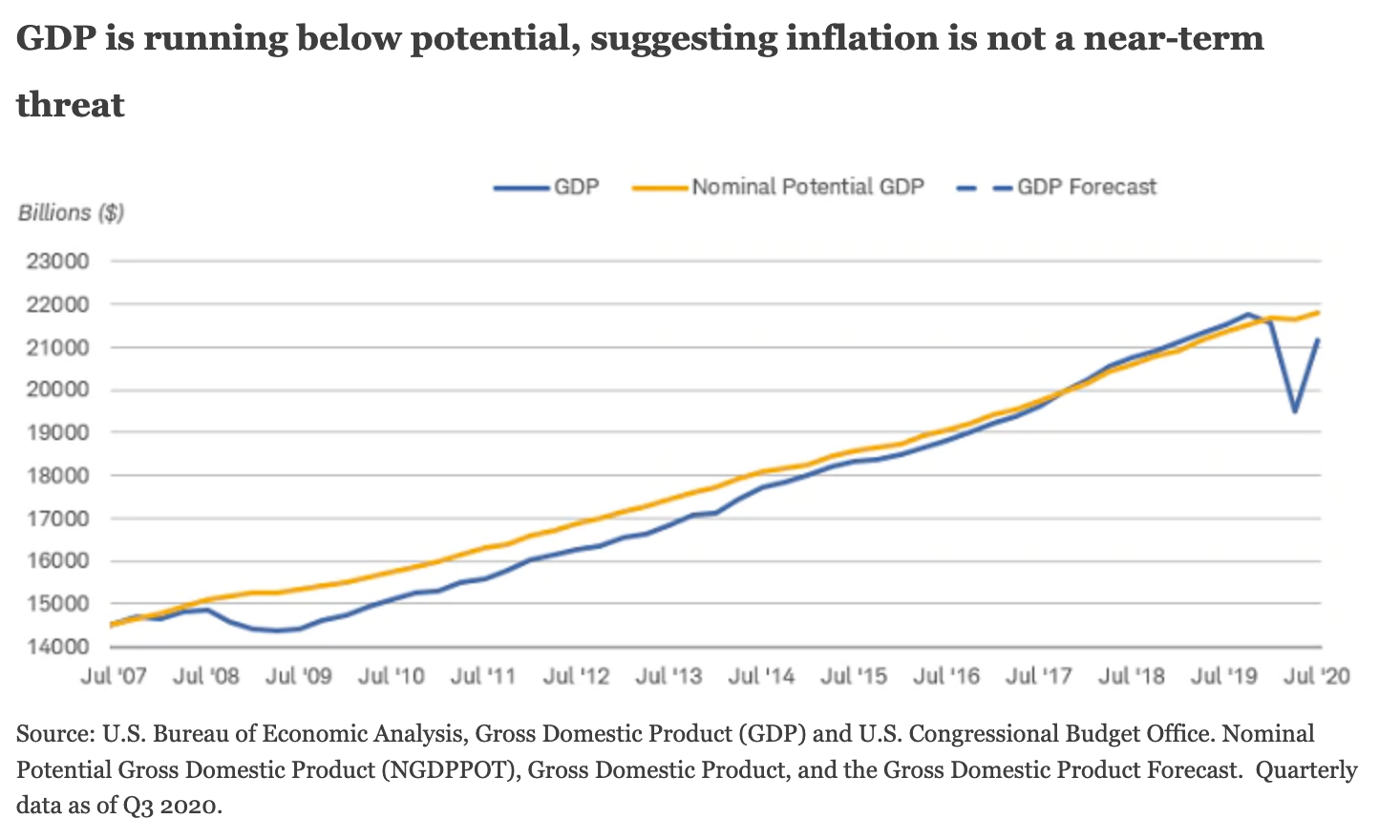

We don’t expect any major policy changes from the Fed for at least the first half of 2021. Even under an optimistic scenario for the distribution of a vaccine, the economy will take time to rebound to pre-pandemic levels. There is a lot of lost ground to make up. The economy has only recovered about two-thirds of the gross domestic product (GDP) growth that it lost in the downturn and is still growing at a rate well below its potential.

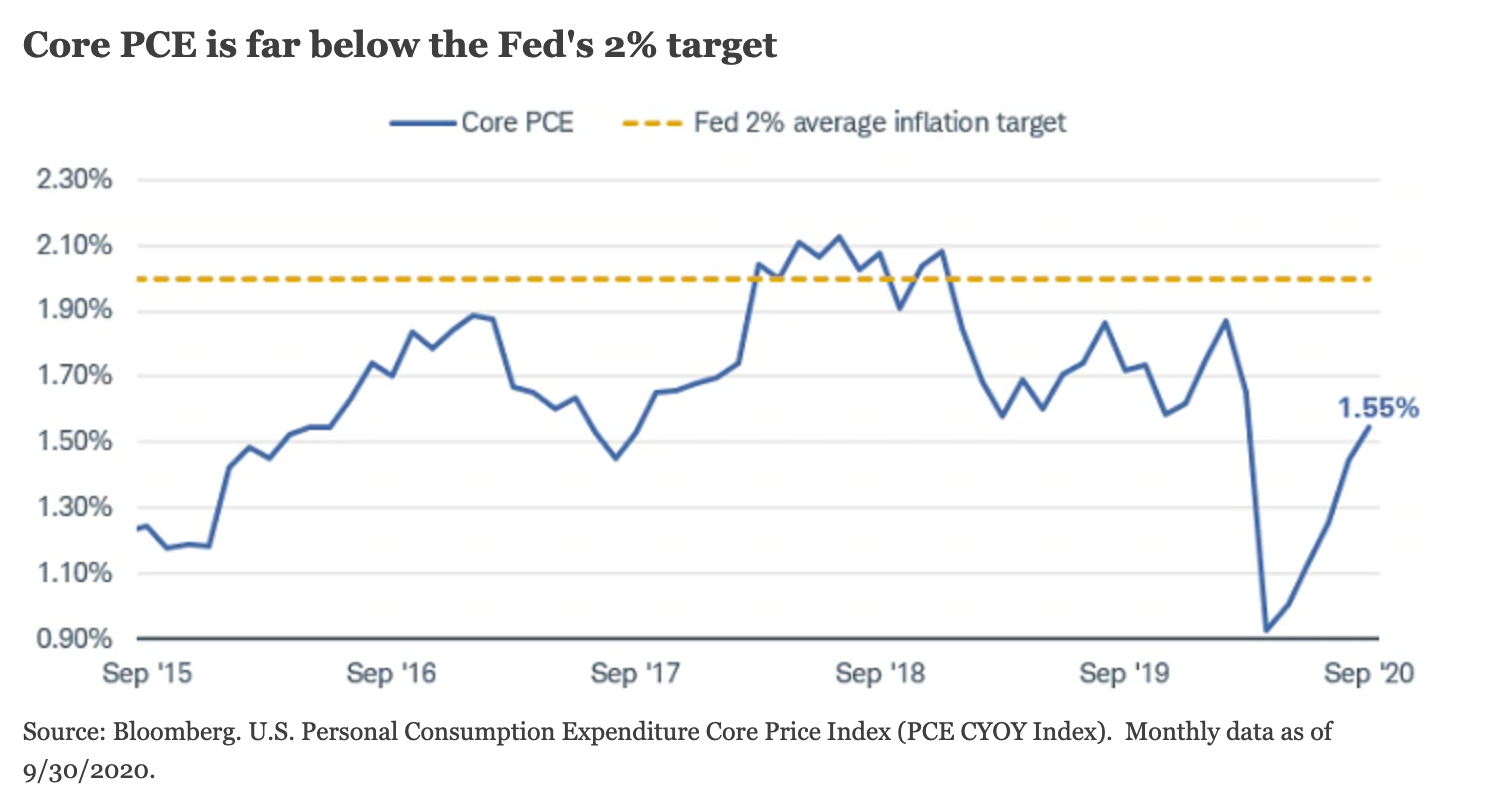

Consequently, inflation is not likely to be a risk until economic growth closes the gap by reaching its potential and exceeding it for a period of time. Moreover, under the Fed’s new policy guidelines, it will not begin to tighten policy until inflation actually goes above its 2% target for a sustained period of time and the unemployment rate falls to a level consistent with full employment. The Fed’s new mandate indicates “maximum employment is a broad-based and inclusive goal.” We doubt those conditions will be met until sometime in 2022 or later.

Inflation, using the measure that the Fed uses for its benchmark—the deflator for personal consumption expenditures excluding food and energy—has been below 2% for most of the past several years. The unemployment rate has fallen to under 8%, but it is still a long way from 3.5%, where it stood earlier this year, and there are still more than 10 million fewer jobs now than there were earlier in the year.

If the inflation outlook shifted more quickly, the Fed could alter its other policies before it changed interest rates. It could reduce the pace of its purchases of Treasuries and mortgage-backed securities and shift the maturities of the bonds it buys. It isn’t clear what will happen to the Fed’s special facilities that provided a lifeline to parts of the fixed income market early in the crisis. Most are scheduled to expire by the end of this year. Most likely, the Fed would like to extend them until the economy is stronger, but because these are coordinated with the Treasury Department, it’s possible that the change in administration could make an extension difficult.

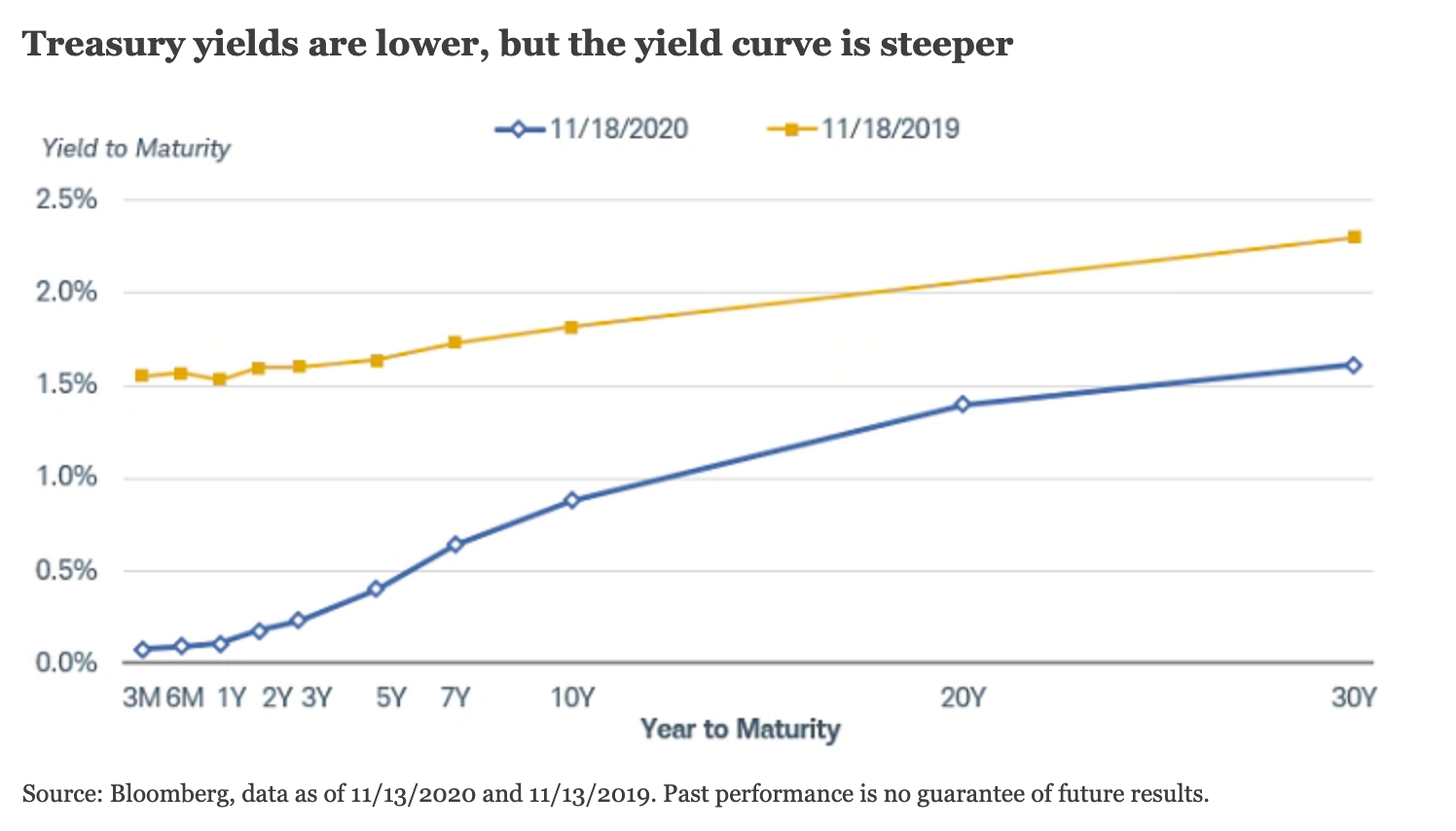

The market, however, expects the Fed to keep interest rates on hold until 2023. Treasury notes with maturities up to 2 years remain within the federal funds target range of 0% to 25% (set by the Fed) and haven’t changed much even as long-term yields have risen.

New strategies for a new year

The prospect of rising interest rates tends to make bond investors wary, as higher rates mean lower bond prices, all else being equal. However, we view higher bond yields as an opportunity. When bond yields move up, it offers the chance for investors to capture more income from interest payments without necessarily taking more risk. Structuring a portfolio to benefit from rising yields is the opportunity we see in 2021.

- Keep average duration low but look to increase it as yields move higher. Throughout most of 2020, we suggested keeping the average duration of the bonds in a portfolio low. (Duration is a measure of a bond’s sensitivity to interest rate changes. Generally speaking, the higher the duration, the more a bond will fall if interest rates rise and vice versa.) For now, we would stay with that strategy. However, if yields rise as we anticipate, we would use it as an opportunity to gradually add some longer-term bonds for more income. A bond ladder is a tool that can help do this, because it lends itself to averaging into higher yields over time.

- Look for bonds with higher coupons – cautiously. In a world with low and rising interest rates, it makes sense to hold bonds with higher coupons, as most of the return is likely to come from the interest income generated. However, we would be cautious about reaching into the lowest credit ratings in search of yield. The risk/reward in the lower tiers of high yield or municipal bonds looks unattractive to us based on current valuations.

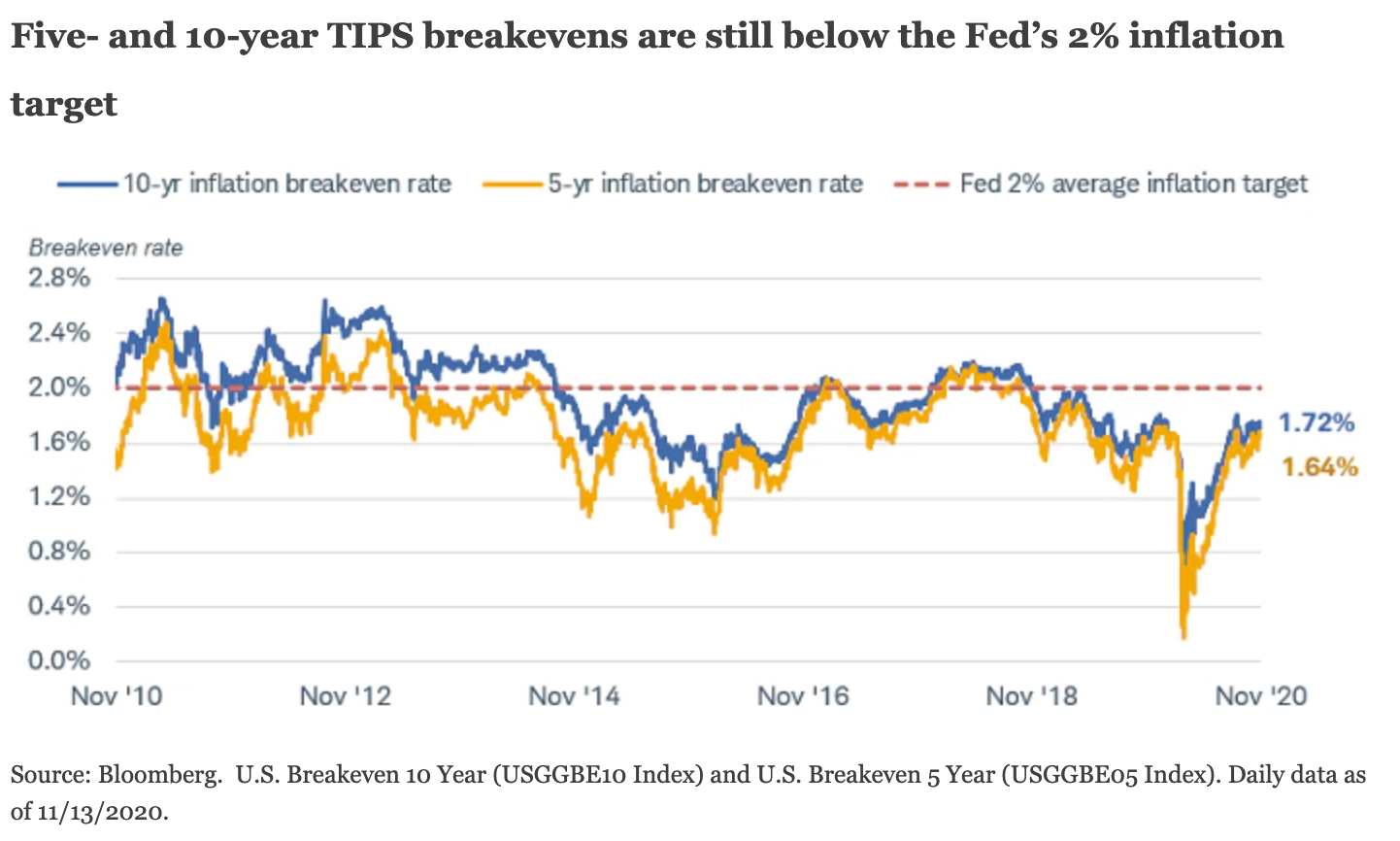

- Consider inflation-linked bonds like Treasury Inflation Protected Securities (TIPS). As the economy recovers, inflation is likely to continue edging higher. While we don’t expect a big rise, having some inflation protection can help offset a gradual rise over time. The breakeven rates (the rate that inflation would need to average for a TIPS to outperform a comparable nominal Treasury) for five and ten-year TIPS are still below the Fed’s 2% inflation target, leaving room for appreciation if inflation rises. However, TIPS yields are low or negative, so we suggest an approach of shifting some Treasury holdings to TIPS.

.

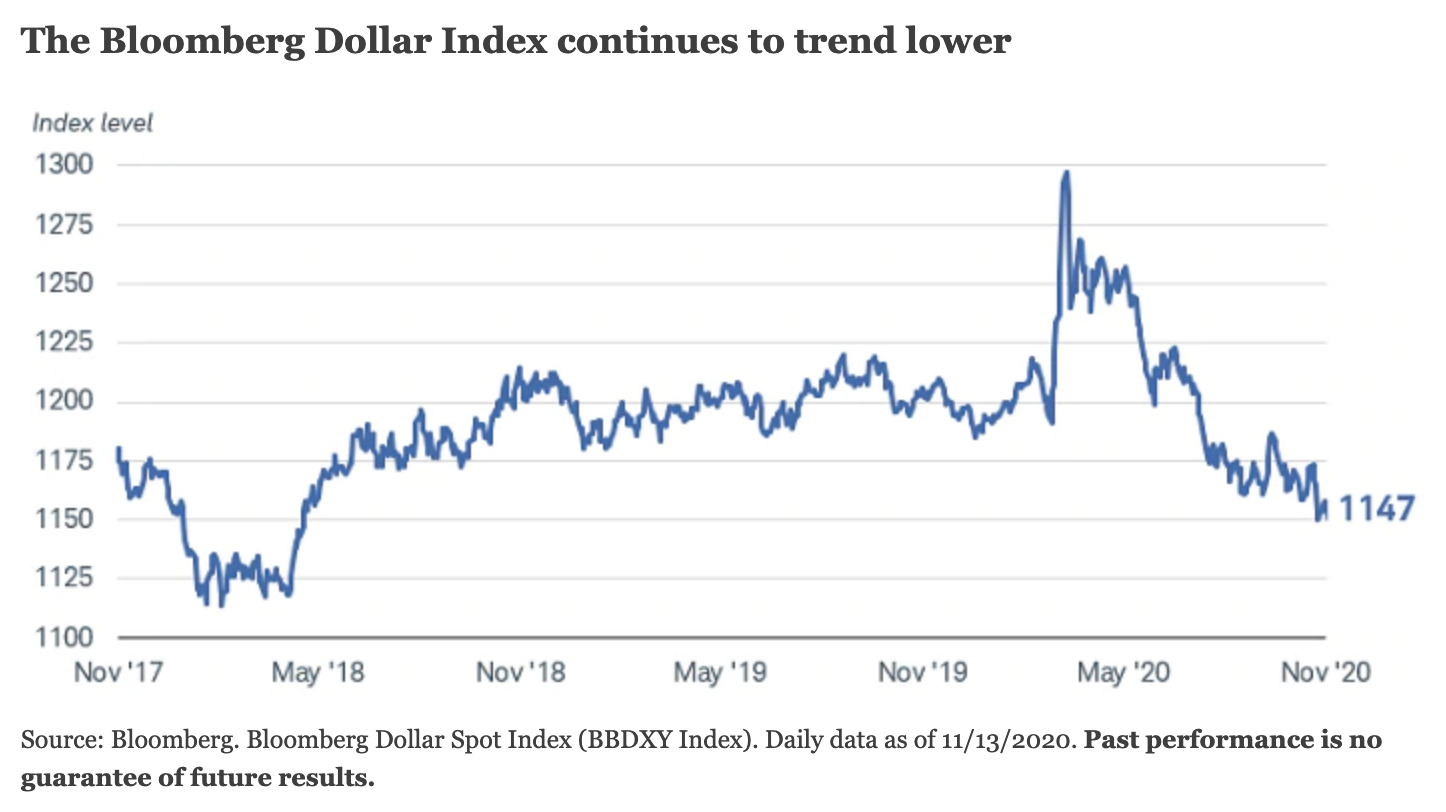

- Diversify globally. One consequence of the Fed’s aggressive policy moves earlier in the year is a weaker dollar. As the Fed lowered short-term interest rates to zero, real bond yields (adjusted for inflation) fell into negative territory, with yields below the rate of inflation. Now they are as low as those in Europe, where short-term rates are negative and there are concerns about deflation. We expect the dollar to continue trending lower due to the Fed’s very easy monetary policy and the likelihood that U.S. budget and trade deficits will continue to expand. Since the U.S. borrows more than it earns on foreign investments, financing the trade and budget deficits means attracting foreign capital. A cheaper dollar makes it easier to attract enough investment to fill the gap.

As the dollar falls, it can boost the returns of foreign bonds, especially emerging-market bonds. The combination of a weaker dollar and stronger global growth should benefit emerging-market countries, because many rely on exports for economic growth. In addition, yields for emerging- market bonds are still slightly above the long-term average.

In general, our guidance for investors looking to allocate to fixed income investments is to concentrate the bulk of the portfolio in core bonds—those with higher credit ratings and lower risk of default. The remainder of the portfolio can be allocated to more aggressive income investments for those seeking higher income with the capacity and inclination to take more risk.

What could go wrong?

There is a famous saying that “Predictions are difficult, especially about the future.” We have to acknowledge that there are risks to our outlook. The biggest one is the risk that an effective vaccine is not found or distributed as soon as currently anticipated. Given the severity of the COVID-19 crisis, this is something we are monitoring closely. Related to that is the risk that Congress does not come through with enough aid to support the economy early in the year, causing growth to falter and unemployment to rise. Both of these would likely result in lower Treasury yields, or potentially a smaller rise in yields than we are anticipating.

There is also the risk that the dollar proves more resilient than expected, supporting demand for U.S. bonds. Foreign demand for U.S. government bonds has remained firm despite rising deficits, and may increase if yields rise further relative to those in other major developed countries. That could cap the upside in yields.

On the upside, there is a chance that the pandemic could end sooner than expected, leading to a stronger-than-expected rebound in the economy and inflation. When combined with the prospect of large and rising deficits that need to be funded by increasing issuance of government bonds, yields could rise more than we currently expect.

Overall, we see 2021 as a potentially more challenging year for fixed income investors. Planning a fixed income allocation based on the path of a global pandemic isn’t easy. We believe focusing on earning income, managing risk and diversification will be valuable strategies given the wide range of potential outcomes.

Copyright © Schwab Center for FInancial Research