by Shamaila Khan, AllianceBernstein

Emerging-market debt (EMD) has rebounded sharply off March lows as investor fears of a pandemic-driven rout have subsided. But even with volatility possibly picking up over the near term—largely the result of uncertainty around US elections—we see significant opportunities ahead.

Below are four important guideposts for investors in today’s EMD markets.

1. Emerging markets (EM) are resilient. The COVID-19 experience for EM countries has been similar to that of developed markets—some countries have fared well, some have not. Even EM countries like headline-grabbing Brazil and India have thus far stabilized COVID-19 cases and bent the curve.

In general, EM governments have curtailed shutdowns to retain revenue and limited the size of fiscal stimulus to prevent erosion of credit quality. As a result, concerns about systemic defaults triggered by the pandemic haven’t been realized. Recent defaults by Argentina, Ecuador, and Lebanon were anticipated well before 2020.

We expect this kind of broad resiliency to persist. And as more information is known about potential vaccines, improved treatments and even better testing capacity, global growth should get a boost—a positive for EM assets.

2. US elections matter. From rising tensions between the US and China to infrastructure and energy policies, the outcome of this US election may matter more than usual for risk assets. EMD is no exception.

For example, we believe EM countries would benefit from conventional diplomacy and more predictable trade negotiations with China, which are more probable under a Biden administration. Lower headline risk would make a more conducive environment for EMD assets. Fiscal stimulus and increased spending on US infrastructure—highly likely if Democrats win the White House and sweep Congress—would also be a tailwind to EM countries and companies, which supply the needed raw commodities.

A new administration might also have different views about the role of the International Monetary Fund in the global economy. This might result in either additional or reallocated Special Drawing Rights, which could increase funding sources for EM countries.

Lastly, US energy policy is particularly critical for EM economies, whether oil producing or oil consuming. A Biden administration’s focus on green energy would impact the shale sector, which could raise energy prices over the near term. Over the medium term, however, our view on energy prices is more nuanced. Improved relations between the US and Iran could allow for Iranian oil sales, lowering energy prices. So would greater support for the sale of electric vehicles.

On the other hand, should Trump prevail, we would likely see a continuation of current policies, meaning that oil prices would rise only when global economies recover and/or a vaccine for the novel coronavirus proves successful.

3. A weaker US dollar could provide lift. The US dollar is overvalued. We believe that the dollar could weaken due to the current account deficit, a (growing) budget deficit and low rates.

Generally, when the dollar is weak, capital flows into EM assets in search of higher growth and yields. A weaker dollar would also benefit EM countries by reducing the cost of debt service on existing US dollar–denominated EM debt. And it could make local-currency debt more attractive in the long run.

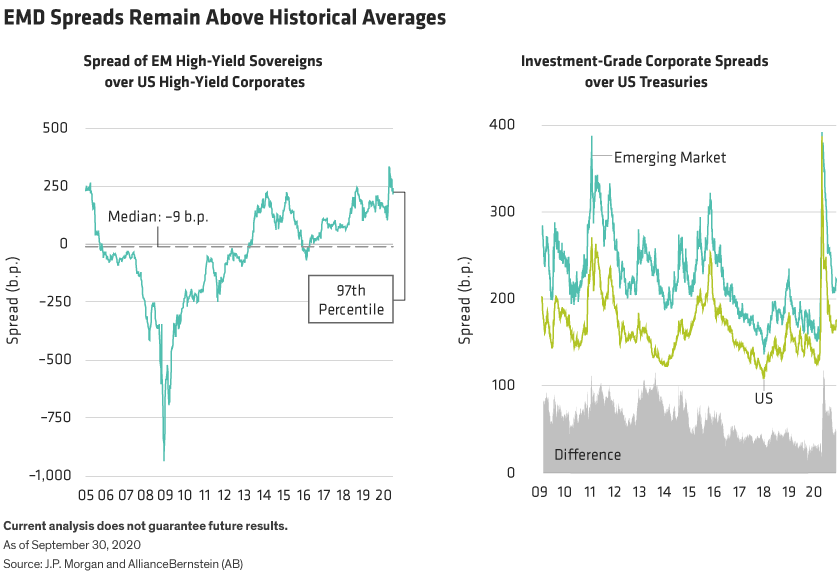

4. EMD offers compelling yields. EMD offers exceptionally attractive yields in a low-yield environment. We see the most compelling opportunities in EM high-yield debt, particularly in sovereign bonds. EM high yield is currently trading at historically wide spreads compared to US high yield (Display, left).

But high-yield sovereigns aren’t the only compelling opportunity in EMD today. Investment-grade EM corporate spreads also remain wider than US investment-grade corporate spreads (Display, right), despite their strong and improving trend in credit fundamentals. This suggests that the tailwinds behind EMD aren’t yet fully priced in.

Of course, EM countries are not homogenous, and selectivity is important. For example, Turkey is at risk of suffering a balance-of-payments crisis, and Sri Lanka has issues with debt sustainability. That’s why we believe that bottom-up analysis and active investing remain imperative for EMD investors.

In our view, EMD investors who heed these guideposts can successfully navigate any bumps in the road while enjoying attractive yields, compelling opportunities and the benefits of today’s tailwinds.

Shamaila Khan is Director of Emerging-Market Debt at AB.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

This post was first published at the official blog of AllianceBernstein..