by Lei Qiu, Portfolio Manager—International Technology; Senior Research Analyst—Thematic & Sustainable Equities, AllianceBernstein

Technology stocks seem unstoppable. Giants like Apple and Microsoft, as well as technology-driven consumer firms such as Amazon and Alibaba Group, continue to do well through the COVID-19 pandemic. Meanwhile, an emerging group of resilient, innovative leaders, ranging from cloud-based service providers and fintech to ecommerce enablers, also show solid growth, fueled by rapid business and consumer changes brought by the pandemic.

The tech-heavy Nasdaq Composite Index has surged by 20.5% this year through July 31, while the MSCI World Technology Index is up 20.8% for the period. When compared to the more muted rebounds of the S&P 500 and MSCI World indexes, it’s clear that investors are giving tech stocks their day in the sun.

Strong gains have pushed up valuations of technology stocks. Global technology stocks trade at a price/forward earnings valuation of 26.5x, a 30% premium to the MSCI World Index. Is the gap warranted or based more on irrational animal spirits? In these unprecedented times, we think some high prices are justified, especially for companies with sustainable growth drivers. Investors just need to get past a few myths to find the opportunities.

Myth #1: All Tech is Overpriced

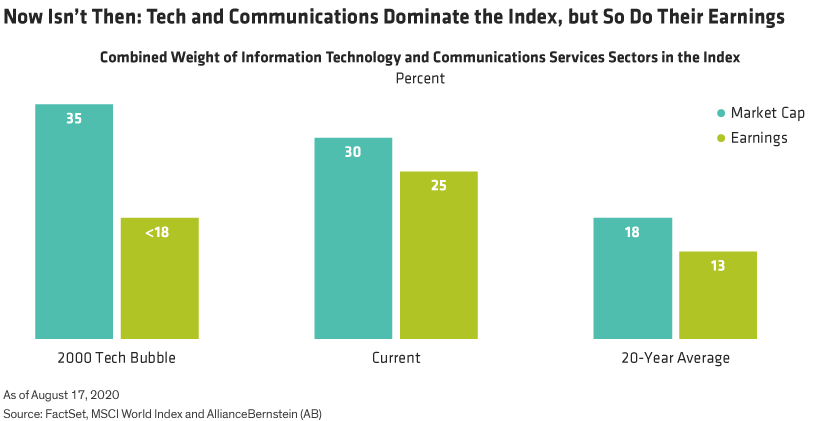

Technology is not a homogenous sector, and not all tech companies are overpriced. In fact, the sector’s valuation premium is relatively low versus its historical high (Display).

At the market’s peak in March of 2000, the MSCI World’s technology and communication services sectors combined accounted for 35% of market cap and less than 18% of the earnings. But today, the two sectors represent 30% of market cap yet almost 25% of all earnings (Display). The reason? In an ever more web-connected world, tech companies increasingly enjoy the positive benefit of the network effect, allowing them to take advantage of scale and generate higher incremental margins.

Myth #2: High Valuation = High Risk

Is it riskier to pay more for a stock? Not necessarily, especially when the reasons and perceptions behind high valuations can be so different. Tech companies with secular growth drivers, for instance, are perceived to have greater predictable earnings growth versus companies with cyclical drivers, which are more dependent on macroeconomic forces hurt by the pandemic, and therefore considered much riskier.

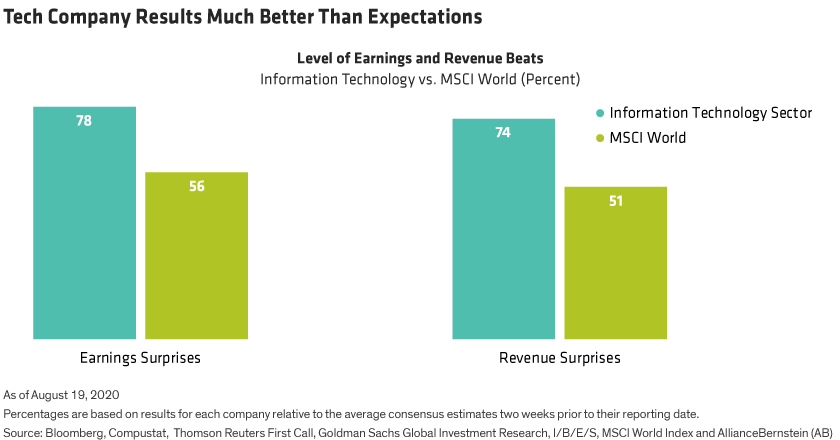

In the market’s current earnings season, information technology companies are among very few reporting year-over-year revenue growth and earnings growth. Tech companies also fared much better than expectations. Some 74% of information technology companies in the MSCI World reported higher revenue expectations and 78% reported upside surprises to earnings, compared to just 51% and 56%, respectively, for the market overall (Display).

In our view, higher valuations reflect the low risk tolerance of the broad investor base. Today, technology companies trade at similar valuations to consumer staples, while offering better growth characteristics. For instance, shares of brick-and-mortar retailers and technology companies that provide on-site IT services and equipment may look cheap but could face further declines if the pandemic persists and headwinds intensify.

The low interest-rate environment also fuels tech’s growth prospects. High-growth companies tend to have greater income streams coming from future revenue and earnings. So, when rates remain low, income streams benefit from lower discount rates, helping to boost stock prices.

Myth #3: More About Valuation, Less About Fundamentals

Is valuation even the right debate, and is there too much emphasis on price and not enough on earnings growth potential? We think so.

Remember the first-generation iPhone and Apple in 2007? Apple shares traded at jaw-dropping highs of around $18, based on projections to sell 3 million units worldwide in the first year. Compare this to the 200 million it sells annually today. It’s a familiar growth story, along with Amazon, which was always considered expensive. But even at a $280 billion revenue run rate as of year-end 2019, the company has consistently beat analyst revenue expectations while turning the corner in profitability.

Innovative tech companies may look expensive if viewed using only the consensus estimate at a static point in time. But true tech leaders have vision and tenacity. They constantly improve and reinvent themselves to maintain a competitive edge with new products and services for shifting and growing market needs. Sometimes success requires a willingness to self-disrupt their business models today to ensure their future—perhaps one of the hardest, and most controversial things to do. Think Netflix, when it first surprised the market by dramatically shifting from what was then a reasonably successful DVD-by-mail rental service to introduce an untested streaming model, which today boasts 193 million subscribers. Amazon is a classic example here too. What started off as a traditional online bookseller has expanded into a technology powerhouse that includes retail, advertising, streaming media, logistics and cloud-based infrastructure services. And during this journey, current estimates underestimated the company’s growth potential and sustainability by misreading risk queues or underappreciating earnings.

A successful innovative company is more than just a good new idea. Lasting innovators should offer sustainable revenue and profit growth potential. Currently, ample liquidity is indeed chasing very few growth opportunities, many of which are among smaller, lesser-known companies. Not all are the next Amazon, but some may have the right characteristics to become the next generation’s leaders—products and services with transformational impact and the relentless, innovative DNA to constantly reinvent themselves along their growth paths. While some may look expensive based on near-term estimates, ultimately the most important exercise for investors in tech innovation is to identify the next disruptive leaders that can deliver sustainable and underestimated growth beyond the short-term boom.

Lei Qiu is a Portfolio Manager on the International Technology Portfolio and a Senior Research Analyst for Thematic & Sustainable Equities at AllianceBernstein

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time. AllianceBernstein Limited is authorised and regulated by the Financial Conduct Authority in the United Kingdom.

MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein.

This post was first published at the official blog of AllianceBernstein..