by Ryan Detrick, CMT, Chief Market Strategist, LPL Financial

This earnings season may be one to forget. We will see one of the biggest year-over-year quarterly declines in S&P 500 Index profits ever, and we will hear a lot about uncertainty facing corporate America as COVID-19 continues to impact many companies in the United States and globally. But it may not all be negative.

ESTIMATES MAY BE TOO LOW

The unprecedented nature of the COVID-19 lockdowns and widespread withdrawal of corporate guidance has set up an unpredictable earnings season. The magnitude of the decline we are likely to see may make this an earnings season to forget.

As tough as it is to find a bright side in an estimated 40% collapse in S&P 500 Index earnings per share (EPS), there are several reasons to think the season may be better than analysts’ estimates have suggested. First, second quarter guidance has been better than average—55% of the guidance that has been provided has been negative, well below the five-year average of 69%, according to FactSet.

Second, recent economic data has mostly exceeded expectations, particularly for jobs and retail sales. The Citigroup Economic Surprise Index—a measure of the frequency that economic data is exceeding expectations—stands at an all-time record high for the United States. Bloomberg’s version of the same measure is very close to a record high.

Finally, earnings estimates for the second half of 2020 have been impressively stable in June and early July, which we believe increases the chances of more and bigger upside surprises. Consensus estimates for 2020 (FactSet) as of July 17 stood at $126.90, only marginally below the $127.66 estimate on June 1. We interpret this as a positive signal, while we also acknowledge the uncertainty—given that more than one-third of the S&P 500 companies withdrew guidance during the pandemic.

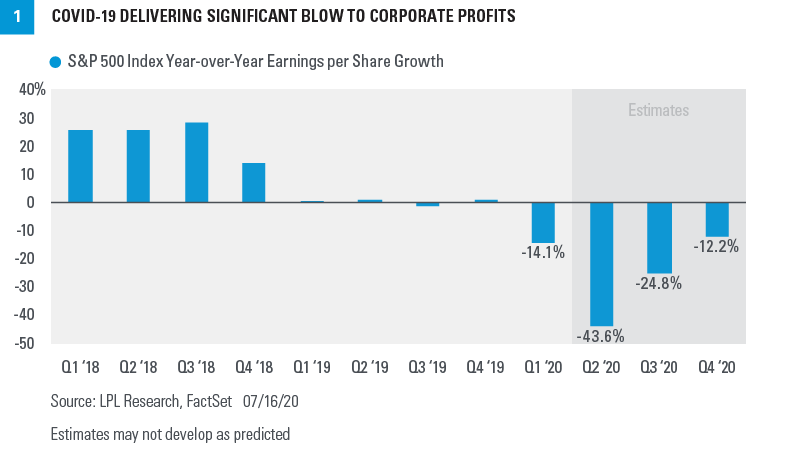

Bottom line, we think second quarter earnings season may produce a larger upside surprise to quarter-end estimates than the historical average of 3–4%. FactSet’s consensus S&P 500 EPS estimates were calling for a 44% year-over-year decline during in the second quarter, as of June 30, 2020 [FIGURE 1].

KEY THEMES TO WATCH

As we wade through this unpredictable earnings season, there are a few key themes to watch:

- Caution over optimism. Although guidance has been less negative than normal for the second quarter and the economic rebound has exceeded expectations, the outlooks for the economy and corporate America remain very uncertain. Many states, particularly in the West and South, are struggling to contain the latest outbreak of COVID-19, while several other countries, notably Brazil and India, are still seeing steady increases in cases. Improving treatments and progress toward a vaccine are encouraging, but we expect companies to err on the side of being conservative.

- Finding a floor. Economic uncertainty potentially may cause many companies to withhold guidance again, as they did after first quarter results. This may leave analysts guessing and lead to continued wide dispersion of company estimates. Whatever guidance we do get may give us a better sense of where the floor in earnings might be in the event that additional virus containment measures disrupt businesses in the coming months.

- Widening gap between winners and losers. Some companies have been largely unaffected by the COVID-19 pandemic, while others have been hard hit. For example, technology and healthcare sectors may see only modest single-digit percentage declines, based on consensus estimates. The consumer discretionary and energy sectors, however, are expected to report losses—all profits are expected to be wiped out by the pandemic. The separation between the winners and losers continues to widen in this environment.

UPDATED EARNINGS FORECAST

As we discussed in our Midyear Outlook 2020 publication, we expect the drop in earnings this year to be roughly in line with the historical average during recessions in the 25% range, or $120 to $125 per share in S&P 500 EPS. We believe this forecast reflects the severity of the decline in economic activity in March and early April, the initial snapback as the economy reopened, and growth headwinds that will constrain the recovery later this year. The severity of the recession and challenges for businesses incorporating social distancing introduce downside risk to this forecast.

Breakthroughs on treatments may make a return to pre-pandemic levels of corporate profits possible in 2021. However, given the amount of economic damage that has been done already, we think that may be unlikely.

STOCK MARKET OUTLOOK

Given earnings are depressed, we use a normalized EPS figure of $165 to set our stock market forecast. We believe that level of earnings power will be achievable as soon as the virus is fully contained. Our year-end target range for the S&P 500 fair value of 3,250–3,300 is based on that earnings forecast and a price-to-earnings (PE) ratio slightly below 20.

Even though that annual earnings run rate may not be achievable until late 2021 through early 2022, we are comfortable using a longer-term earnings target to value stocks at this point in time, given interest rates are so low and because we assign a high probability of a COVID-19 vaccine becoming available within that time frame. Although we believe stocks may be pricing in a bit too much economic optimism in the short term, for long-term investors, we continue to anticipate more potential gains for stocks than bonds over the next 12 to 24 months.

*****

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

Investing in foreign and emerging markets securities involves special additional risks. These risks include, but are not limited to, currency risk, geopolitical risk, and risk associated with varying accounting standards. Investing in emerging markets may accentuate these risks.

US Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio.

Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability. Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio.

All index data from FactSet.

Please read the full Midyear Outlook 2020: The Trail to Recovery publication for additional description and disclosure.