by Stephen Duench, AGF Management Ltd.

The COVID-19 pandemic is creating a familiar dynamic for dividend investors who have navigated economic downturns in the past, with record-high yields on one hand and payout suspensions and cuts on the other. And just like previous crises, the fallout from the virus is a valuable reminder that dividend-paying stocks are not created equally and must be evaluated on their own merits.

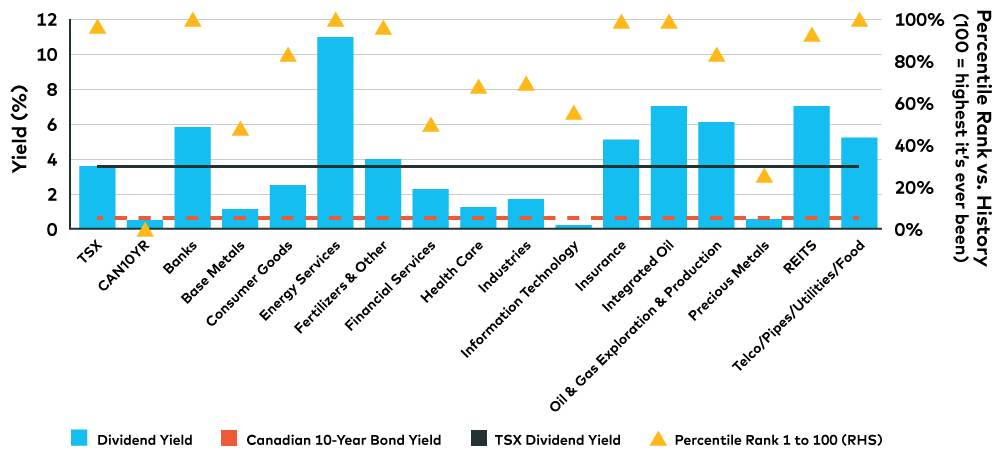

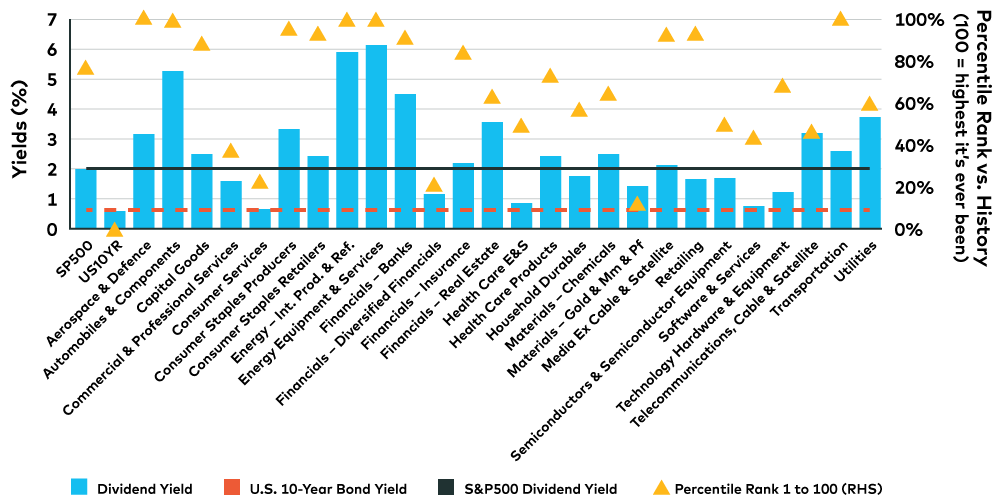

To that end, there’s no question that yields across the broad spectrum of dividend payers has become more attractive relative to 10-year government bond yields in recent weeks. In Canada and the U.S., this is true across most sectors and the average spread between the two yields recently reached all-time highs, based on our data since the Second World War. At the same time, many industries are now boasting average dividend yields near or at their historical highs on an absolute basis.

Canadian Dividend Yields: Today vs. History

Source: AGFiQ as of May 15, 2020

But higher yields are only part of the equation that makes up the current landscape for dividends. Also at play is a growing list of dividend suspensions and/or cuts as companies batten down their hatches in hopes of minimizing the damage of the economic slowdown. In many cases, these actions are being taken to shore up already diminishing balance sheet strength or to pre-empt such deterioration from happening in the first place. Meanwhile, some companies are suspending or reducing their dividends on principle after having to furlough employees unable to work due to government shutdowns and social distancing measures.

U.S. Dividend Yields: Today vs. History

Source: AGFiQ as of May 15, 2020

Either way, this growing list highlights the value of analyzing dividend payers based not only on the size of their current yield, but also its sustainability over time. And while it’s difficult to predict whether a company chooses to suspend or cut its dividend under extraordinary circumstances, it’s possible to forecast which companies may be forced to make those same decisions. For example, those with low debt-to-equity and high cash-to-asset ratios are more likely to support their dividends than those without. The same goes for payers that have historically high return-on-equity (ROE) and low payout ratios.

Keeping close tabs on these factors—along with others such as high free cash flow yield and high free cash flow margin—should be nothing new to seasoned dividend investors, but doing so rigorously has not been this critical since the Great Financial Crisis more than a decade ago. After all, the opportunity set for dividends may never be more attractive than it is now, but it also may never be more precarious.

Stephen Duench is a Vice President and Portfolio Manager at AGF Investments Inc. He is a regular contributor to AGF Perspectives.

To learn more about our quantitative capabilities, please click here.

*****

The commentaries contained herein are provided as a general source of information based on information available as of May 25, 2020 and should not be considered as investment advice or an offer or solicitations to buy and/or sell securities. Every effort has been made to ensure accuracy in these commentaries at the time of publication, however, accuracy cannot be guaranteed. Investors are expected to obtain professional investment advice.

The views expressed in this blog are those of the author and do not necessarily represent the opinions of AGF, its subsidiaries or any of its affiliated companies, funds or investment strategies.

AGF Investments is a group of wholly owned subsidiaries of AGF and includes AGF Investments Inc., AGF Investments America Inc., AGF Investments LLC, AGF Asset Management (Asia) Limited and AGF International Advisors Company Limited. The term AGF Investments m ay refer to one or more of the direct or indirect subsidiaries of AGF or to all of them jointly. This term is used for convenience and does not precisely describe any of the separate companies, each of which manages its own affairs.

™ The ‘AGF’ logo is a trademark of AGF Management Limited and used under licence.

About AGF Management Limited

Founded in 1957, AGF Management Limited (AGF) is an independent and globally diverse asset management firm. AGF brings a disciplined approach to delivering excellence in investment management through its fundamental, quantitative, alternative and high-net-worth businesses focused on providing an exceptional client experience. AGF’s suite of investment solutions extends globally to a wide range of clients, from financial advisors and individual investors to institutional investors including pension plans, corporate plans, sovereign wealth funds and endowments and foundations.

For further information, please visit AGF.com.

© 2020 AGF Management Limited. All rights reserved.

This post was first published at the AGF Perspectives Blog.