by The editor's desk, AGF Management Ltd.

Members of the AGFiQ quantitative investing team provide their perspective on the COVID-19 pandemic in the latest crisis roundup from AGF’s investment management team.

Stephen Duench, Vice-President and Portfolio Manager, AGF Investments Inc.

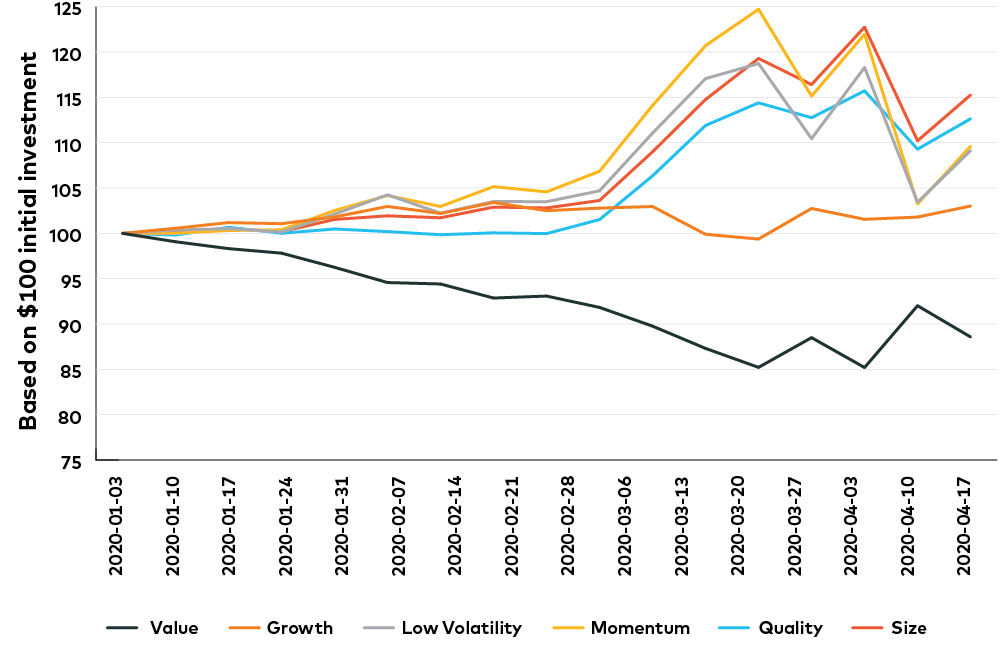

There’s been a lot of talk about what the best performing factor is so far this year. Many cite growth as the one that has led the way through the first quarter and that it is now trading at historically extreme levels. But this is misleading and based on growth’s widely discussed outperformance relative to value, which has continued to lag in 2020. While our analysis shows that growth has done well, its performance is neither the strongest nor the most extreme when considering the handful of “pure” factors that we consider in our investment decisions. In fact, of all the factors that have outperformed the broader market to this point in 2020, size and quality are the top two performers, followed by momentum, low volatility, and then growth, which is trailed only by value, the lone factor to underperform the market this year. Perhaps the more interesting facet in this analysis then is how poorly value continues to stack up against other factors. Even when stripped of sector and size bias, it continues to be left behind. Will this persist? That’s largely unclear, but as we continue to monitor factor behavior, factor internals and factor valuations, we are slowly warming up to value on an unbiased sector basis.

Factor Performance: Leaving Value Behind

Source: AGFiQ with data from FactSet as of April 17, 2020. Cumulative performance of Sector Neutral Value, Growth, Low Volatility, Momentum, Quality, and Size factors for stocks listed on the MSCI USA Index. Factor returns are calculated as the quintile performance spread between the best and worst group of stocks ordered by the relative factor. Trailing Price to Earnings, Trailing Earnings Growth, 300 Day Volatility, 12 Month Price Momentum, ROIC, and Market Cap are used as proxies for the factors respectively.

Abhishek Ashok, Analyst, AGF Investments Inc.

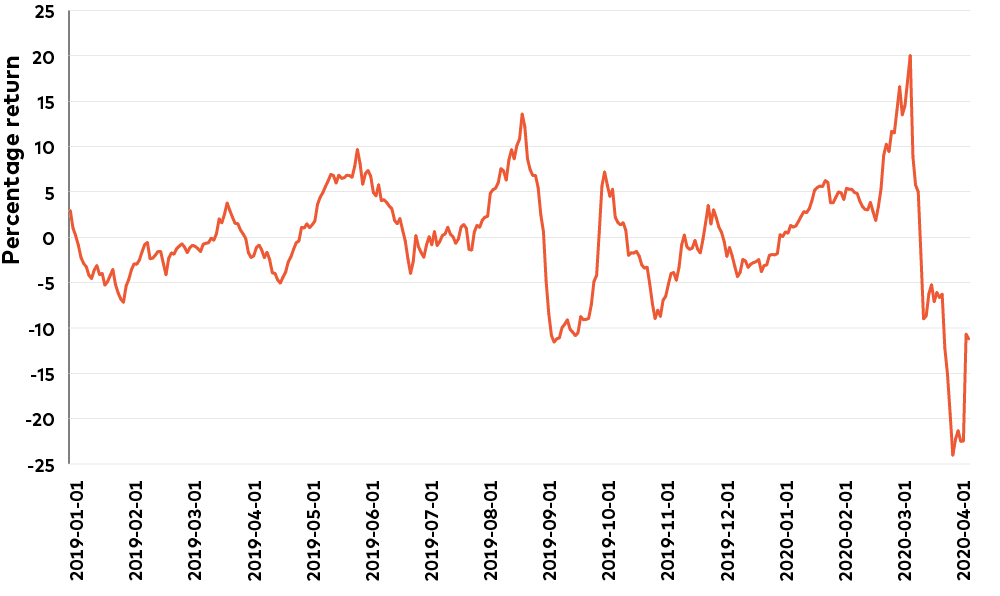

Momentum as a factor has never been stronger, nor more volatile with intra-sector winners outperforming their respective losers by over 20% through the majority of the first quarter and into the market low in March. The acceleration of momentum easily surpassed the previous high spread between winners and losers that occurred this past summer. However, like then, the current high spread has unwound viciously in more recent weeks, creating unprecedented factor volatility. In fact, intra-sector winners from earlier in the year underperformed prior losers by close to 25% through the end of March. Since then, the volatility has continued, with winners underperforming the laggards by close to 13% one week only to outperform by 10% in the following week. These extreme swings in performance should normalize as the path towards a global recovery becomes clearer, but our focus lies in figuring out whether the volatility in momentum is signalling a small regime shift like it did this past summer.

Momentum: Strong and Volatile

Source: AGFiQ with data from FactSet as of April 17, 2020. Quintile spread of the one-month performance between stocks with the best and worst 12 Month Price Momentum in the MSCI USA Index.

Grant Wang, Senior Vice-President, Co-CIO AGFiQ Quantitative Investing, Head of Research, AGF Investments Inc.

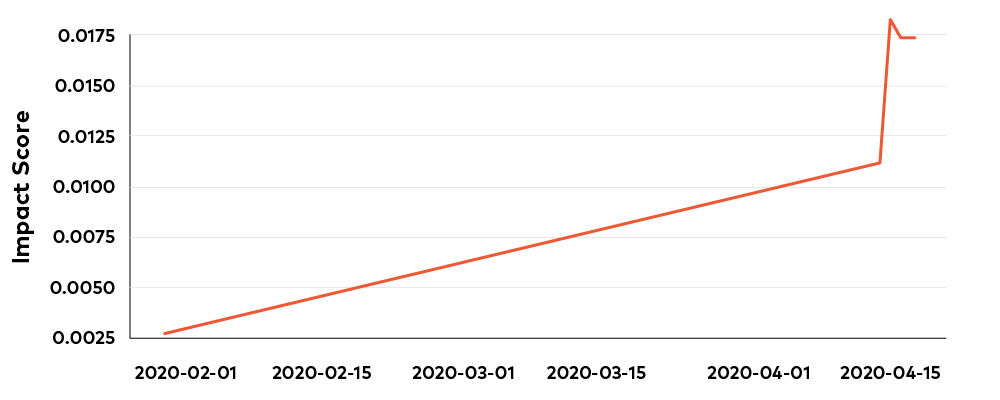

We’ve been quantifying company exposure to the coronavirus since February using natural language processing techniques that scour world-wide earnings call transcripts for words and sentences that highlight sentiment towards the pandemic. While healthcare providers have been treated separately due to their special role in the current environment, companies in other sectors that have commented on the virus in their earnings presentations have tended to suffer from severe losses in the aftermath. And companies who do not mention the virus have performed better. For example, we observed an immediate spike in the impact score of U.S. banks once they started reporting second quarter earnings earlier this month and from April 14th to April 17th, the KBW Nasdaq Bank Index was down 3% versus a 4% gain in the S&P 500 index. That makes banking one of the most negatively impacted U.S. sectors so far, while utilities is the least impacted sector.

U.S. Banks: Hanging on Every Word

Source: AGF Investments Inc. The impact score is based on the analysis of earnings call transcripts of U.S. banks listed on the MSCI USA Index and represents the ratio of pandemic word counts to total word counts adjusted by negative sentiment scores.

The commentaries contained herein are provided as a general source of information based on information available as of April 22, 2020 and should not be considered as investment advice or an offer or solicitations to buy and/or sell securities. Every effort has been made to ensure accuracy in these commentaries at the time of publication, however, accuracy cannot be guaranteed. Investors are expected to obtain professional investment advice.

The views expressed in this blog are those of the author and do not necessarily represent the opinions of AGF, its subsidiaries or any of its affiliated companies, funds or investment strategies.

AGF Investments is a group of wholly owned subsidiaries of AGF and includes AGF Investments Inc., AGF Investments America Inc., AGF Investments LLC, AGF Asset Management (Asia) Limited and AGF International Advisors Company Limited. The term AGF Investments m ay refer to one or m ore of the direct or indirect subsidiaries of AGF or to all of them jointly. This term is used for convenience and does not precisely describe any of the separate companies, each of which manages its own affairs.

™ The ‘AGF’ logo is a trademark of AGF Management Limited and used under licence.

About AGF Management Limited

Founded in 1957, AGF Management Limited (AGF) is an independent and globally diverse asset management firm. AGF brings a disciplined approach to delivering excellence in investment management through its fundamental, quantitative, alternative and high-net-worth businesses focused on providing an exceptional client experience. AGF’s suite of investment solutions extends globally to a wide range of clients, from financial advisors and individual investors to institutional investors including pension plans, corporate plans, sovereign wealth funds and endowments and foundations.

For further information, please visit AGF.com.

© 2020 AGF Management Limited. All rights reserved.

This post was first published at the AGF Perspectives Blog.