by Lance Roberts, RIA Pro

Last week we discussed the breakout to all-time highs as the belief the market is immune to risks, due to the Federal Reserve, has become pervasive. As I quoted:

“Yet as a major economic problem looms on the horizon, the cognitive disconnect between current asset prices and reality feels like the market equivalent of ‘peace for our time.’

For those investors who perceive the disconnect between risk assets which are priced for a rosy outcome, and the reality of the looming risks to growth and earnings, any attempt to reduce risk leads to underperformance. It is a mind-numbing exercise for investors who see the cognitive dissonance. The frantic race to accumulate securities has cast price discovery to the side.

I have never in my career seen anything as crazy as what’s going on right now, this will eventually end badly.“ – Scott Minerd, CIO of Guggenheim Investments

The current environment remind s me of when I was growing up. My father, probably much like yours, had pearls of wisdom that he would drop along the way. It wasn’t until much later in life that I learned that such knowledge did not come from books, but through experience. One of my favorite pieces of “wisdom” was:

“Exactly how many warnings do need before you figure out that something bad is about to happen?”

Of course, back then, he was mostly referring to warnings he issued for me “not” to do something I was determined to do. Generally, it involved something like trying to replicate Evil Knievel’s jump at Caesar’s Palace using a homemade ramp and a collection of the neighbor’s trash cans.

However, I always based my arguments on sound logic and data analysis:

“But Dad, everyone else is doing it.”

After I had broken my wrist, I understood what he meant.

Likewise, investors are currently rushing to get back into the market with a near reckless disregard for the consequences.

A near-record stretch of calm has ignited options traders’ desire to buy speculative call options.

Over the past 6 weeks, they’ve bought (to open) 70 million more contracts than they’ve sold (to close).

We’ve never seen this level of speculation before. Not even close. pic.twitter.com/VtRCRXRTbS

— SentimenTrader (@sentimentrader) February 15, 2020

Simply because “everyone else is doing it.”

So, before you go “hit the ramp”, there are some warning signs to consider.

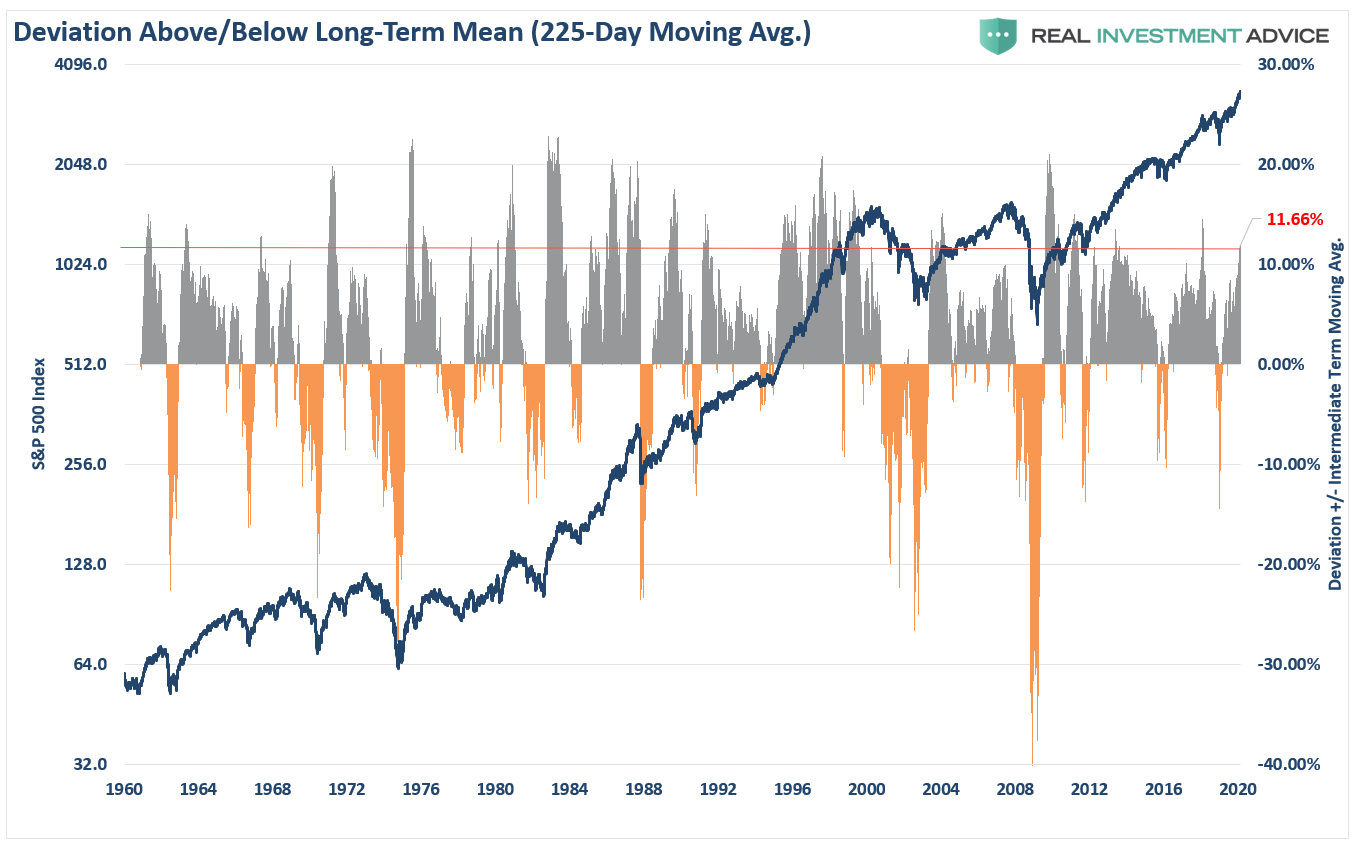

Warning 1: Deviations From The Mean

There is a funny story about a “defensive driving” class where the instructor asks the class how many thought they were “above average drivers.” About 80% of the class raised their hands. The funny thing is that all of them were in the class because of traffic violations or accidents. But more to the point, 80% of drivers cannot be above average. It is mathematically impossible.

Likewise, in investing, prices must be both above, and below, the “average price” over a set period for an average to exist. To many degrees, “price” is bound by the laws of physics, the farther from the “average price” the current price becomes, the greater the reversion to, and generally beyond, the average. This is shown in the daily chart below.

Currently, the market is more than 11% above its longer-term daily average price. These more extreme deviations tend not to last an extraordinarily long time. Furthermore, reversions from these more extreme deviations tend to be rather quick.

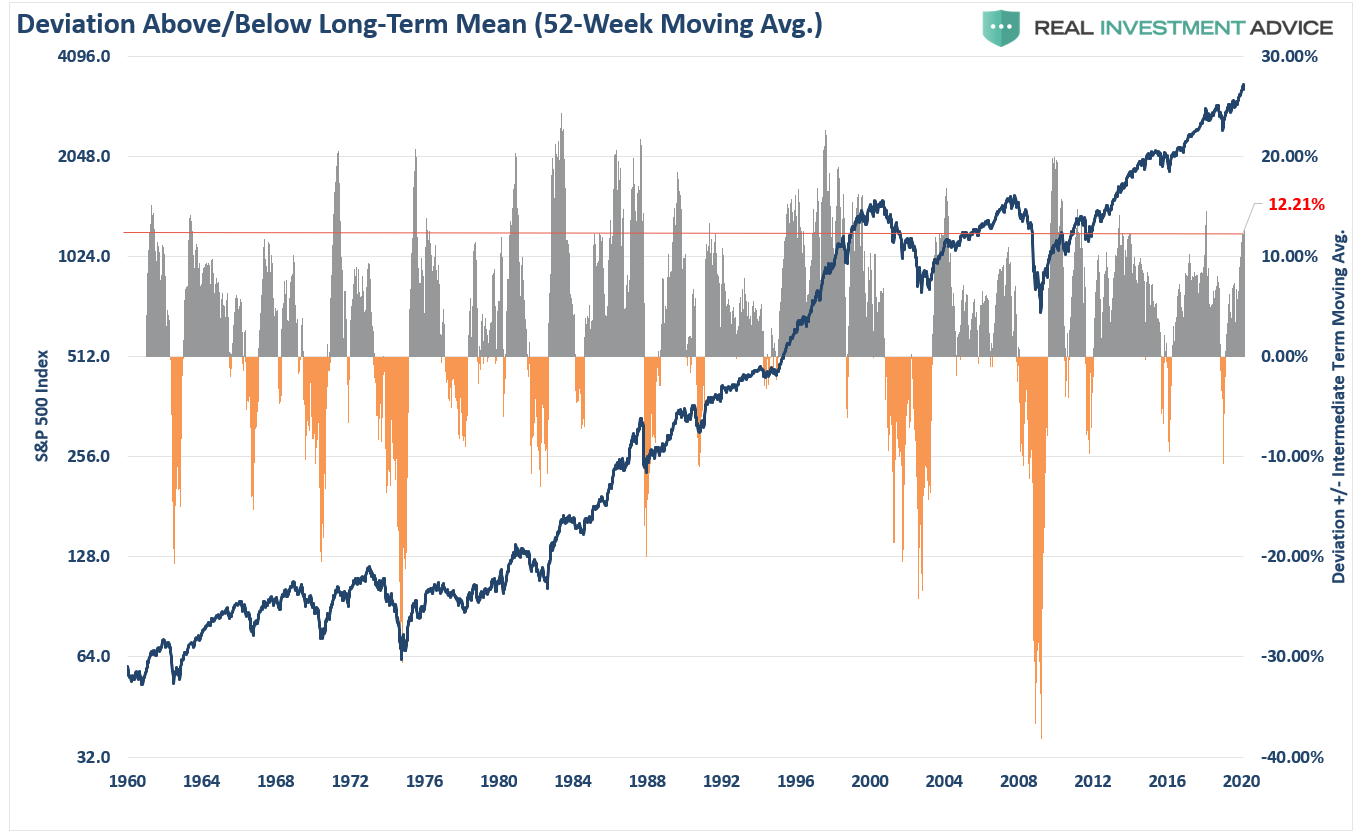

If we view a weekly basis, we see the same warning.

At more than 12% above the long-term weekly moving average, the market is currently pushing the upper end of historical deviations. There have been higher extremes for certain, but discounting risk often doesn’t end well.

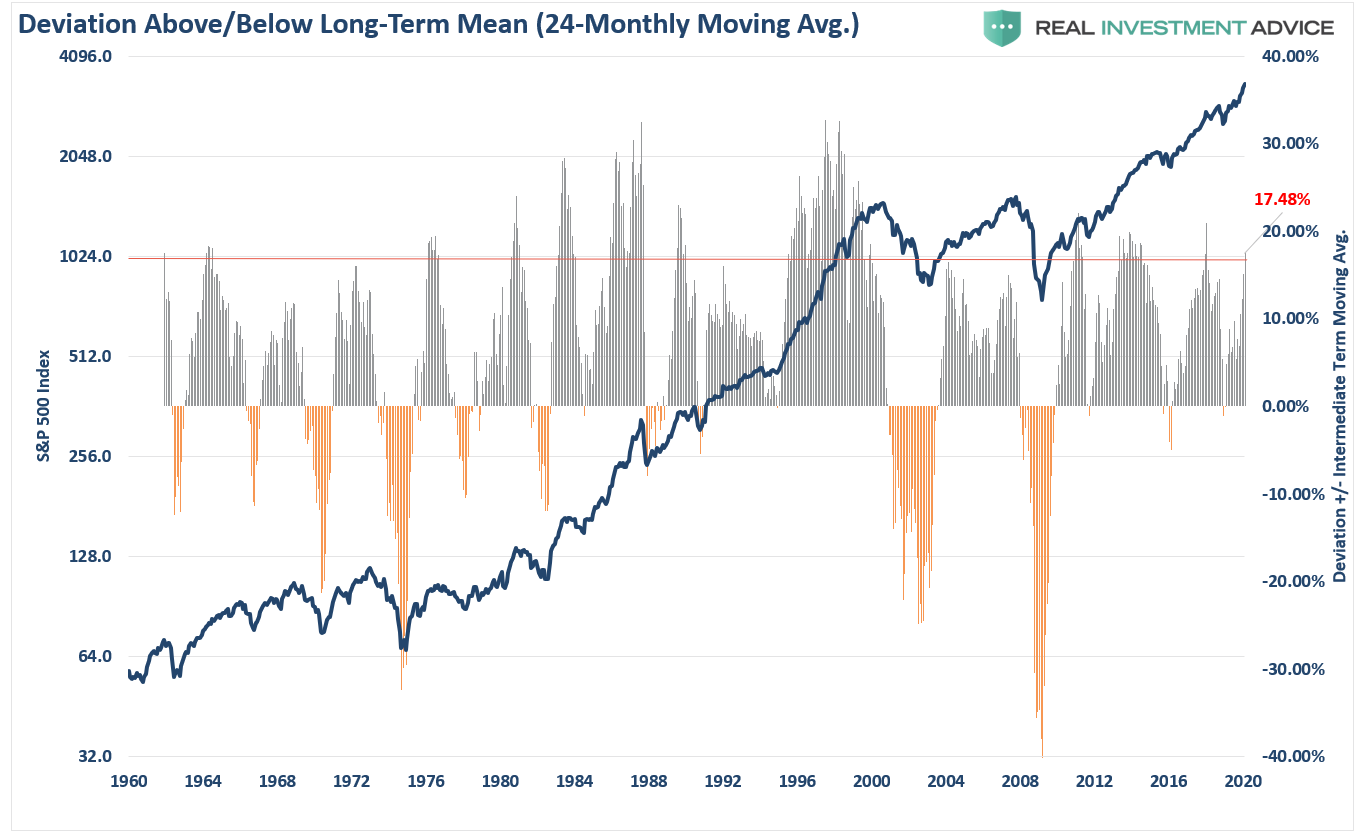

On a monthly basis, the almost 17.5% deviation is hitting levels more associated with drawdowns of 20% of more.

The important point to take away from this data is that “mean reverting” events are commonplace within the context of annual market movements.

Currently, investors have become extremely complacent with the rally from the beginning of the year and are discounting the potential global-supply shock from the “coronavirus.” The assumption that any disruption will be met by more Central Bank intervention, and higher stock prices, is a likely a risky proposition this late into an economic cycle.

In every given year, there are drawdowns that have wiped out some, most, or all of the previous gains. While the market has ended the year higher, more often than not, the declines have often shaken out many an investor along the way.

Let’s take a look at what happened the last time the market finished a year up nearly 30%. Over the next two years, the market consolidated with a near-zero rate of return.

From a portfolio management standpoint, the markets are very extended, and a correction over the next couple of months is highly likely. While it is quite likely the year will end positive, particularly given the current momentum push, taking some profits now, rebalancing risks, and using the coming correction to add exposure as needed will yield a better result.

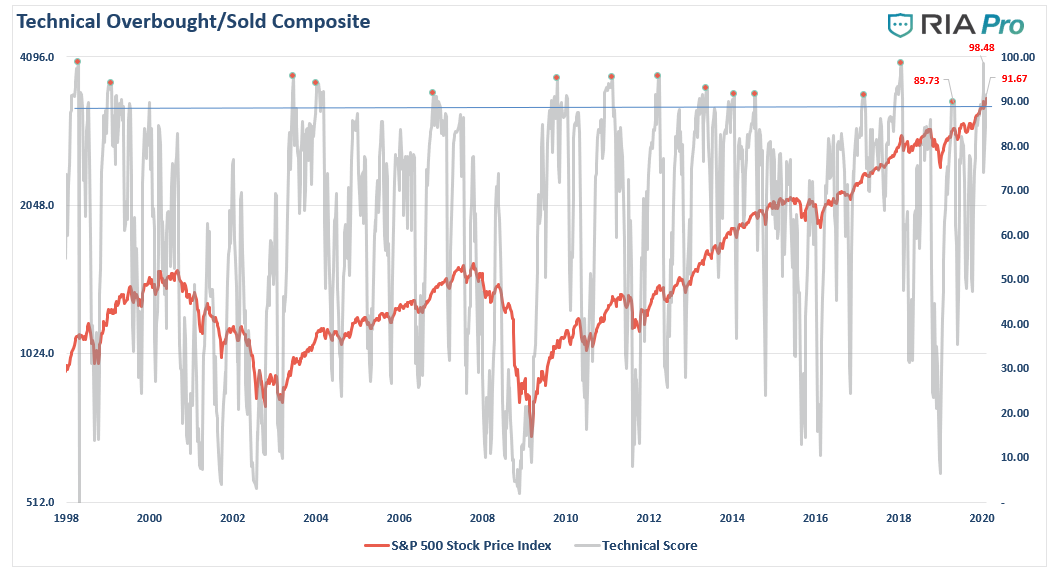

Warning 2 – Technical Warnings

The technical warnings also confirm our concerns about a near-term correction.

Each week, we post the chart below for our RIA PRO (Try Risk-Free for 30-days) subscribers, which is a composite index of our weekly technical measures including RSI, Williams %R, Stochastics, etc. Currently, the overbought condition of the market is near points which have denoted more significant corrections.

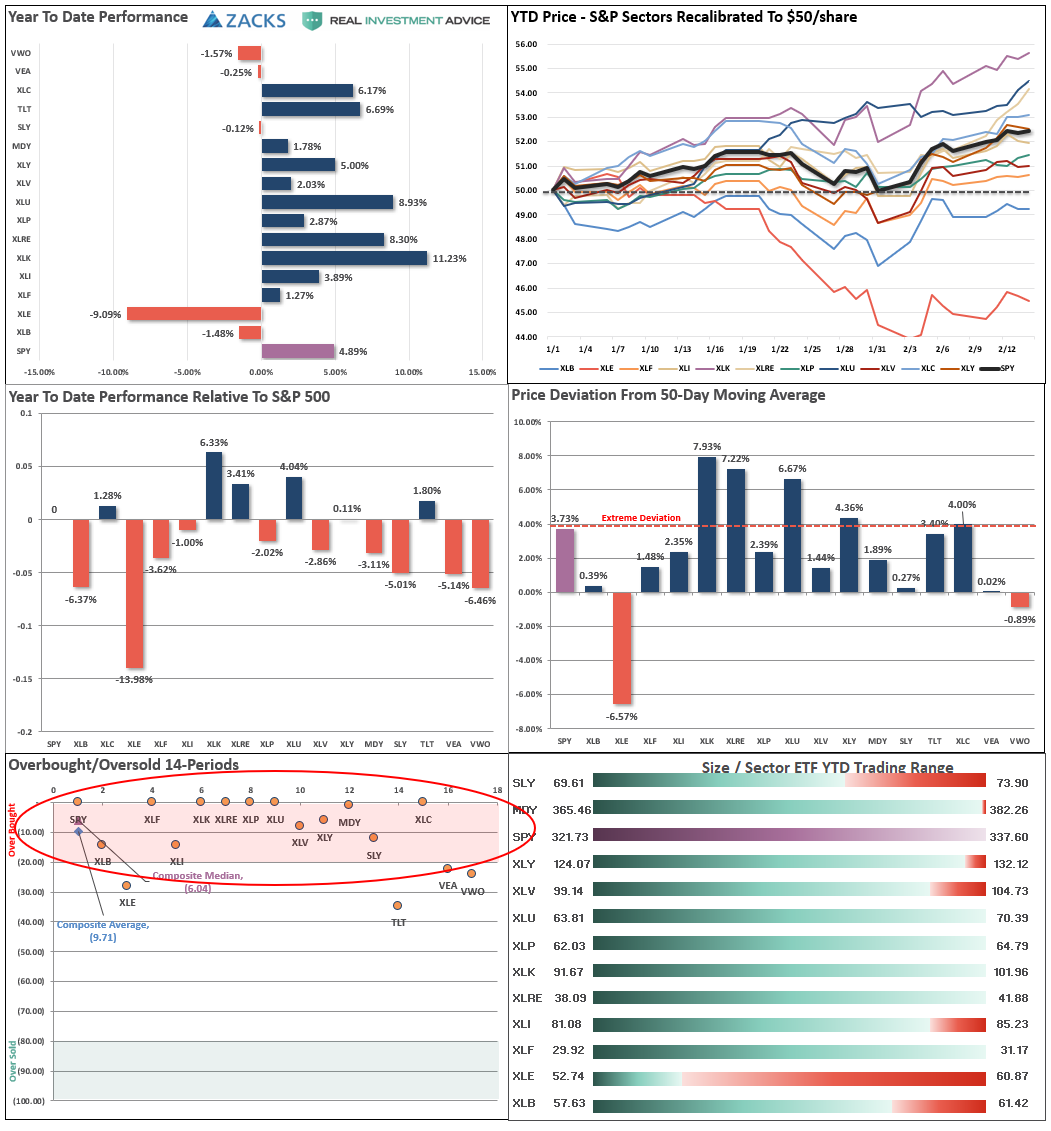

The market/sector analysis, which is also exclusive to RIA PRO members, shows the rather extreme price deviation in Technology, Real Estate, & Utilities. Also, relative performance shows that it has primarily been those three sectors providing a bulk of the “alpha” year-to-date. (Also, note the lower left-hand panel which shows virtually every sector back to extreme overbought.)

The market/sector analysis, which is also exclusive to RIA PRO members, shows the rather extreme price deviation in Technology, Real Estate, & Utilities. Also, relative performance shows that it has primarily been those three sectors providing a bulk of the “alpha” year-to-date. (Also, note the lower left-hand panel which shows virtually every sector back to extreme overbought.)

These are abnormalities that tend not to last long in isolation, and rotations tend to occur rather quickly.

Warning 3 – Economic Concerns

Just recently, Barbara Kolmeyer via MarketWatch discussed thoughts from Julien Bittel of Pictet Asset Management. He gives a pretty stern warning to the litany of economic bulls. To wit:

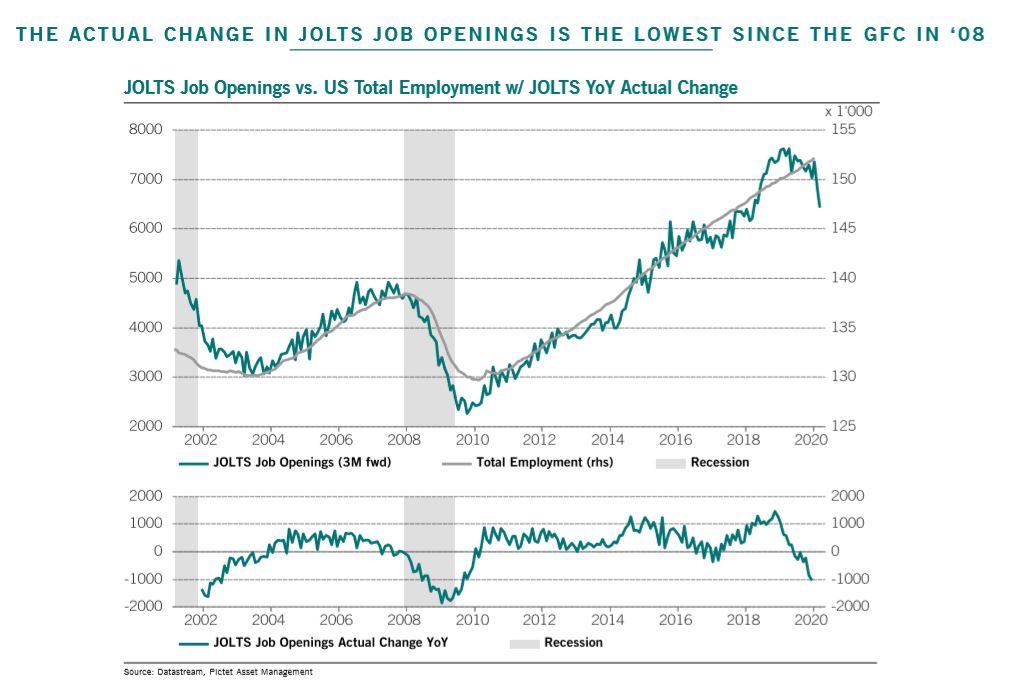

He sees a lot of similarities between what is happening now and the year 2000—the market peaked in the front half of the year, followed by a recession. Bittel has lots of charts to back up his case, such as this one showing Jolts job openings (which measures U.S. job vacancies), at the lowest since the Global Financial Crisis, often a bad omen for employment:”

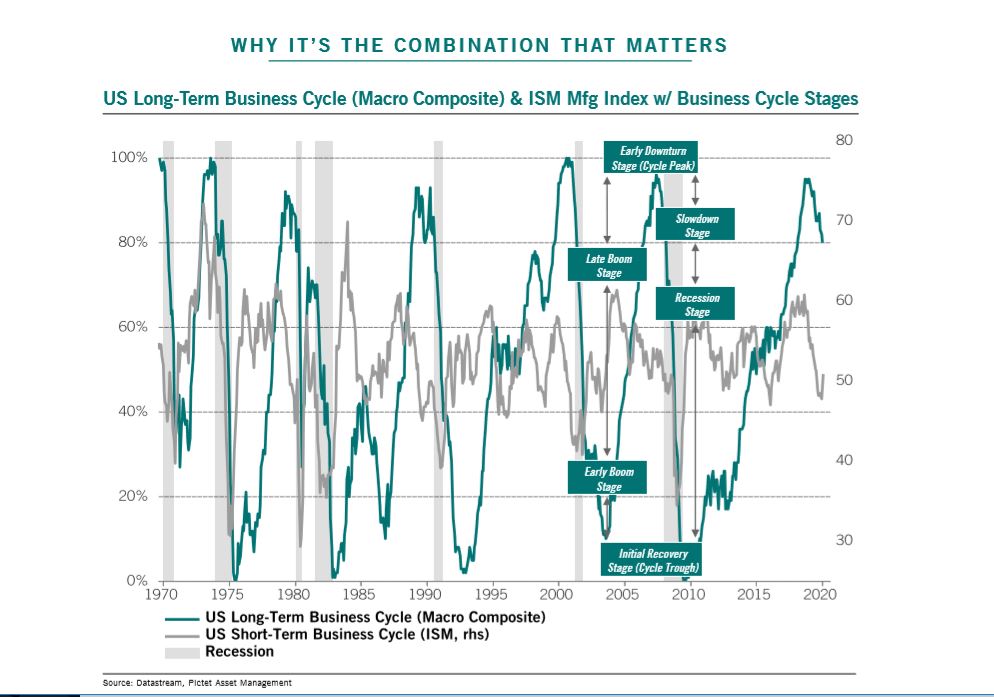

“He also highlighted trouble for the U.S. long-term business cycle, ‘linked to the less-cyclical areas of the economy so it’s the credit cycle, consumer confidence and the labor markets…these dynamics are all slowing,’ he said.”

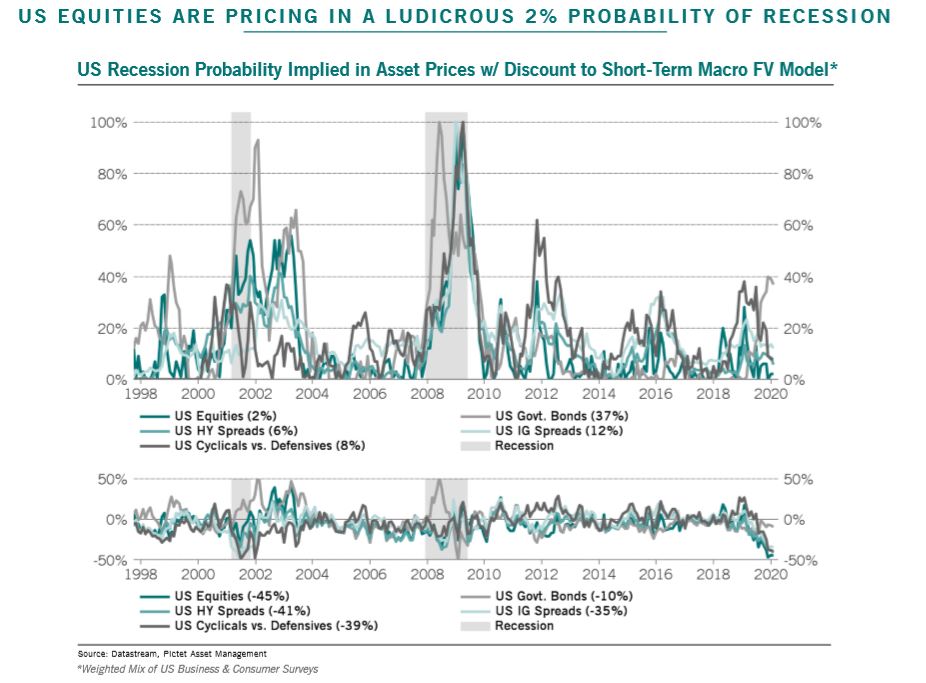

He said what makes his call so contrarian is that most economists see a 25% recession possibility, while equity markets are factoring in only a 2% chance.

“‘I think investors are a bit naive going into this year, thinking that the gravy trains or rainbows will continue, but in order for that to happen earnings need to come back in a big way. A sustained move in equity markets that’s driven by multiple expansion cannot maintain itself unless you get a huge recovery in earnings.” – Julien Bittel

Speaking of an earnings recovery, that is unlikely to happen.

Warning 4 – Earnings

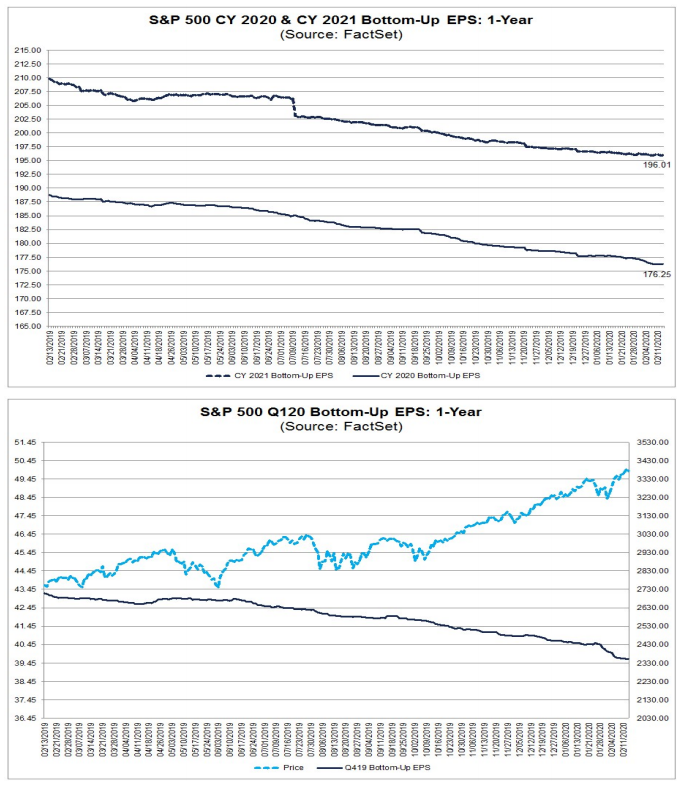

It is highly unlikely you are going to get a massive surge in earnings to support lofty asset prices and valuations particularly when you have a global supply-chain shock in progress. While the media has been fawning over the latest earnings season, it really isn’t what it seems.

As noted by FactSet:

“ For Q4 2019 (with 77% of the companies in the S&P 500 reporting actual results), 71% of S&P 500 companies have reported a positive EPS surprise and 67% of S&P 500 companies have reported a positive revenue surprise.”

Wow…that’s impressive and certainly would seem to be the reason behind surging asset prices.

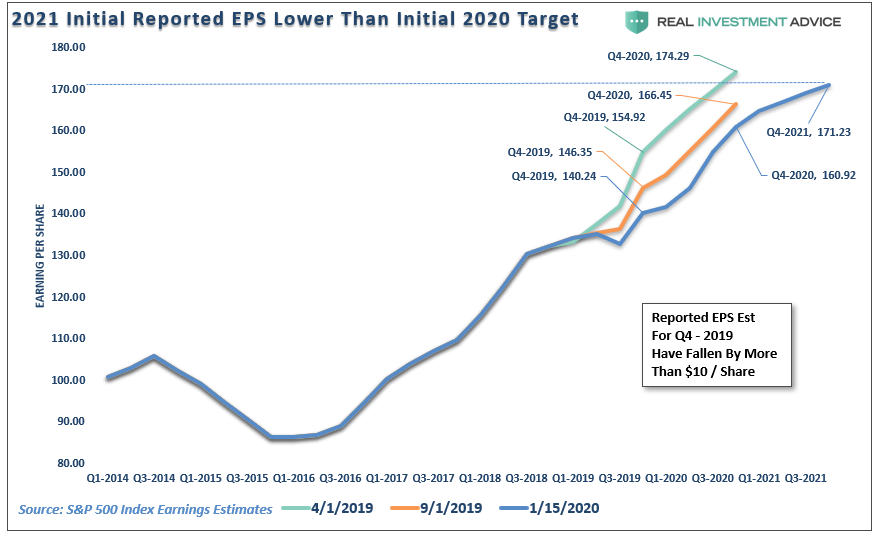

The problem is that “beat rate” was simply due to the consistent “lowering of the bar” as shown in the chart below:

Pay attention to the two charts above.

- Earnings declined in 2019 and are projected to continue to decline into 2021.

- Investors are not discounting the decline in earnings, and rising valuations, which will eventually become problematic.

Importantly, as I noted this past weekend:

“With equities now more than 30% higher than they were then, the Fed mostly on hold in terms of rate cuts, and “repo” operations starting to slow, it certainly seems that expectations for substantially higher market values may be a bit optimistic.

Furthermore, as noted above, earnings expectations declined for the entirety of 2019, as shown in the chart below. However, the impact of the “coronavirus” has not been adopted into these reduced estimates as of yet. These estimates WILL fall, and likely markedly so, which as stated above, is going to make justifying record asset prices more problematic.”

“Conversely, if by some miracle, the economy does show actual improvement, it could result in yields rising on the long-end of the curve, which would also make stocks less attractive.

This is the problem of overpaying for value. The current environment is so richly priced there is little opportunity for investors to extract additional gains from risk-based investments.”

If They Don’t “Buy & Hold” – Why Should You?

Here is the market for you, year to date:

- S&P 500 +4.62%

- Alphabet +13.74%

- Microsoft +17.53%

- Apple +10.92%

- Amazon +15.53%

- Tesla +91.24%

(Disclosure: We are long Apple, Amazon, and Microsoft in our equity portfolio.)

These “warning signs” are just that. None them suggest the markets, or the economy, are immediately plunging into the next recession-driven market reversion.

But as David Rosenberg previously noted:

“The equity market stopped being a leading indicator, or an economic barometer, a long time ago. Central banks looked after that. This entire cycle saw the weakest economic growth of all time coupled with the mother of all bull markets.”

There will be payback for the misalignment of funds.

Past experience suggests that future returns will be far less than historical averages suggest. Furthermore, there is a dramatic difference between investing for 30-years, and whatever time you personally have left to your financial goals. As noted yesterday, many investors are just now getting back to even.

While much of the mainstream media suggests that you should “invest for the long-term,” and “buy and hold” regardless of what the market brings, that is not what professional investors are doing.

The point here is simple.

No professional, or successful investor, every bought and held for the long-term without regard, or respect, for the risks that are undertaken. If professionals are looking at “risk,” and planning on protecting capital from mean-reverting events, then why aren’t you?

Copyright © RIA Pro