by Collin Martin, CFA, Fixed Income Strategist, Schwab Center for Financial Research

Key Points

- The compositions of many bond benchmarks have changed over the years.

- Just by tracking a benchmark bond index, investors may be unknowingly taking on more interest rate risk or credit risk than originally anticipated.

- When investing in bond funds, pay attention to the characteristics of the underlying bonds to make sure the duration and/or credit quality matches your investing horizon and risk tolerance.

Many bond benchmark indexes have gotten riskier.

Over time, the compositions of some of the key U.S. bond benchmark indexes have changed. Many indexes are now composed of bonds with longer maturities than in years past, while the number of lower-rated issues has increased, as well. This means investors may be taking more interest rate risk or more credit risk than they initially expected.

Below we’ll go over some of the key changes of three fixed income benchmark indexes, but first let’s discuss why this even matters.

The two key risks in fixed income investing

Interest rate risk and credit risk are two of the important risks when investing in the bond market.

- Interest rate risk is the risk that the price of a bond will fall if interest rates rise, as bond prices and yields move in opposite directions.“Duration” is a measure of interest rate sensitivity. All else being equal, the higher a bond’s duration, the more sensitive the bond’s price is to a given change in interest rates. The same is true for bond funds, which have an average duration based on the fund’s underlying holdings.

What does a higher duration mean in terms of prices? A simple rule of thumb when it comes to duration is that a bond's (or bond fund's) price will generally rise or fall by a magnitude of its duration (in percentage terms) for each percentage point change in its yield. For example, assume a bond has a duration of five. If its yield were to rise by one percentage point (say, from 2% to 3%), its price would fall by roughly 5%.

- Credit risk is the risk that a bond will default or will be downgraded, possibly resulting in a drop in its value. Bonds with low credit ratings tend to have higher credit risk, and their prices are usually more volatile than those with higher credit ratings—and that’s usually exacerbated during periods of broad market volatility or stock market sell-offs.

With that background on some of the key risks of fixed income investing, the changing composition of various benchmark indexes has generally resulted in more interest rate risk and credit risk for investors.

The broad bond market’s key benchmark has changed

The Bloomberg Barclays U.S. Aggregate Bond Index—commonly referred to as the “Agg”—is often considered the benchmark for the domestic bond market. It’s composed of U.S. Treasuries, agency mortgage-backed securities, agency bonds, and investment-grade corporate bonds.

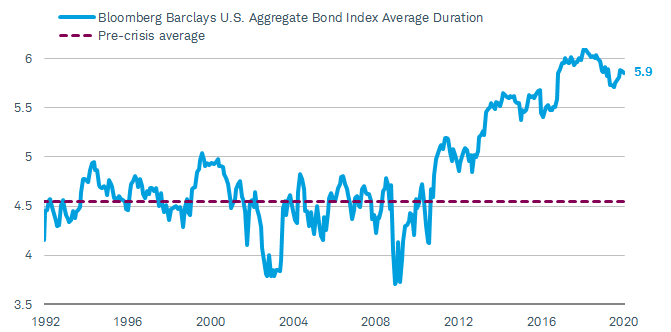

The average duration of the Agg rose sharply after the financial crisis, and is still near its all-time highs. The average duration of the Agg was 5.9 as of January 31,2020, well above its pre-crisis average of 4.5.

The average duration of the Agg is still near its all-time high

Source: Bloomberg, using monthly data as of 1/31/2020.

This has implications for investors who may use passive, index-tracking mutual funds or exchange-traded funds (ETFs), because the Agg is the likely the benchmark for many of these funds.

If you’ve been holding a fund that tracks the Agg over the years, that investment might have a lot more interest rate risk today than when you first invested.

If you’re looking to invest in the bond market today, and you’re looking for exposure to the broad, domestic bond market, the interest rate risk of many of these investments might be a lot higher than what you’re looking for.

The corporate bond market has experienced a similar trend

The investment-grade corporate bond market has witnessed a similar trend, but on an even greater scale. Both the interest rate risk and the credit risk of this market are at all-time highs.

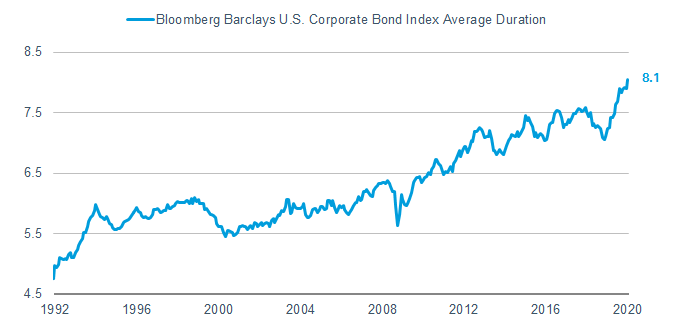

The average duration of the Bloomberg Barclays U.S. Corporate Bond Index is above 8.0, an all-time high. It has been trending higher for years.

The interest rate risk for investment-grade corporate bonds has never been higher

Source: Bloomberg, using monthly data as of 1/31/2020.

This trend is likely the result of the low-interest-rate environment we’ve been in for the past few years. With borrowing costs so low, corporations have been issuing more and more debt, and a lot of the debt has been issued with very long maturities, allowing firms to lock in these low rates for a really long time.

Credit risk is on the rise in the corporate bond market as well—the average credit rating of the Bloomberg Barclays U.S. Corporate Bond Index has been declining. Not only have corporations been increasing the average maturity of their debt, more and more lower-rated companies have been issuing debt as well.

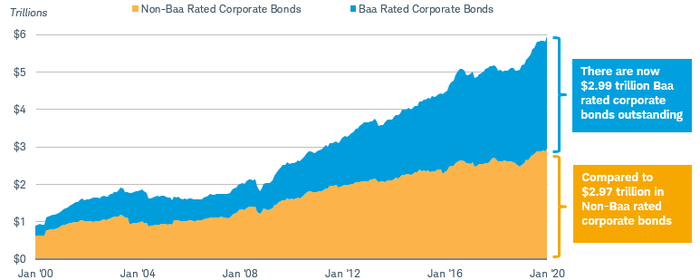

The “triple B” rating is the lowest rung of the investment grade scale. “Triple B” rated companies (those rated Baa by Moody’s Investors Services or BBB by Standard & Poor’s) now make up more than 50% of the investment-grade corporate bond market. In December 2007, they made up about a third of the market, and in 1999 “BBBs” made up just a quarter of the market. Yes, it’s still an investment-grade rating, but one rating lower is known as the high-yield, or “junk,” market. High-yield bonds have, historically, defaulted more frequently than those with investment grade ratings.

“Triple B” issues now make up more than half of the investment-grade corporate bond market

Source: Bloomberg, using monthly data as of 1/31/2020.

Just like with the Agg, an index-tracking approach in the corporate bond market might not make sense given your risk tolerance or investing time horizon. By investing in an investment grade corporate bond mutual fund or ETF that passively tracks the broad index, it may have more interest rate risk or more credit risk—or both—than you’d prefer.

What to do now

You may be taking on more interest rate risk or more credit risk than initially anticipated if you’re broadly tracking a bond index today.

If you’re considering broad, high quality bond market exposure like what the U.S. Aggregate Bond Index provides, consider that the interest rate sensitivity of that benchmark is well above its sensitivity years ago. Given our outlook for modestly higher longer Treasury yields later this year, we prefer investors favor bonds and bond funds with more short-term maturities.

For investment grade corporate bond investors, we prefer investors focus on investments with “A” ratings or better as market risks are increasing. We also prefer a more short-term bias when it comes to investment-grade corporate bonds, as the interest rate risk of the broad benchmark index is at an all-time high.

How can investors get the duration exposure we prefer? One way is to look for funds that are classified as either short or intermediate, according to Morningstar’s classification. A good place to start is either the Mutual Fund Select List or the ETF Select List. Short-term funds generally have average durations between 1 and 3.5, while intermediate-term funds generally have average durations between 3.5 and 6, so funds in the same category can have very different average durations. You can find the average duration of a given fund when researching funds on schwab.com by clicking the “Portfolio” tab. The average duration of the fund will be listed on the bottom.

Investors can also find information about the average credit quality of each fund’s holdings under the “Portfolio” tab. Given the large amount of “BBB” rated corporate bonds outstanding, many corporate bond mutual funds and ETFs will likely have a high weighting of holdings with that credit rating. Some funds do focus on the higher-rated parts of the market, but they are few and far between.