by Edward D. Perks, CFA, Franklin Templeton Investments

We as humans exhibit a fear of the exotic, yet complacency with the routine. We may refer to “just having a flu”, when every year, the flu on average kills 36,000 in the United States alone. Broadly speaking, deaths from epidemics are declining, even if news coverage often leaves out this important context.

Additionally, there’s been an explosion of technology since SARS (severe acute respiratory syndrome) first struck in late 2002. We can now take a specimen of the virus, put it in a nutrient, run the DNA against a library, and identify the virus in a matter of hours; a process which used to take days and weeks, thus speeding along the discovery and delivery of effective medical measures.

Despite the above, the outbreak of a new coronavirus strain (Novel Coronavirus or nCov for short) is creating havoc in China and heightened concern across the globe, and the World Health Organization (WHO) has officially declared it a health emergency. The death toll in China has been rising, and there are more global cases officially reported than during the SARS epidemic. The situation remains fluid.

Unexpected Shocks and Portfolio Diversification

As we entered calendar year 2020, several upcoming political and geopolitical events were already on our radar. The nCov outbreak was unexpected, and has reminded us of the need to maintain diversified portfolios.1 We have written about protecting portfolios from shocks from economic growth, inflation and interest rates, and believe the current situation will most likely be felt in assets which are tied to economic growth.

Unexpected Shocks and Investment Strategy

Unexpected shocks and volatility in asset prices can provide temptation to trade around news flow and emotion. Our investment process is designed to avoid these pitfalls and instead focus on our expertise, which centres around economic and market fundamentals. This does not mean that we ignore events like the nCov virus. Instead, we focus on how this event will affect the fundamentals and adjust our portfolio asset allocation accordingly.

Economic Impact of nCoV: What We Expect

We maintain that the broad global macroeconomic backdrop is improving, notably as growth is stabilising. However, we acknowledge that the nCov episode is making the stabilisation process much more difficult, and noisier.

We expect growth to experience an immediate hit in the first quarter of 2020, especially in regions most directly affected by nCov like China. However, we also expect a V-shaped recovery once the episode passes that should be supported by additional counter-cyclical policy measures. This catch-up period will likely offset any first-quarter weakness we see.

For reference, the SARS outbreak impact on China’s economy included slowing gross domestic product (GDP) growth from an average of 10.5% quarter-over-quarter (q/q), seasonally adjusted (saar) growth pace in the four quarters through the first quarter of 2003 to 3.4% q/q saar in the second quarter of 2003, followed by a significant rebound to an average of 13.5% q/q saar in the second half of 2003.2

Our team members on the ground are reporting that people in China have been cancelling their travel plans, curtailing social interactions, and foregoing outings. That is leaving restaurants, cinemas, theatres and hotels empty, with much-reduced traffic in the transport hubs that are still in operation. We are paying close attention to this reduced activity, as the Chinese economy has greatly evolved since 2003. Services and consumption account for a much larger portion of GDP growth today (chart below).

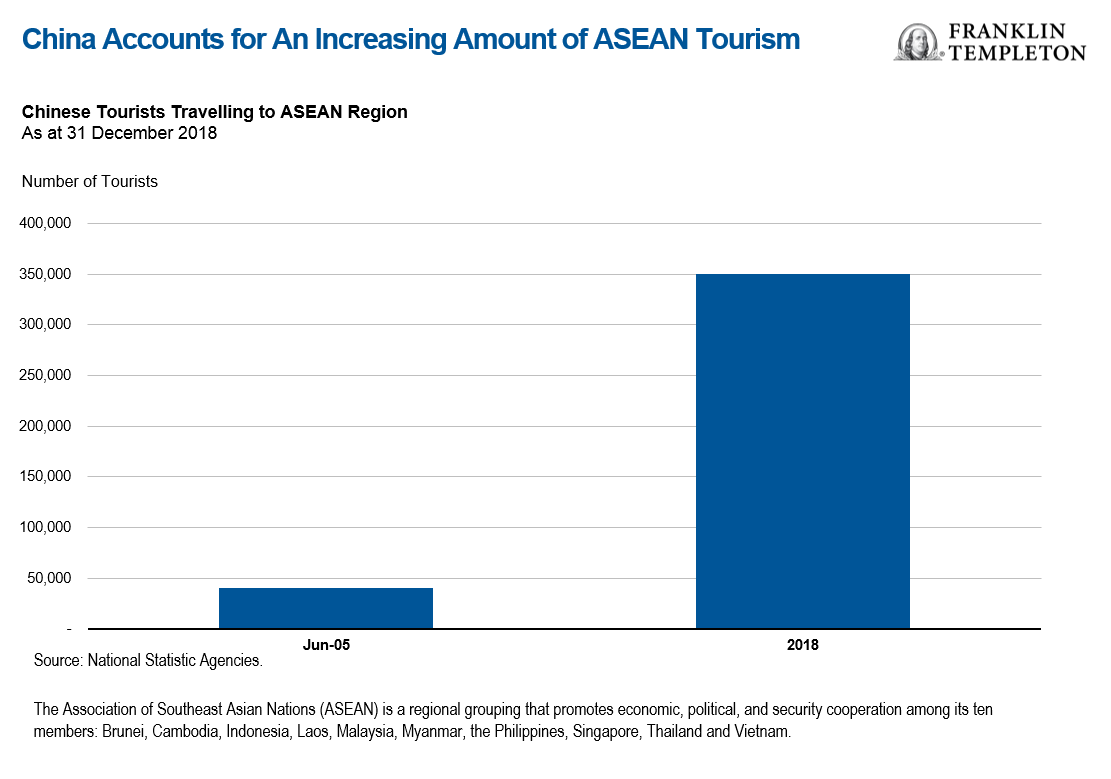

Furthermore, China’s influence over the world, particularly the Asian region, has dramatically increased over the past two decades. China has a large influence over global supply chains and accounts for an increasing amount of tourism. Any sort of slowdown in China will likely have ripple effects throughout the region.

The Market Impact of nCoV

The Market Impact of nCoV

We have seen that pandemics can produce volatile market reactions, with a tendency toward a sell-off and quick rebound, almost always offsetting the initial drawdown. We attribute these fierce V-shaped recoveries to the generous monetary and fiscal policies that have typically followed similar events. This is true both at the global level, and also at the local level where the episode has the most direct impact.

In our view, the biggest disparity in market impact will likely be regional instead of across the capital structure. Regionally, our preference from an investment standpoint would be to focus on markets that have both policy flexibility and are more insulated from the nCov epidemic.

Two such markets are the United States and United Kingdom; both are relatively closed economies in which trade contributes a smaller portion to GDP growth. Additionally, the United States and United Kingdom still can cut interest rates if policymakers need to respond to a growth slowdown.

On the other hand, the eurozone and Japan are more reliant on trade as a contributor to growth, and policymakers in these regions are also more stretched, with less room to counteract a growth slowdown.

Signals We Are Watching that Can Make Matters Better/Worse

The signals below would suggest we are more likely towards the end of the nCov episode:

- Growth rate of new cases peaks

- News coverage peaks (based on story counts)

- Improved testing results of vaccinations

- Hotter temperatures—it is more difficult for virus to survive in warmer weather

Some signals that would suggest the nCov health scare may get worse:

- Clarification that the virus can be spread during incubation stage (i.e. before a person is exhibiting symptoms)

- Greater evidence of spread beyond origin of Hubei Province

- Greater evidence that nCov is more deadly

We will continue to monitor this situation as it develops and remain nimble within our investment approach to this and other potential market shocks.

To get insights from Franklin Templeton delivered to your inbox, subscribe to the Beyond Bulls & Bears blog.

For timely investing tidbits, follow us on Twitter @FTI_Global and on LinkedIn.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as of publication date and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton Investments (“FTI”) has not independently verified, validated or audited such data. FTI accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FTI affiliates and/or their distributors as local laws and regulation permits. Please consult your own professional adviser or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton Distributors, Inc., One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com—Franklin Templeton Distributors, Inc. is the principal distributor of Franklin Templeton Investments’ U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

What Are the Risks?

All investments involve risks, including possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Bond prices generally move in the opposite direction of interest rates. Thus, as the prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline. Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments. Investments in emerging markets, of which frontier markets are a subset, involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated with emerging markets are magnified in frontier markets.

__________________

1. Diversification does not guarantee profit or protect against risk of loss.

2. Source: Bloomberg Economics.

This post was first published at the official blog of Franklin Templeton Investments.