by Edward D. Perks, CFA, Franklin Templeton Investments

Thoughts for 2020 and Beyond

Financial markets spent most of 2019 torn between signs that the current expansion is mature and optimism that policymakers stand ready to sustain growth in the years ahead. As we look ahead to the coming year, we retain a modestly cautious position, balancing the evident risks that lie ahead with the longer-term return potential of riskier and higher-yielding investments.

The slowdown in global trade that has been the dominant economic theme this past year may be showing signs of stabilisation, and investors are prepared to look favourably on the signs of détente in the US-China trade negotiations. Progress towards a trade deal, and whether it might be delivered before year-end, appears less certain but also an ever-changing feature of the investment landscape. We observe the evolving situation with interest but remain unconvinced on its near-term impact on growth.

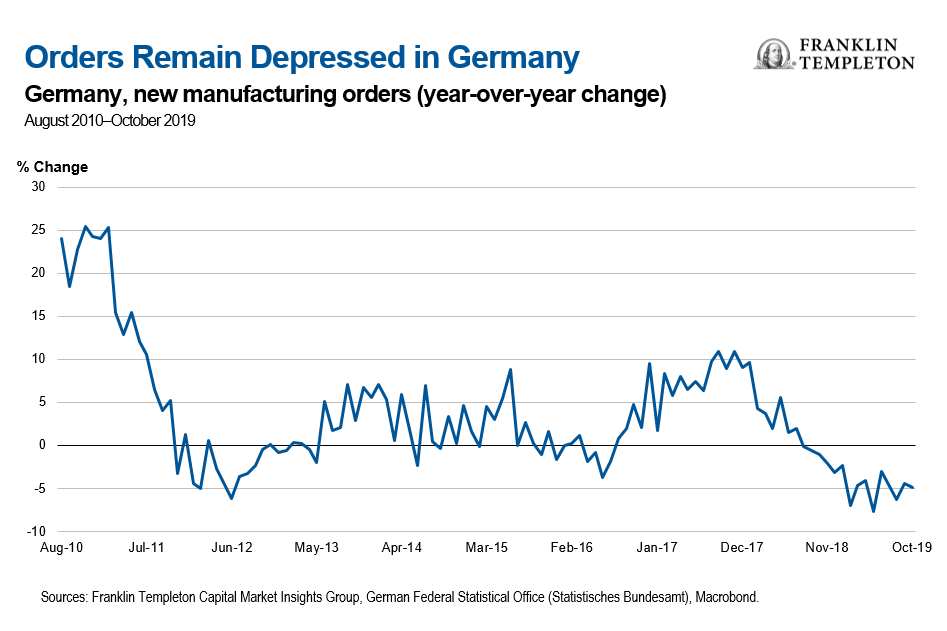

However, when we look to 2020 as a whole, we continue to view the balance of risks to global growth as being skewed to the downside, even as the worst fears of slowdown may have eased. Germany narrowly avoided a technical recession by posting the most modest of quarterly growth rates in the third quarter, after contracting in the previous period. This superficially good news might be viewed as easing the pressure to deliver additional fiscal stimulus in one of the eurozone countries with the greatest flexibility to do so. At the same time, the cumulative hit to confidence is gradually impacting the broader economy, and with factory orders remaining in a continued steady decline (see chart below), the headwinds remain evident.

Longer-Term Drivers of Growth

At our Annual Investment Symposium in November, we debated the longer-term themes that impact our analysis of the global economy. This saw the Multi-Asset Solutions team engage in collaborative dialogue with senior leaders and CIOs from across Franklin Templeton’s wide range of asset class specialists.

This year, our focus was on populism, debt levels and policy response in the next downturn. We noted that growth has disappointed this cycle, failing to deliver the broad increase in prosperity seen in earlier decades, compounding the rise of inequality. How policymakers respond to populism, and pressures such as climate change, will determine the long-term trajectory of absolute growth and relative prosperity.

The topics we discussed are complex and overlapping but help us understand the underlying dynamics that will drive macroeconomic outcomes over a longer investment horizon. Continued modest growth likely reflects the impact of deleveraging that has been felt globally initially in certain economies (Japan, exacerbated by adverse demographics) and, most significantly, specific sectors (US households). China’s deleveraging will likely perpetuate this dynamic moving forward.

However, we expect continued global growth and moderate inflation over the long term. With relatively few imbalances, and ongoing central bank stimulus measures, the global economy is less likely to see extreme swings in output. We continue to see only a moderate risk of a US recession in the next 12 months. For now, our proprietary indicators of growth momentum, in both developed and emerging markets, remain negative and the risks going into 2020 appear skewed to the downside. Our dominant investment theme is fundamentally unchanged as “Slower global growth remains a concern.”

Inflation Expectations Are Modest

We also focused on themes that color our outlook for inflation. The structural disinflationary forces that led to the great moderation have not disappeared, but their continued influence is being questioned. For example, the “Great Power” tensions evident in the rise of China may divert the steady march of technological progress and globalisation.

In the very long term, demographics will likely exacerbate the disinflationary impulse. This risks a downward shift in inflation expectations (“Japanification”) that may be reversed only by seemingly extreme policy actions. However, policy actions can influence the impact of secular trends, such as population dynamics. Decisions over immigration regimes and measures to expand female participation can help offset the impact of a declining workforce.

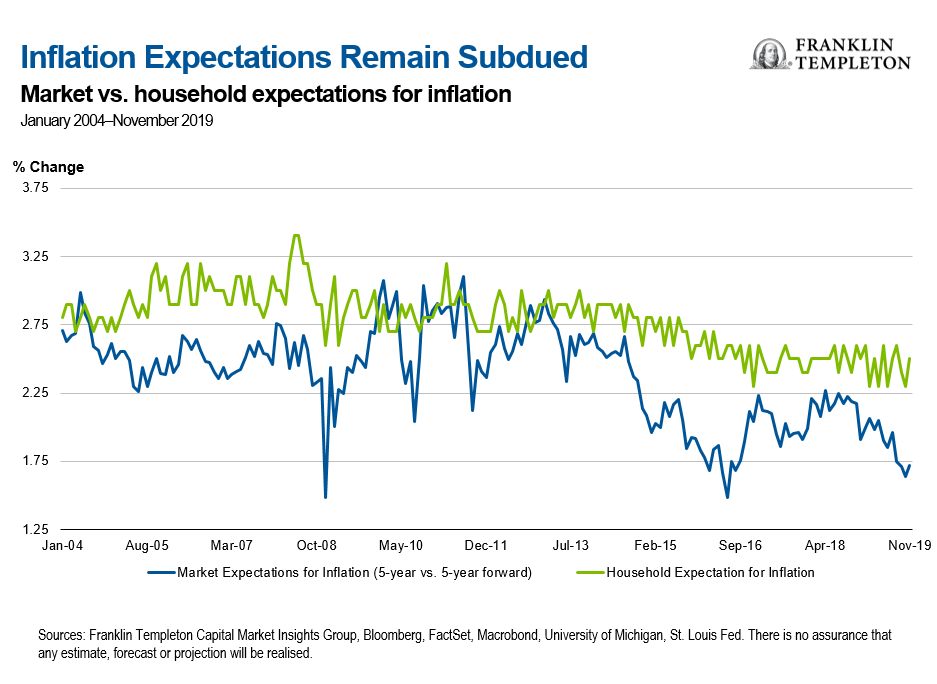

Market-based measures of inflation expectations, derived from the yields of nominal- and real-return bonds, have declined sharply this year. These so-called breakeven inflation rates (where the prospective return on nominal- and real-return bonds are equal) have responded directly to head-line inflation and commodity prices. Looking more deeply, the level of breakeven inflation over the five-year period starting five years from now (5-year/5-year forward rate) has remained depressed (see chart below). This may largely reflect a decline in the risk premium for inflation uncertainty, as government bond yields have fallen.

For now, we view the primary driver of inflation to be changes in demand. As a result, the headwinds for global growth are anticipated to cap inflation. This effect has been felt broadly, including in emerging markets, re-inforcing our theme that sees “Subdued inflation across economies.”

Policy Response in the Year Ahead

Among the themes that we debated was the likely policy response during the next recession. As we noted above, this probably isn’t a question for 2020. However, it is already helping to frame central banks’ thoughts about their mandates. Both the US Federal Reserve (Fed) and the European Central Bank (ECB) are engaged in reviews that could result in more symmetrical inflation targets.

Likewise, our discussion on the theme of populism showed a greater emphasis on the quality and distribution of growth than its level. Political and social imperatives such as environmental protection will require fiscal spending to be achieved, offsetting private sector deleveraging. Some central banks, notably the ECB, are increasingly supportive of more active fiscal policy to engineer these outcomes. However, we continue to question whether the political will exists to adopt such measures in the year ahead, or whether they can be delivered without a deeper slowdown and the fear of a renewed crisis in the eurozone.

Having paused its sequence of rate cuts in October, the Fed remains acutely aware of the need to be seen to stand ready to buy a little more “insurance” if necessary. Fed Chairman Jerome Powell indicated that the bar to further rate cuts had moved higher. But the bar to rate hikes was even higher still. Our outlook for asset markets remains more uncertain than usual due to the inherent tension between the need for stimulus and the fear encapsulated in our final major theme that we may be “Approaching the limits of monetary policy effectiveness.”

Practical Positioning: Nimble Management Required

We incorporate the longer-term themes that we discussed at our Annual Investment Symposium into our research process, helping to set the direction for our portfolios and the benchmarks that we agree upon with clients.

Over this longer-term horizon, we believe global stocks have greater performance potential than global bonds, supported by continued growth. Within bonds and equities, we believe there is stronger return potential for emerging markets. And with short-term interest rates and government bond term-premia remaining below historical averages, we see a lower performance potential from government bonds.

However, in managing portfolios today, we also need to reflect more immediate economic concerns and the dynamics that drive shorter-term market moves. Uncertainty over policy response and its efficacy leaves the outlook more clouded than usual. As we proceed towards the latter part of an unusually long economic expansion in the United States, we need to recognise that our longer-term outlook will not be reached along a smooth path. Markets are understandably focused on the probability that a recession might occur in the next few years.

Although we acknowledge the longer-term return potential for stocks and believe that they will earn their equity risk premium over time, we continue to point to shorter-term concerns that have tempered our enthusiasm. Against a backdrop of slower growth, global equities as a whole are not cheap, in our analysis. The cumulative effect of ongoing trade tensions leaves us concerned about investment and hiring plans, and we struggle to see catalysts for much stronger activity in a growing number of economies.

Having scaled back our cautious stance on risk assets last month, we retain a modestly lower conviction on global equities. Our view reflects the balance between longer-term attractions and some reasons for concern over valuations and diverging expectations across markets, but we are not overly bearish. We continue to believe that navigating the challenges the year ahead presents will require nimble management.

Bond Valuations Are Also Stretched

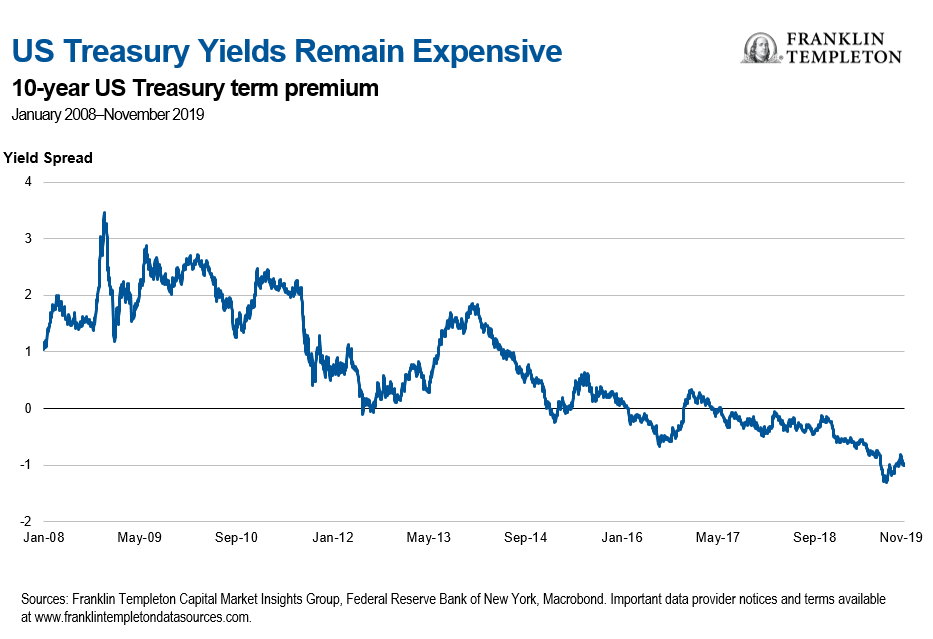

One of the most striking features of our longer-term analysis is that the return potential from global bonds, especially government bonds, is depressed. This largely reflects the fact that current yields are at historical lows. However, we note that depressed yields likely reflect demographics and demand for matching assets, which are likely to persist. This shows up in the “term premium,” the difference between the current bond yield and the average level for short-term interest rates over the life of the bond (see chart below).

In a multi-asset portfolio, we need to hold assets that provide the potential for diversification. Bonds traditionally fulfill that role. Global bonds—especially high credit quality and long- duration issues—appear vulnerable due to low term-premia and modest credit spreads for investment-grade corporate issues. However, slower growth and subdued inflation balance this in our neutral overall view of the asset class.

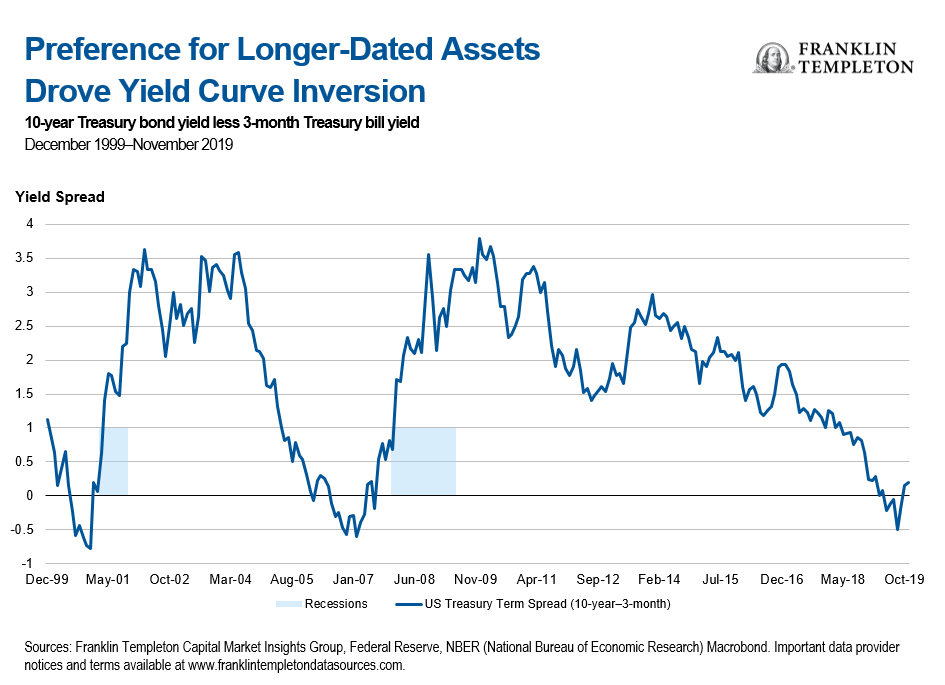

The yield curve inversions that occurred this year have left a bearish signal about the prospects for recession in the year or two ahead. Whether this occurs is an open question, and many investors point to reasons why it might be “different this time,” but the response of central banks will probably be key (see chart below). In part, we believe it is this bias towards cutting interest rates, even from the low levels already reached, that argues for a relatively evenly balanced portfolio of bonds and stocks at this time.

Opportunities and Threats in Emerging Markets

In both stocks and bonds, we believe the longer-term performance potential in emerging markets will exceed that of developed markets. This has been a persistent result of our analysis, but one that has been tempered in its application to portfolios in the recent past.

Emerging economies have demonstrated a much higher growth potential, notably in China and India. As these countries grow to comprise a larger part of the global economy and contribute a still larger share of global growth, we believe the structural tailwind is likely to persist over the very long term. In a world where the growth of earnings mainly drives equity return potential, we believe this should favour emerging market stocks’ return potential.

The range of starting points of various economies, and the manifold forms of populism that are already being seen, may present opportunities for active managers to take advantage of growing dispersion of outcomes. We believe strongly in the attractions of emerging markets as a venue for active management. Indeed, we would always start with a presumption towards active management in this area.

However, in the current environment of global trade uncertainty and with a less favourable outlook for commodities, we have scaled back our conviction on emerging market equities. Valuations remain attractive to us relative to developed market peers, but we see this balanced by reasons for caution. We do, however, retain a more optimistic view of local-currency emerging market bonds, especially in comparison to the opportunities available in lower-rated corporate credit in the developed world.

More generally, we continue to believe a return to long-run levels of volatility since early 2018, rather than the muted levels seen for much of the past 10 years, indicates that we have entered a new volatility regime. Such an environment may present headwinds for emerging market investments, and tempers our enthusiasm, despite longer-term attractions.

To get insights from Franklin Templeton delivered to your inbox, subscribe to the Beyond Bulls & Bears blog.

For timely investing tidbits, follow us on Twitter @FTI_Global and on LinkedIn.

*****

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as of the publication date and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market.

All investments involve risks, including possible loss of principal.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton Investments (“FTI”) has not independently verified, validated or audited such data. FTI accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FTI affiliates and/or their distributors as local laws and regulation permits. Please consult your own professional adviser or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

What Are the Risks?

All investments involve risks, including possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. The positioning of a specific portfolio may differ from the information presented herein due to various factors, including, but not limited to, allocations from the core portfolio and specific investment objectives, guidelines, strategy and restrictions of a portfolio. There is no assurance any forecast, projection or estimate will be realised. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Bond prices generally move in the opposite direction of interest rates. Thus, as the prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline. Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments. Investments in emerging markets, of which frontier markets are a subset, involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated with emerging markets are magnified in frontier markets. Derivatives, including currency management strategies, involve costs and can create economic leverage in a portfolio which may result in significant volatility and cause the portfolio to participate in losses (as well as enable gains) on an amount that exceeds the portfolio’s initial investment. A strategy may not achieve the anticipated benefits, and may realise losses, when a counterparty fails to perform as promised. Currency rates may fluctuate significantly over short periods of time and can reduce returns. Investing in the natural resources sector involves special risks, including increased susceptibility to adverse economic and regulatory developments affecting the sector—prices of such securities can be volatile, particularly over the short term. Real estate securities involve special risks, such as declines in the value of real estate and increased susceptibility to adverse economic or regulatory developments affecting the sector. Investments in REITs involve additional risks; since REITs typically are invested in a limited number of projects or in a particular market segment, they are more susceptible to adverse developments affecting a single project or market segment than more broadly diversified investments.

This post was first published at the official blog of Franklin Templeton Investments.