by Mike Pyle, Blackrock

Mike explains the importance of government bonds in building portfolio resilience and share tips on how to do so.

We see raising portfolio resilience as a key theme for investors – not only for this year but over a long term. It’s crucial to safeguard a portfolio against a variety of adverse conditions, especially in a time of elevated macro uncertainty. We view government bonds as key portfolio ballast, even after their yields have plunged.

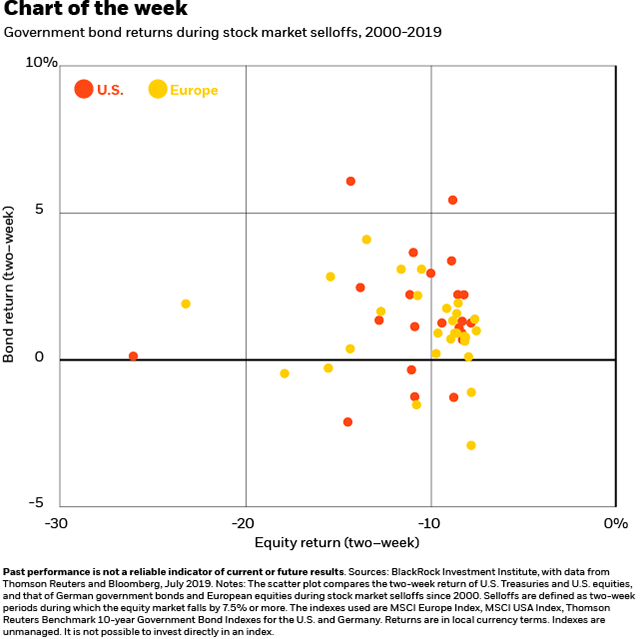

The hope when holding government bonds in a multi-asset portfolio: Bond prices should rise when stocks fall, cushioning the overall portfolio impact of “risk-off” episodes. This has generally been the case since 1980, according to our study of the correlation between the performance of U.S. Treasuries and stock market, and that of German government bonds and European stock market. There have been exceptions. Take the “taper tantrum” of 2013: Then Fed Chairman Ben Bernanke hinted at reducing post-crisis monetary stimulus, sending both stocks and bonds lower. But such events have been relatively uncommon, especially since the global financial crisis. The chart above shows the U.S. and German government bond performance during stock selloffs in their corresponding markets since 2000. We see government bonds providing important ballast against risk asset selloffs in the current environment, as trade and geopolitical frictions become a key market driver.

In search of ballast

The protection offered by global government bonds is still meaningful even as their yields have hit historical lows, in our view. Take German government bonds (or “bunds”), which have one of the lowest yields globally. The worry for investors: euro-zone policy rates–already in negative territory–may be nearing an “effective lower bound (ELB),” or the minimum level of interest rates that central banks can feasibly set. This would suggest there is little further room for bund yields to fall–and their prices to rally–during equity market selloffs. The ELB is tough to estimate and its level can change over time. Some studies, including one from Princeton economist Markus K. Brunnermeier, pin the euro area’s ELB around -1%. This (albeit highly uncertain) estimate would imply that euro area sovereigns still have some room for yields to decline, but they offer a thinner cushion than in the past against major equity shocks.

We see an important role for inflation-linked bonds, both as a ballast to equity selloffs driven by growth shocks and to underappreciated inflation risks. Inflation-linked bonds generally rally when equity markets sell off, like nominal bonds. The potential unravelling of global supply chains over a longer horizon, as a consequence of protectionist policies, could lead to an unwelcome mix of sluggish growth and higher inflation–and a difficult environment for both equities and nominal bonds. A blend of nominal and inflation-linked bonds in strategic portfolios can create resilience to a variety of adverse conditions. In addition, low inflation expectations have made inflation-linked bonds inexpensive, adding to their appeal.

We stress the importance of government bonds in building portfolio resilience, yet there are tactical considerations to take into account. We see potentially better entry points for U.S. Treasuries in the next few months relative to bunds, especially if the Fed’s policy meeting this week–or in coming months–moderates some of the excessive market expectations for easing measures. Tactically we favor European sovereigns with a preference for peripherals, given our view that the ECB is likely to meet–or even exceed–market expectations for further easing.

Mike Pyle is BlackRock’s global chief investment strategist. He is a regular contributor to The Blog

Investing involves risks, including possible loss of principal.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of July 2019 and may change as subsequent conditions vary. The information and opinions contained in this post are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This post may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this post is at the sole discretion of the reader. Past performance is no guarantee of future results. Index performance is shown for illustrative purposes only. You cannot invest directly in an index.

©2018 BlackRock, Inc. All rights reserved. BLACKROCK is a registered trademark of BlackRock, Inc., or its subsidiaries in the United States and elsewhere. All other marks are the property of their respective owners.

BIIM0719U-908872

This post was first published at the official blog of Blackrock.