by Raymond Jacobs, Franklin Templeton Investments

Undeniably, the digitisation of the retail industry over the last 10 years has dramatically changed traditional commerce. Keystrokes and mouse clicks have increasingly supplanted physical visits to corner stores and strip malls. Shoppers worldwide now have instant access to virtually unlimited selections of goods and services, from toothbrushes and razors to esoteric and bulky items like mattresses and televisions, delivered to their doorsteps often in 24 hours or less.

This new e-economy has had a ripple effect impact on commercial real estate, particularly commercial retail and industrial properties, felt across the United States, Europe, Latin America and Asia. This is the so-called “Amazon effect,” or “clicks versus bricks,” referring to the economic pressures put on traditional retail properties due to declining on-site traffic. While this impact on retail real estate is significant, the narrative associated with it often tends to emphasise the negative aspects—the closures of malls and big-box retailers.

What we think is overlooked is a vast redevelopment opportunity, particularly as it pertains to the space required to support “e-tail” business logistics.

When a Mall Closes a Warehouse Opens

As consumers of all ages embrace the convenience of online shopping, they have come to expect near-instant gratification in terms of product delivery. Goods of all sizes and types are delivered within 24 hours, and in some cases, less.

Consumers in Europe cited “best price,” “speed,” and “the ability to order anywhere and anytime” as the top three most-important factors driving their online shopping habits, according to Euromonitor’s syndicated Lifestyles Survey.1 E-retailers aim to meet this demand by securing warehouse and distribution space to house the inventory in as close proximity to their customer base as possible.

If inventory is no longer on store shelves, it must be kept somewhere.

To accommodate this growth, investors and developers around the globe are snapping up industrial-use land and buildings, as well as repurposing shuttered big-box stores and other old retail spaces into distribution hubs. We believe these so-called “last-mile” logistics spaces present a tremendous opportunity for investors possessing the resources and expertise to navigate this burgeoning real estate market.

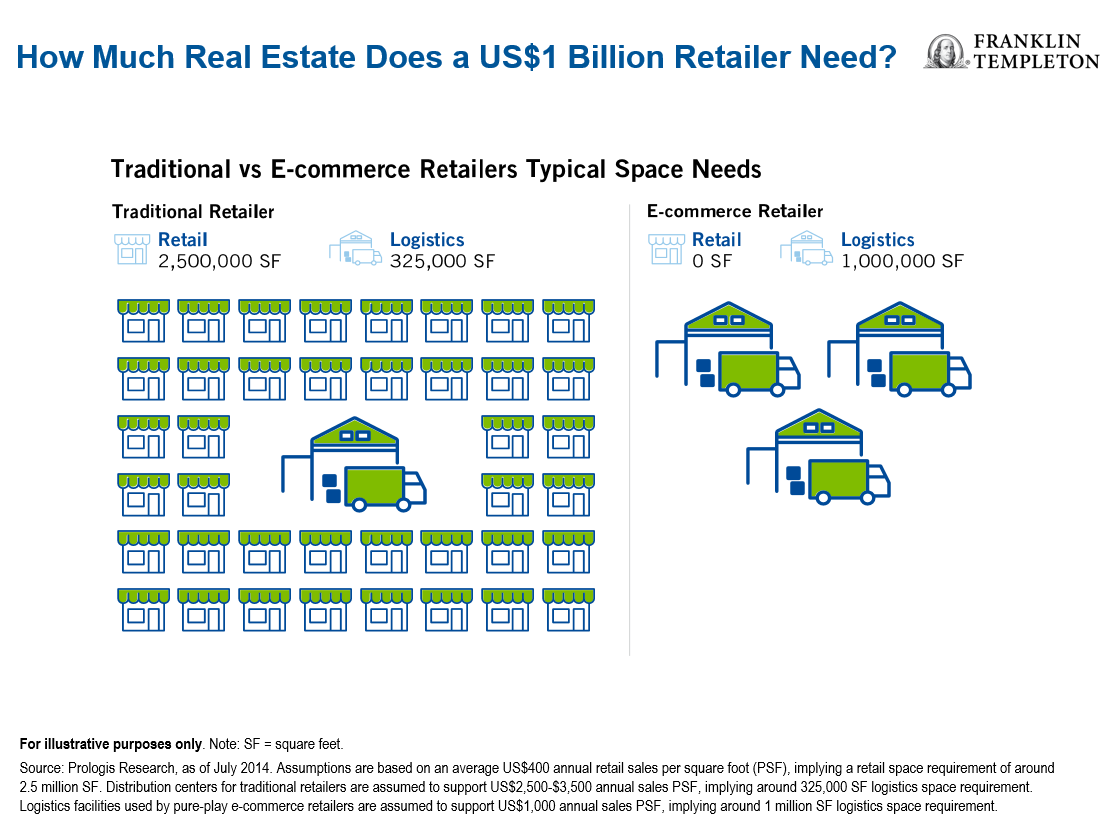

Some analysis suggests that e-commerce retailers require three times the logistics space of a traditional retail business. Assuming an online company generated sales of US$1 billion, for example, it would need more than 1 million square feet of warehouse space to support its fulfillment and distribution operations.2 A 2018 Industrial Labor report by CBRE predicts 184 million square feet of e-commerce logistics demand by 2020.3

Where Is the Last Mile?

While not a literal measured distance (naturally), the objective of “last-mile” logistics facilities is to situate them as close to the end consumer as possible—the closer the better in terms of rapid and efficient delivery of goods ordered online. Unlike sprawling fulfillment centers typically built in regional distribution hubs, newer last-mile logistics sites are usually situated in densely populated areas.

Demand for this coveted space is high. For example, in an analysis of the location of last-mile facilities in the 15 largest metropolitan areas in the United States, sites ranged from six miles from the city centre in the San Francisco Bay area to nine miles from the city centre in the Inland Empire of Los Angeles.4

In Asia, logistics rental growth is highest in Melbourne, Shanghai, Beijing and Hong Kong. Demographic trends—such as baby boomers retiring in cities and the growth of tech-savvy millennials—have resulted in a concentration of buying power in metropolitan areas.

In some parts of the world, last-mile logistics presents an even greater challenge for companies. Consider Indonesia, for example, where smaller local hubs located closer to customers on various islands in the country are needed.

Finding New Use for Old Spaces

The growing demand for last-mile logistics space has opened a new frontier in terms of investment and redevelopment opportunities for previously vacant or under-utilised properties—such as empty big-box retail lots, old government facilities, abandoned industrial sites in various stages of remediation and under-used office space. More often than not, last-mile deals involve buying existing buildings and converting them.

This offers an opportunity to acquire assets from pressured retailers and create value through adapting the use and tenant mix in response to logistics demands.

In one unique case, an under-utilised parking garage in Chicago was converted into a last-mile hub. Millennium Parking Garage, one of the largest underground parking systems in the world with 3.8 million square feet over two floors,5 was recently partially transformed into a shipping/warehouse location.

Also in the United States in Bayonne, New Jersey, owners converted a 90-acre former Naval base abandoned since its closure in 1999 into a warehouse. Repurposing the site created millions of dollars of tax revenue for Bayonne, brought jobs to the city and revitalised a waterfront that had fallen into decay.

Enabling the Movement of Goods

Interestingly, factors that once dictated the viability of a site for industrial use at the turn of the 20th century are again deemed to be important when considering warehouses for last-mile logistics. These include easy access to transportation, proximity to urban areas filled with potential customers and employees, access to waterways, appropriate zoning, rail service, etc.

Consider the converted Bayonne site as an example. It is across the river from New York City, possesses a private rail line, is zoned for commercial/industrial use and is adjacent to a major shipping route into New York City.

To capture a share of the e-commerce market, some traditional big-box stores still in operation are adapting their business models to use current real estate to serve as last-mile sites.

For example, 70% of the US population lives within five miles of a physical Walmart store. The company is using these traditional stores as e-commerce hubs by incentivising customers to buy goods online, but then pick up merchandise at their neighbourhood store without paying shipping charges.

The Real Estate Opportunity

Demand for last-mile real estate, particularly in densely populated suburbs and metropolitan centres, has spiked in recent years. Investors and tenants are now competing for small previously obsolete class-B, -C and -D industrial buildings in urban areas.

Revenue from logistics infrastructure in the Asia-Pacific region is predicted to grow by a compound annual growth rate (CAGR) of 7.6% between 2018 and 2025.6 This is more than double the rate of expected growth in North America and Europe over the same period.7

In Asia, in the coming years we anticipate a steady increase in investments in warehouses, industrial parks and ports in countries associated with China’s Belt and Road initiative.

In the United States, the supply/demand imbalance is especially acute in the western part of the country, where light-industrial rents (a good proxy for last mile) have grown by more than 10% annually in 2016 and 2017.8

In the European market, e-commerce logistics demand continues to be a key driver of real estate performance as well. BNP Paribas estimates that 13% of all commercial real estate investment is logistics-related.9 Three out of the top 10 performing cities in global rental growth for logistics markets are in Europe: Rotterdam, Budapest and Prague.10

Investment Considerations

Sourcing and selecting suitable industrial sites for use as last-mile logistics distribution centres presents a specific set of challenges. We think proper due diligence can go a long way towards selecting investments.

In our view, last-mile capability sites should have the following characteristics: be close to end-users and employee bases, be adequate in size, have good parking and access, have appropriate ceiling heights, loading areas, enough heating, ventilation and air conditioning (HVAC) and electrical systems, and the capability to sustain heavy floor loads.

It is important to note that industrial properties, especially sites formerly utilised for manufacturing purposes, can pose a wide range of environmental concerns. Hazardous waste generation, underground and above-ground storage tanks, oil/water separators, fueling operations, vehicle maintenance activities and waste disposal are also factors to be considered.

Specialists can help identify building deficiencies and evaluate suitability of building sub-systems, as well as quantify potential risks posed by former property usage.

Converting big-box sites and retail sites to warehouse space can also be challenging due to zoning laws and restrictions. Distribution centers present the possibility of noise and heavy freight traffic.

There are other considerations in different markets that may be overlooked. In the United States, for example, distribution centres are considered “commercial facilities” under the Americans with Disabilities Act. As such, they are such subject to accessibility standards. This affects parking ratios, building entry points, doorways and hallways, curb heights, etc.

Ultimately, however, we believe these “last-mile” properties can offer a compelling opportunity to those who can manage and navigate these challenges.

As e-commerce continues to penetrate global markets, we believe the shift from physical retail real estate to industrial logistics space will persist. We view this as a quality investment opportunity for those well positioned globally to negotiate the varied and complex landscape.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The companies and case studies shown herein are used solely for illustrative purposes; any investment may or may not be currently held by any portfolio advised by Franklin Templeton Investments. The opinions are intended solely to provide insight into how securities are analyzed. The information provided is not a recommendation or individual investment advice for any particular security, strategy, or investment product and is not an indication of the trading intent of any Franklin Templeton managed portfolio.

This is not a complete analysis of every material fact regarding any industry, security or investment and should not be viewed as an investment recommendation. This is intended to provide insight into the portfolio selection and research process. Factual statements are taken from sources considered

reliable, but have not been independently verified for completeness or accuracy. These opinions may not be relied upon as investment advice or as an offer for any particular security. Past performance does not guarantee future results.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton Investments (“FTI”) has not independently verified, validated or audited such data. FTI accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments opinions and analyses in the material is at the sole discretion of the user.

What Are the Risks?

All investments involve risks, including possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. The risks associated with a real estate strategy include, but are not limited to various risks inherent in the ownership of real estate property, such as fluctuations in lease occupancy rates and operating expenses, variations in rental schedules, which in turn may be adversely affected by general and local economic conditions, the supply and demand for real estate properties, zoning laws, rent control laws, real property taxes, the availability and costs of financing, environmental laws, and uninsured losses (generally from catastrophic events such as earthquakes, floods and wars). Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions.

Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments; investments in emerging markets involve heightened risks related to the same factors. To the extent a strategy focuses on particular countries, regions, industries, sectors or types of investment from time to time, it may be subject to greater risks of adverse developments in such areas of focus than a strategy that invests in a wider variety of countries, regions, industries, sectors or investments.

_____________________________

1. Source: Euromonitor International, Lifestyles Survey Report, September 2017.

2. Source: Prologis Research, E-Commerce and Logistics Real Estate, Inside the Global Supply Chain: E-Commerce and a New Demand Model for Logistics Real Estate, July 2014.

3. Source: CBRE Research, Industrial & Logistics Labor Report, The U.S. Supply Chain Quandary: Finding Enough Workers for An Expanding I&L Sector, 2018.

4. Source: CBRE Research, “Last-Mile: Concept or Measurement,” U.S. Market Flash, 11 July 2017.

5. Source: Phillips, E. “E-Commerce Companies Get Creative in Quest for ‘Last Mile’ Space,” The Wall Street Journal, 9 December 2018.

6. Source: JLL, Logistics: Beyond Warehousing, Why industrial and logistics are the next big think in Asia, 2018. There is no assurance that any estimate, forecast or projection will be realised.

7. Ibid.

8. Source: CBRE Research, “What is the Last Mile: The Definitive Guild to Omnichannel Real Estate,” www.cbre.us, 2018.

9. Source: BNP Paribas Real Estate, Property Report, European Logistics Market, February 2019.

10. Source: Prologis Research, The Prologis Logistics Rent Index, 2018: Broadening Global Growth, January 2019.

Copyright © Franklin Templeton Investments