by Avi Hooper, Senior Portfolio Manager, Invesco Canada

The economic implications from an inverted yield curve may be overstated, in our view. Historically, when short-term interest rates, anchored by central bank policies, yield more than longer duration maturities the bond market is signaling that monetary policy has become restrictive. Taking on more interest rate risk in your portfolio for less yield to maturity is an unattractive option for investors.

On the Invesco Investment Grade team, our economic outlook for the Canadian economy is subdued, but not recessionary. The Bank of Canada reduced its forecast for gross domestic product (GDP) growth in 2019 to 1.2% as global trade frictions are hurting exports and consumers are saddled with high levels of household debt. Nevertheless, job growth continues to remain very strong and wages are rising, ensuring a sustainable level of expansion over the forecast horizon. Inflation trends are slowing, leading to the market pricing some probability of rate cuts this year. In the Canadian government bond curve, this inversion is most acute in the five-year part of the curve.

Globally, the stock of negative-yielding debt grew by +1.2% in May to US$10.6 trillion.1 The global search for positive yield has made North American bond markets attractive. Capital inflows from Europe and Asia have been a major technical force in 2019, leading to outsized bond market returns. Market technicals can overwhelm fundamentals in the economy for periods of time. Curve inversions have long lead and lag times in predicting recessions. For this reason, they are an unreliable signal for managing portfolios, in our view.

Slowing growth, but not recession, and low inflation remain positive tailwinds for company earnings. Corporate bond valuations are no longer as attractive as they were in the final quarter of 2018, but many pockets of opportunity globally continue to surface.

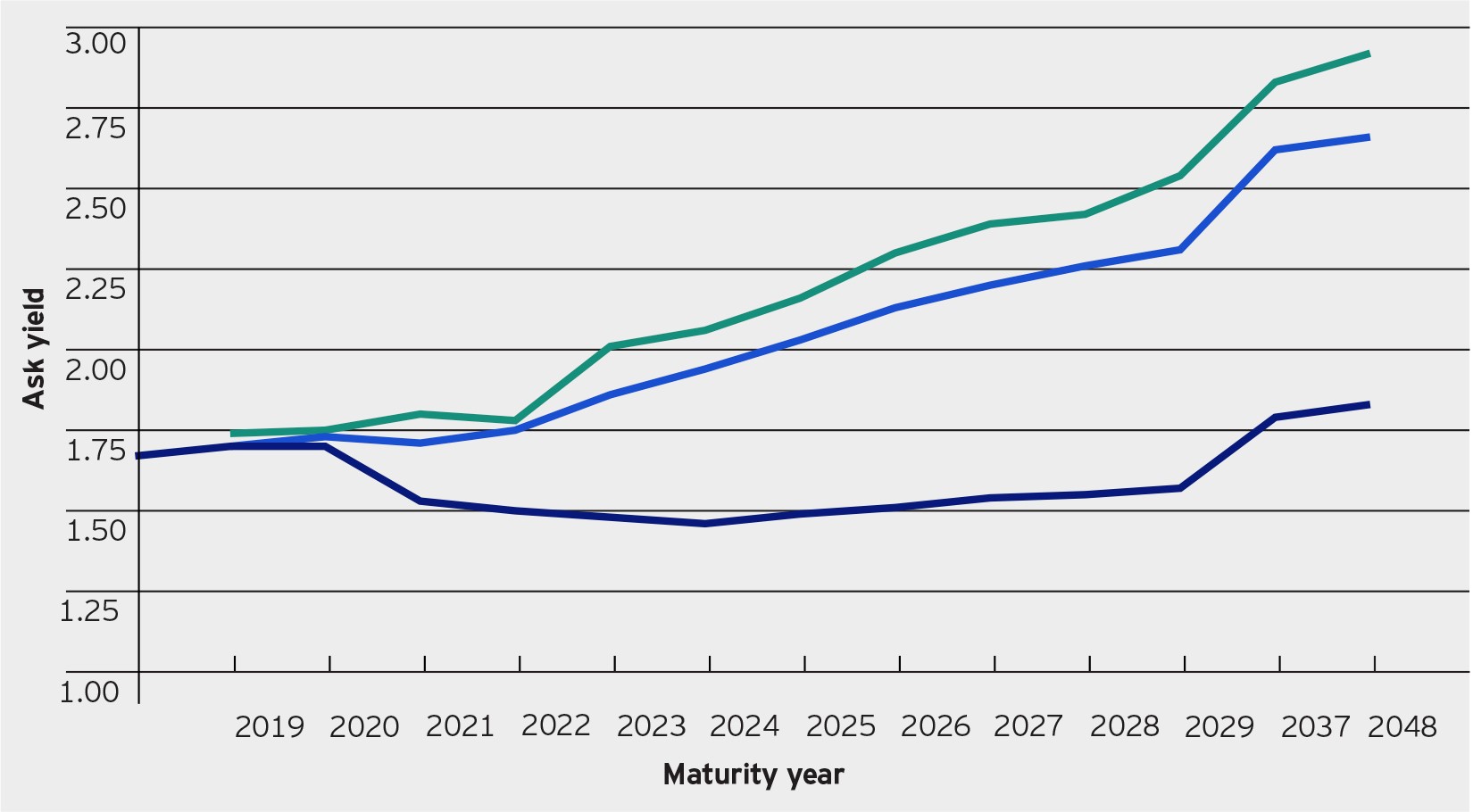

Keep in mind, there are hundreds of yield curves globally. Currently, In Canada, only the Government of Canada yield curve is inverting – highly rated Provincial and Municipal bond curves have been steepening.

Source: Bloomberg, as at May 28, 2019. Ask yield refers to the yield a bond would pay if purchased at the seller’s asking price.

We have no exposure to low-yielding, federal government debt in our portfolios, instead maintaining the portfolio risk ballast from fixed income and maximizing yield by capturing these steeper curves in regional government debt markets. We are also taking advantage of steeper corporate credit yield curves by adding duration in our best ideas globally.

This post was originally published at Invesco Canada Blog

Copyright © Invesco Canada Blog