by Russ Koesterich, CFA, Blackrock

Markets are not too expensive, or too cheap. As Russ explains, that offers a clue into what could cause the next move.

Stock markets have been more wobbly of late. While the proximate cause was an unexpected deterioration (collapse?) in trade talks with China, many investors were getting nervous even before the most recent barrage of tweets. Some were understandably skeptical of a rally that took U.S. equity indexes up 25% in four months.

The skepticism was further compounded by the fact that the rally was entirely driven by multiple expansion, i.e. paying more for a dollar of earnings.

Given this dynamic, and apart from any trade risks, have stocks simply become too expensive? Surprisingly, the answer is not necessarily.

The S&P 500 Index is currently trading at roughly 17 times next year’s earnings (as measured by price-to-earnings ratio, or P/E) and a little under 19 times trailing earnings. Today’s valuation is high but not extreme.

The P/E on the S&P 500 is slightly above the post-crisis average and modestly above the long-term average. That said, today’s valuation is roughly 20% below the January 2018 peak and roughly 35% below the 1999 top.

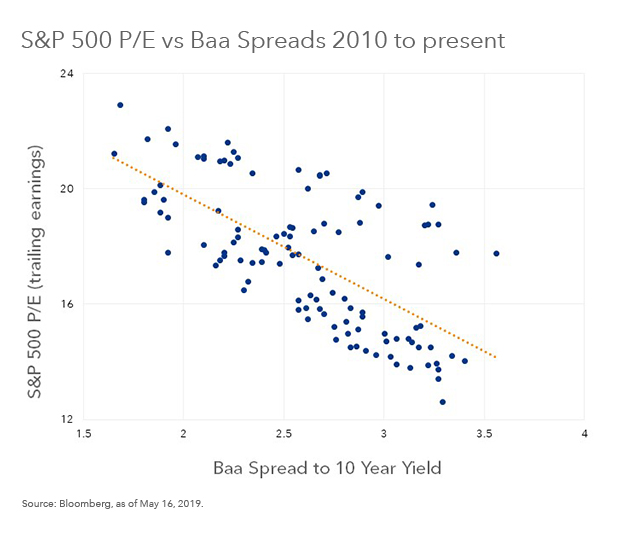

Valuations in comparison to market conditions

More importantly, how do today’s valuations compare against market conditions? As I’ve discussed in the past, valuation is conditional on the environment. Investors may be more or less willing to pay up for stocks depending on financial conditions, growth expectations and inflation. Looking across six different models, which on average explain about 40% of the variation in multiples, current valuations look about right.

Going into a bit more detail, stocks look most expensive based on the level of economic growth relative to expectations, i.e. economic surprise indexes. To the extent U.S. economic data has generally been trailing expectations, you would expect stocks to trade about 10% cheaper than they currently are.

Conversely, relative to consumer confidence, one of the better coincident factors in the post-crisis regime, stock valuations look about 10% too cheap. Most of the other metrics, which are primarily different versions of financial conditions, suggest that the P/E on the S&P 500 is almost exactly where you would expect it to be (see Chart).

What could change the outlook?

Obviously a change in conditions, apart from the impact on earnings, would suggest some re-calibration in equity multiples. The worst scenario would be a combination of slower growth and some tightening in financial conditions. A surge in the dollar would also be a risk to watch. Another very real possibility: a prolonged trade dispute, particularly if tariffs cause a sustained bump in inflation. This would inhibit both growth and the Federal Reserve’s latitude to adjust monetary conditions.

On the other hand, a more benign scenario would be a pre-emptive easing by the Fed. Under this scenario, easier financial conditions would help stocks, even if growth slowed a bit.

To be clear, none of the above suggests that investors should rush out to buy stocks or sell based on the notion that markets are fully priced. What it does suggest is that the future path of the market will be more dependent on the environment than valuations.

Russ Koesterich, CFA, is Portfolio Manager for BlackRock’s Global Allocation team and is a regular contributor to The Blog.

Investing involves risks, including possible loss of principal.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of May 2019 and may change as subsequent conditions vary.

The information and opinions contained in this post are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy.

As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents.

This post may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass.

Reliance upon information in this post is at the sole discretion of the reader. Past performance is no guarantee of future results. Index performance is shown for illustrative purposes only. You cannot invest directly in an index.

©2019 BlackRock, Inc. All rights reserved. BLACKROCK is a registered trademark of BlackRock, Inc., or its subsidiaries in the United States and elsewhere. All other marks are the property of their respective owners.

USRMH0519U-853745-1/1