by Russ Koesterich, CFA, Blackrock

Russ discusses why volatility has not been more severe, even though growth has softened.

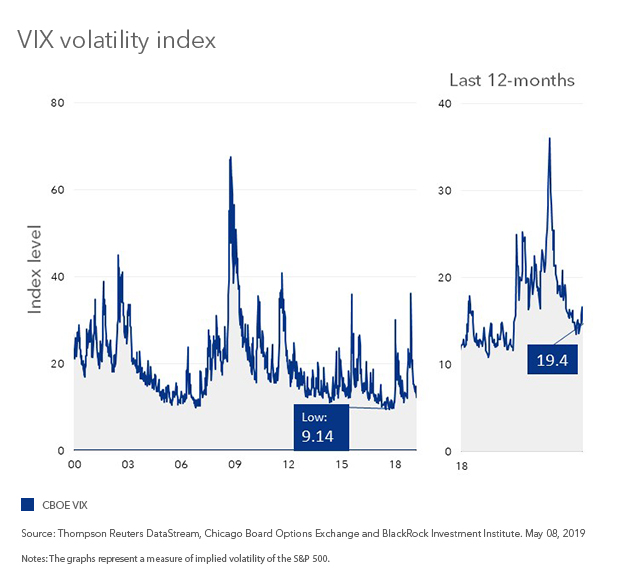

With one Sunday afternoon tweet, President Trump reintroduced what had recently vanished from financial markets: volatility. By Thursday May 9th, the VIX Index, which measures implied volatility on the S&P 500, had reached a four-month high. With a trade deal with China now in doubt, or at least less imminent, investors are reassessing their views on the economy and financial markets.

How much worse can things get?

To answer that, investors should focus on two factors, which are more quantifiable than the day-to-day news flow: expected growth and financial conditions. For now, the latter offers some comfort. While it is true that a complete collapse in trade negotiations would send stocks much lower and volatility much higher, easy financial conditions are one reason the recent pullback has not been more severe. Even at 23 the VIX is well below its December peak and less than half the level it reached in February 2018 (see Chart 1).

A few weeks back I discussed the interplay between financial conditions and the growth outlook. The key message was that financial conditions are central for assessing market volatility. This is even truer when growth is soft, as it is today. Fortunately, while growth is tepid financial conditions are considerably easier than they were late last year.

For example, high yield spreads remain about 25 basis points (bps, or 0.25% points) below the level from late March and 150 bps below the December peak. Long-term interest rates have also pulled back. At 2.45% U.S. 10-year yields are approximately 80 bps below the 2018 peak. Finally, while the dollar has strengthened a bit since, the Dollar Index (DXY) remains within its recent range. The bottom line: Outside of the stock market, most measures of financial conditions have eased. This is why most broad based measures of financial stress look much healthier than a few months ago.

Why is this important?

As I discussed back in April financial conditions ultimately explain the lion’s share of the variation in equity market volatility. In fact, a simple two-factor model, including high yield credit spreads and the St. Louis Financial Stress Indicator, has explained roughly 80% of the variation in the VIX during the past 17 years. What is it suggesting today? Assuming no change in financial conditions, volatility looks too high.

However, even in a post-QE world, financial conditions are not the only driver of markets; growth matters as well. The key risk is that the potential drag from tariffs is occurring at a time when economies outside of the United States are just starting to stabilize. Another disruptive period of trade friction represents a major risk for Europe and China. Should this occur, central banks may have little choice but to ease even more.

Russ Koesterich, CFA, is Portfolio Manager for BlackRock’s Global Allocation team and is a regular contributor to The Blog.