by Doug Kass, Seabreeze Parnters Management

- The Bull Market in complacency has reappeared as the markets (again) disassociate from the real economy.

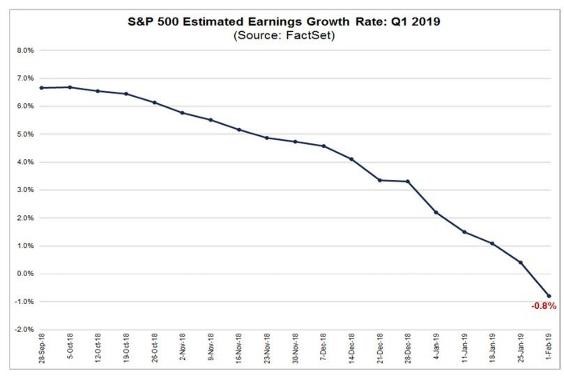

- An earnings recession appears increasingly likely

- (Always) listen to Warren Buffett

“I didn’t come this far to only come this far, so we’ve still got further to go.”- Tom Brady

“You sure that’s the question you want to ask?”- Bill Belichick

Like the dynastic rule of the New England Patriots football team, Mr. Market continued its assault higher yesterday – making it six weeks of consecutive pass completions.

Borrowing from Monday’s column, at the core of my market concerns is the diminished outlook for economic and profit growth in 2019-2020…. and there was nothing in the recent high-frequency data or earnings reports that changes this outlook.

Indeed as noted last week, for every Facebook (FB) there is an Amazon (AMZN) or a DowDuPont (DWDP) with regard to fourth-quarter earnings

With political turmoil continuing and our thesis regarding private — and public-sector debt loads unchanged (its a governor to growth!), the market — much like in previous periods such as January and September, 2018 — has detached itself from the real economy.

One must look to the economic message of the bond market, and with a 10-year yield down to 2.638 this morning, that message is loud and clear. Meanwhile a negative (0.01%) Japanese ten year and a near negative yield on the German 10 year bund (at only sixteen basis points).

As reported in Zero Hedge last last week, 1Q2019 earnings are peaking and are expected to post an annual decline — the first such since 2016:

We have learned that this widening gap between economic and profit reality and fantasy can continue for a while, particularly with the Fed at the market’s side, as the market over the short term is a voting machine.

But, as The Oracle teaches us, in the long run, the markets are a weighing machine.

Bottom Line

- Sellers live lower and buyers live higher

- “Investors should remember that excitement is their enemy.” – Warren Buffett

Warren Buffett famously said that higher stock prices are the enemy of the rational investor.

Price has a way of changing sentiment. (h/t The Divine Ms M) but we should not lose sight that upside reward v. downside risk is a dynamic and quickly changing calculus.

Reward doesn’t get better with higher stock prices, it deteriorates when stocks are advancing. Often, as might be the case, sharp and unrelenting advances lull us into a false sense of security, particularly when global economic growth is so fragile and beginning to show signs of deteriorating (from a rate of change standpoint).

As I mentioned in yesterday’s Bloomberg interview, we are not quite back to the euphoria of late January, 2018 or mid September, 2018 – but we are definitely back into the Bull Market in Complacency.

It can be argued (and I do), that the market has been materially fueled, in no small measure, by the dominance and impact of the machines and algos – that worship at the altar of price momentum. More than ever, our markets have become a one-way trip (up or down) – difficult to navigate (as suggested by all the long/short hedge fund closures in the last 18 months) – and hard to interpret and trade.

As I look into February, we should remind ourselves that February may make us shiver…

And, like the first half of Sunday’s Super Bowl between the Rams and Patriots, the players may fail to make a forward pass in the months ahead.

The movie is now in reverse as the horror story of October- December has become a love story in January. The machines and algos which sold in November/December are buying in January/February, we have made up a significant portion of the post September 2018 losses.

Perhaps, like my pal Tom Lee (and the other Bulls) believe, the S&P may be headed to new highs and the New England Patriots, led by an aging Tom Brady and with coach Bill Belichick going back to his tapes, plots and schemes — are going to win their seventh Super Bowl ring in 2020.

But I doubt it.

Copyright © Doug Kass