by Lance Roberts, Clarity Financial

As we discussed in this past weekend’s missive:

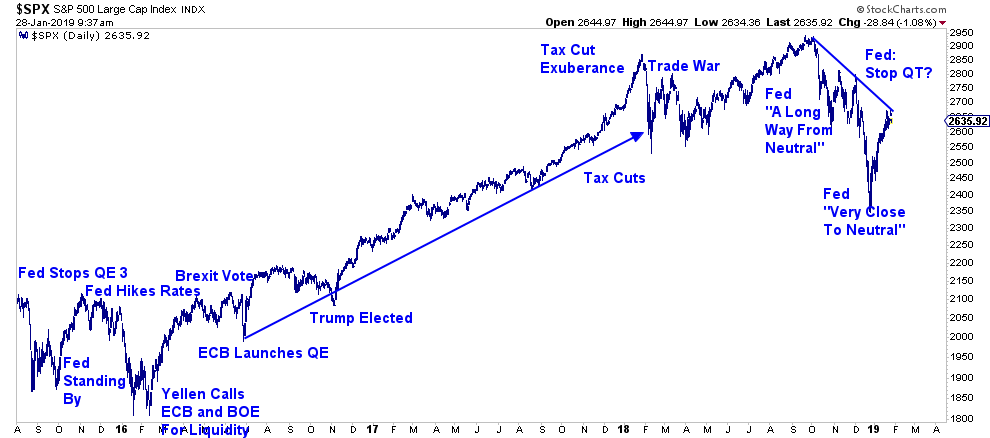

“A WSJ article suggesting that the Fed would not only stop hiking interest rates but also cease the balance sheet reduction which has been extracting liquidity from the market.

In mid-2018, the Federal Reserve was adamant that a strong economy and rising inflationary pressures required tighter monetary conditions. At that time they were discussing additional rate hikes and a continued reduction of their $4 Trillion balance sheet.

All it took was a rough December, pressure from Wall Street’s member banks, and a disgruntled White House to completely flip their thinking.”

This is a change for Jerome Powell, who was believed to be substantially against Fed interventions, shows his worst fear being realized – being held “hostage” by the markets. A look at Fed meeting minutes from 2013 was his recognition of that fear.

“I have one final point, which is to ask, what is the plan if the economy does not cooperate? We are at $4 trillion in expectation now. That is where the balance sheet stops in expectation now. If we have two bad employment reports, the markets are going to move that number way out. We’re headed for $5 trillion, as others have mentioned. And the idea that President Kocherlakota said and Governor Duke echoed— that we ’re now a captive of the market — is somewhat chilling to me.”

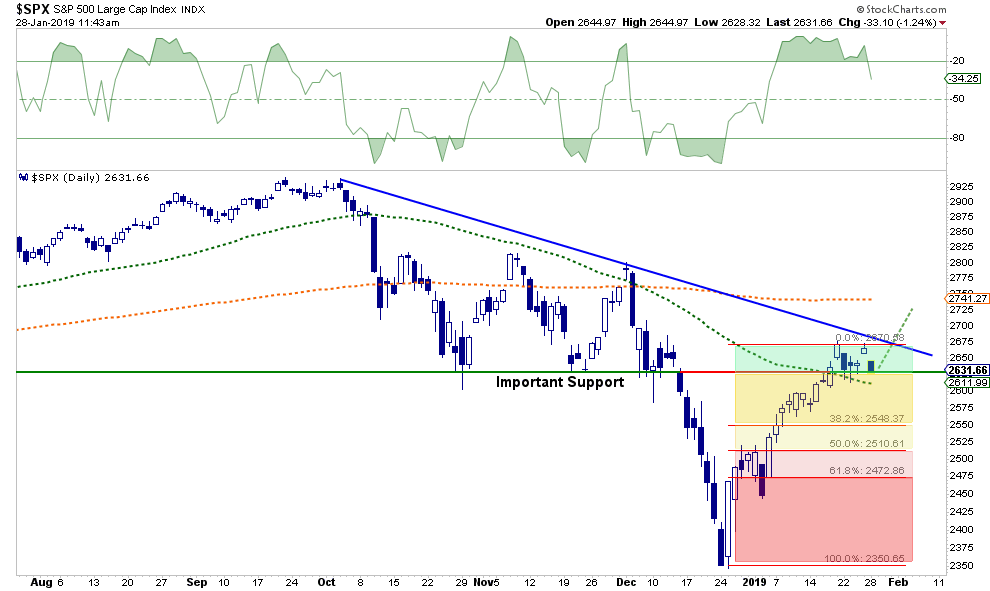

This week, the Fed meets to discuss their next policy moves. If the Fed announces a reduction/elimination of future rate hikes and/or a reduction/elimination of the balance sheet reduction, stocks will likely find a bid.

At least in the short-term.

Longer-term the markets are still dealing with an aging economic growth cycle, weakening rates of earnings growth, and rising political tensions. But from a technical basis, they are also dealing with a break of long-term trend lines and very major “sell” signals.

The problem for the Fed is that while ceasing rate hikes and balance sheet reductions may be a short-term positive, monetary policy is already substantially tighter than it was at the lows. In other words, “stopping” tightening is not the same as “easing.”

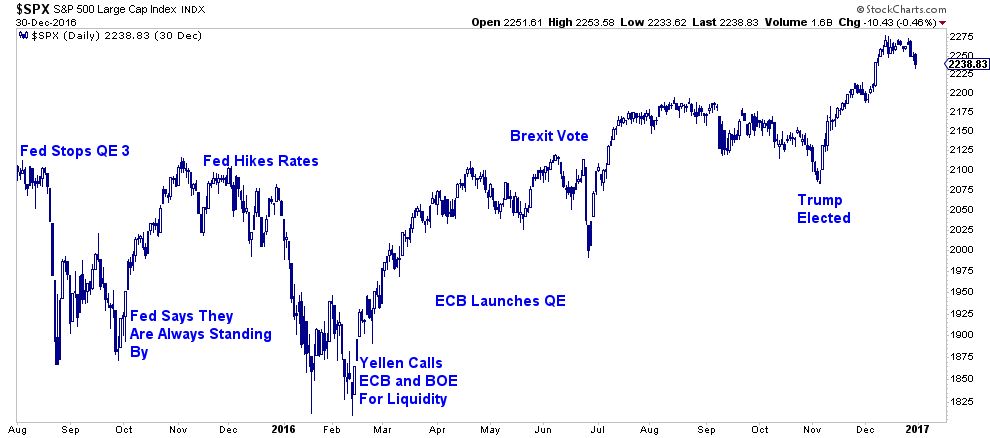

Back To The Future – 2015/2016

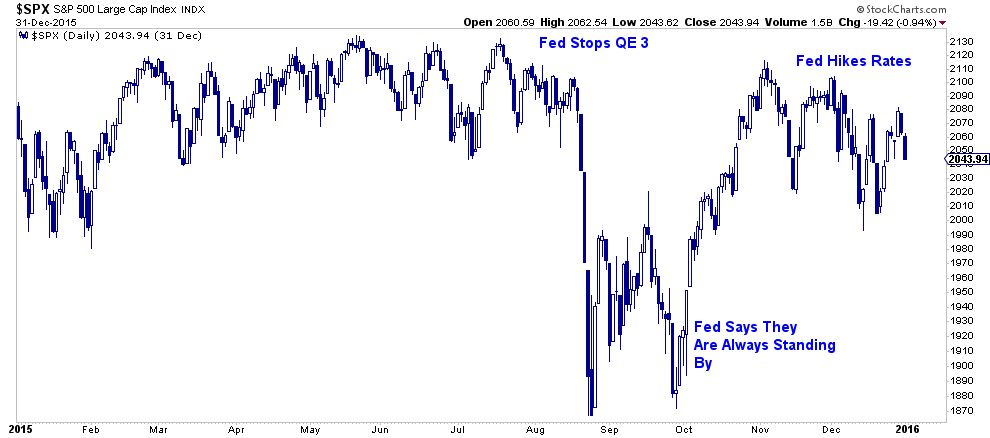

We have seen a similar period previously. During the 2015-2016 correction, the Fed had just announced it’s intent to start hiking rates and had stopped reinvesting liquidity into the markets. (Early tightening.)

The market plunged sharply prompting several Fed Presidents to make announcements reminding markets they still remained extremely “accommodative.”

The market rallied back closing in on previous highs. It certainly looked as if the bulls had regained control of the market. Headlines declared the “correction” was over. But, it wasn’t.

The retest of lows, and setting of new lows, happened over the next 60-days. With concerns over the impact of the upcoming “Brexit” vote, the Fed Chairman Janet Yellen coordinated with global Central Banks to provide liquidity to support global markets in the event of a disorderly “break up.”

In November of that same year, Donald Trump was elected to office with promises of deregulation, tax cuts, and massive infrastructure spending projects which provided an additional boost to equities into the end of the year.

Those promises combined with massive Central Bank stimulus led to one of the longest bull market runs in history with virtually no volatility.

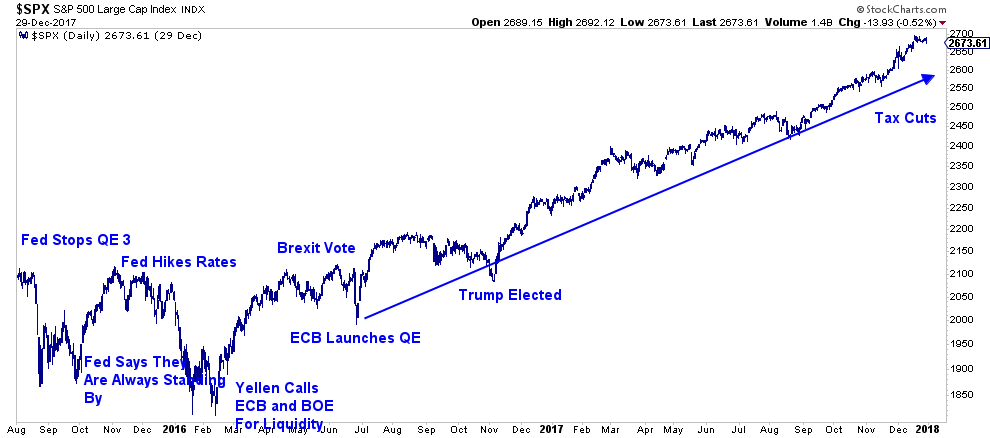

So, here we are today.

The Trump Administration successfully passed tax cut legislation for corporations in December of 2017. Subsequently, stocks surged at the beginning of 2018 as bottom line earnings were expected to explode.

However, that surge also marked the “blow off” top of the rally.

As the Administration launched its “Trade War” with China. Stocks fell in February. However, the markets were able to regain their footing in April as the first look at earnings, post tax-cuts, had soared.

Then came October. The ongoing tariffs on goods being shipped, along with a stronger dollar, began to weigh on corporate outlooks. But it was the Fed, who was in the process of tightening monetary policy, uttered the words that spooked the markets.

“We are still a long-way from the ‘neutral rate.'” – Jerome Powell

Despite evidence of an already slowing economy, and the yield curve almost inverted, the idea the Fed would remain consistent in hiking interest rates and reducing their balance sheet further weighed on investor confidence.

The “Fed Put” was gone.

Market Dependent

Despite commentary from the Fed they were only “data dependent,” all it took was a 20% correction from the highs to change their minds. But not just the Fed’s.

While the WSJ is reporting a change in attitude from the Fed on the reduction of their balance sheet, the White House, which has pinned their measurement of success to stock prices, took prompt action.

The Secretary of the Treasury made announcements assuring the markets of stability and pushing for banks to put liquidity back into the markets. The Trump Administration has repeatedly assured the markets that “trade talks” are going well and “deal” is close to being done.

For now, the markets have bought into the “rhetoric” and have rallied sharply from the lows.

“Mr. Market” clearly has control over both fiscal and monetary policy. “Data dependency” has been relegated to the “dust bin of history.”

So, is the bull back?

Or, is the market, despite all of the support, set to retest lows as seen in early 2016?

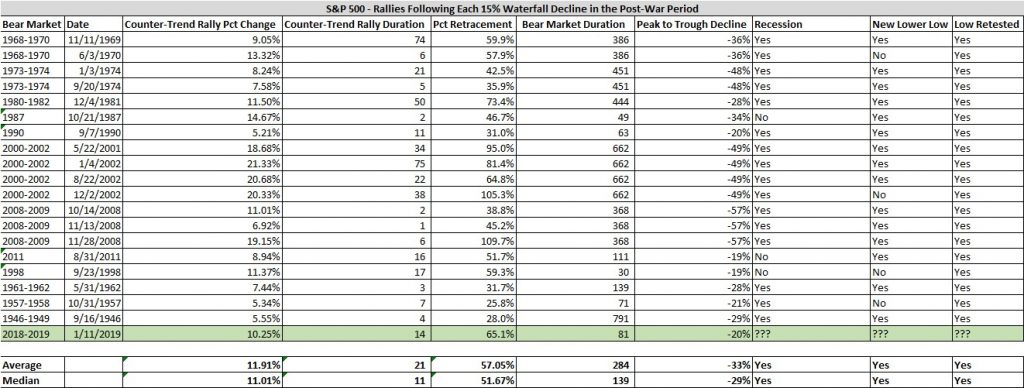

Bryce Coward, CFA recently studied all the previous similar declines:

“We’ve cataloged all 20 uninterrupted 15% declines in the post-war period and documented what has happened afterward, as well as the type of market environment in which those declines have taken place. By uninterrupted decline, we mean a waterfall decline of at least 15% without an intermediate counter-trend rally of at least 5%. Some bullet points describing the rallies following those declines are below:

- The average counter-trend rally following a 15% waterfall decline is 11.9% (11% median) and it takes place over 21 trading days on average (median 11 days).

- The rallies end up retracing 57% of the decline on average (median 52%).

- The average of those bear markets have a peak-to-trough decline of 33% (median 29%)

- The duration of those bear markets is 284 trading days on average (median 139 days)

- In 16 of 19 instances (excluding the decline we just witnessed), a recession was associated with the bear markets.

- Waterfall declines of at least 15% have only taken place in bear markets.

- 100% of the time the low resulting from the waterfall decline was retested, and in 15 of 19 cases a new lower lower was made.”

What do these data say about the current counter-trend rally?

- First, this rally has already retraced 65% of the waterfall decline (greater than average and median) and has lasted about three weeks (less than average but greater than median). This suggests upside from here may be limited in both magnitude and duration.

- Furthermore, these data strongly suggest the major index will retest the Christmas Eve low at the very least and most likely will make a new lower low in the weeks and months ahead.

- While we are not forecasting a recession at this time, waterfall declines of the magnitude just witnessed tend to take place in recessionary market environments, so we need to at least be open to that possibility.

- Finally, waterfall declines typically take place in bear markets lasting an average of 284 days (median 139 days). At just 81 days in duration, these data suggests we have bit further to run before we reach the bear market nadir. That said, there are four instances of waterfall declines taking place in short bear markets, so we don’t place much weight on this particular piece.

While the markets could certainly rally in the weeks ahead, there are significant challenges coming from both weaker economic growth, rising debt levels, and slowing earnings growth.

But most importantly, the biggest challenge in the months, and years, ahead will be the sustainability of the price deviation from long-term trends.

As Dana Lyons penned last week:

“Finally, even stock prices themselves can be considered excessive. In fact, when compared to a regression trend line on the S&P Composite going back to inception in 1871, the index price reached 122% above its long-term trend this past September. Another way of saying that is that the S&P 500 is 122% overbought. In other words, if stock prices were simply to revert to their long-term mean, the S&P 500 would be down closer to 1300 than recent highs near 2900.”

“There are certainly plenty more examples of excess in the stock market. But these few should give you an idea why, if we have entered a longer-term bear market, the oft-derided bears may end up getting the last laugh.”

Yes, this could certainly work out much like 2015-2016 if the Fed throws in the towel to appease the markets.

If they don’t, there are plenty of indications which suggest a more important mean reversion process has already begun.

Copyright © Clarity Financial