by John Lynch Chief Investment Strategist, LPL Financial,

Jeffrey Buchbinder, CFA Equity Strategist, LPL Financial

KEY TAKEAWAYS

• We expect the Fed to pause interest rate hikes this week.

• While the market environment has been challenging, we think recent weakness increases the chances of a positive market response post-tightening cycle.

• Whether the Fed’s rate hike campaign is already over, or will end fairly soon, history indicates that doesn’t suggest a recession is right around the corner.

The Fed will likely pause interest rate hikes at its policy meeting this week. The Federal Reserve (Fed) meets this week, culminating in its rate decision on Wednesday, January 30. We expect the Fed to pause in response to slower global growth, trade tensions, and market volatility, although we believe at least one and possibly two more rate hikes are likely before the end of the cycle. At the same time, we recognize the possibility that the Fed’s December hike may have been its last.

Below, we’ll discuss potential stock market implications if the Fed is done, or nearly done, hiking interest rates. For more of our thoughts on the upcoming Fed meeting, please see this week’s Weekly Economic Commentary.

WILL THE FED PAUSE?

Financial markets and the Fed were at odds through the end of last year. U.S. stocks’ sharp decline during the fourth quarter was driven in large part by the disconnect between the Fed’s and the market’s economic outlooks. Fed Chair Jerome Powell spooked markets in October by communicating that the Fed was a long way from a neutral rate, which the markets interpreted to mean several more hikes were yet to come. However, Powell has since adjusted his narrative.

The latest commentary from Powell and other Fed officials has emphasized the central bank’s flexibility, data dependency, and increasing willingness to factor financial market volatility and overseas developments into rate decisions. Just the message the market wanted to hear, and a nod to the growing possibility that the Fed may pause its gradual rate hikes.

The Fed’s shrinking balance sheet has also been of concern to market participants looking for a pause in tightening. Though different from a rate hike, borrowing costs can rise when bonds that the Fed purchased through its quantitative easing program mature and proceeds are not reinvested (referred to as balance sheet runoff or unwind, or quantitative tightening).

Here, the change in the Fed’s message, from a balance sheet “normalization” on autopilot to one that is more flexible, has helped market sentiment and increased speculation around the Fed’s short-term policy plans. Friday’s Wall Street Journal report that the Fed was considering slowing its balance sheet runoff and holding more Treasuries for longer was another positive sign for the doves.

Markets have increasingly positioned for a pause. Fed funds futures are now pricing in about a 70% probability that rates remain unchanged throughout 2019. So where does that leave us? While we think another hike this year is likely (possibly two), the Fed’s soft exit from accommodative policy is on the horizon.

HOW MIGHT STOCKS REACT?

The Fed’s current tightening cycle is slightly more than three years old. So how might stocks react to a long-term pause? With the help of research provider Ned Davis Research (NDR), we can see that stocks have generally responded favorably. NDR defined a pause as at least five months between rate hikes within a rate hike cycle.

They found that in six such occurrences since 1963, stocks have been up an average of 1% in the three and six months after pauses. The 6% gain in the S&P 500 Index since the Fed’s rate hike on December 19 would be by far the best post-pause performance if the gains hold and the next hike is at least five months away.

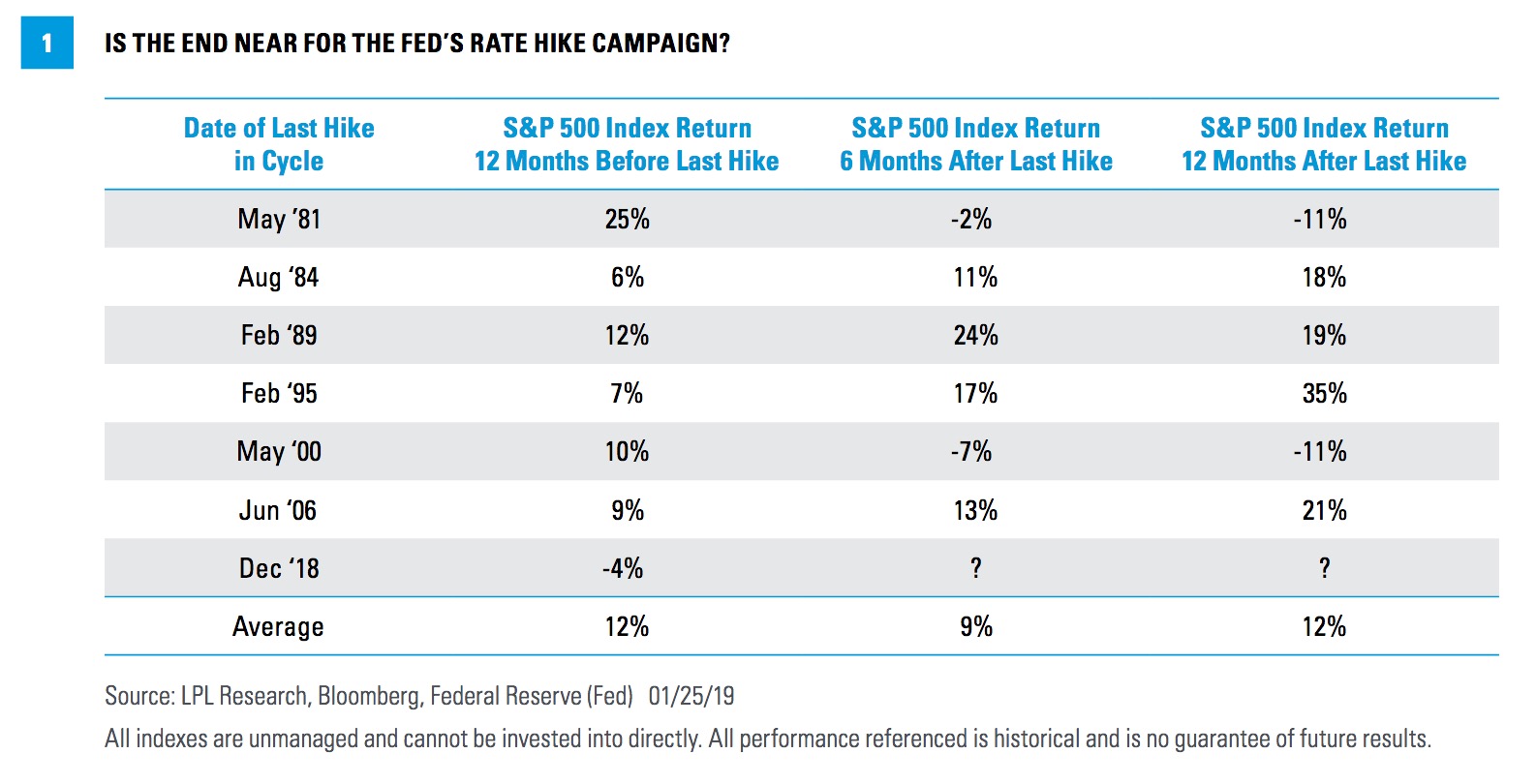

Regardless of what the Fed does this week, we recognize the possibility that they may be finished or nearly so, so we looked at what stocks have done around the end of Fed rate hike campaigns. Not surprisingly, we found that stocks tend to react positively [Figure 1]. Looking at the 6 and 12 months following the final hike in the last seven rate hike cycles, the S&P 500 has risen by an average of 9% and 12%.

Stocks have historically fared well in the 12 months leading up to the last hike. However, the S&P 500 fell 4% during the 12 months ending December 19. While the market environment has been challenging, we think recent weakness increases the chances of a positive market response post-tightening cycle.

Recent stock gains suggest that investors probably recognized rate hike fears were overdone. Though we don’t think the Fed is done, that scenario is worth considering given the market is pricing it in.

If the Fed’s last hike comes this year, which we see as likely, that doesn’t necessarily mean a U.S. recession is near. Every cycle is different, but over the past 40 years, the average time from the last hike to recession has been nearly three years. In 1984 and 1995, it was over six years. Bottom line, we think recession within the next year or two is unlikely.

CONCLUSION

The Fed will likely pause this week and stocks are likely to respond favorably as a result. Whether the Fed’s rate hike campaign is already over, or will end fairly soon, history indicates that doesn’t suggest a recession is right around the corner.

We are encouraged by the latest stock market rebound off the December 24, 2018, lows and see more solid gains ahead in 2019, driven by steady U.S. economic growth, the ongoing effects of fiscal stimulus, mid-to-high-single digit earnings gains, and a potential (we think likely) U.S.-China trade agreement. Our year end fair value target for the S&P 500 is 3000.

*****

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results.

The economic forecasts set forth in the presentation may not develop as predicted. Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk in all market environments.

All indexes are unmanaged and cannot be invested into directly. Unmanaged index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investment.

All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

INDEX DESCRIPTIONS

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

RES 70854 0119 | For Public Use | Tracking #1-816029 (Exp. 01/20)

Not FDIC or NCUA/NCUSIF Insured | No Bank or Credit Union Guarantee | May Lose Value | Not Guaranteed by Any Government Agency | Not a Bank/Credit Union Deposit This research material has been prepared by LPL Financial LLC. To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial LLC is not an affiliate of and makes no representation with respect to such entity.