by Richard Turnill, Global Chief Investment Strategist, Blackrock

We see compelling relative value in the BBB segment of the European credit market. Richard explains.

European corporate bonds sold off late last year amid a broad risk-off environment. Most risk assets have recovered since. One of the surprising exceptions: BBB-rated European debt. We now see compelling relative value in this segment of the European credit market, though we maintain our neutral view of the asset class overall.

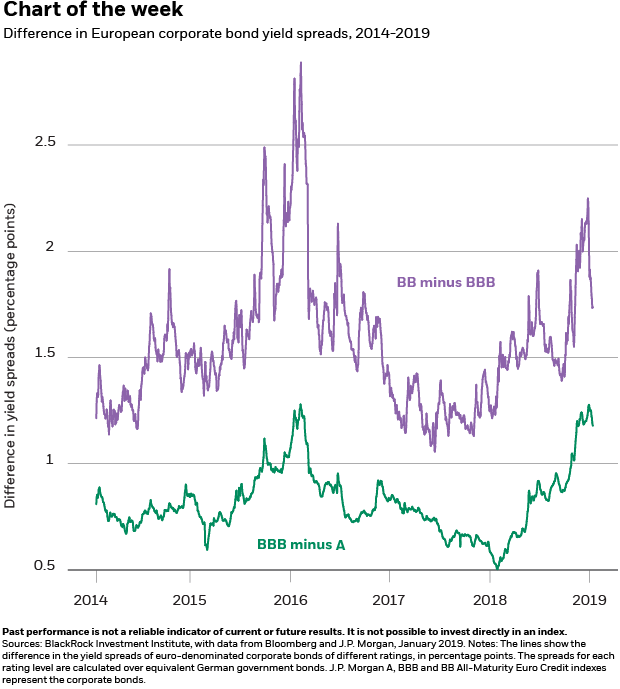

BBB-rated bonds represent the bottom rung in investment grade (IG), so they typically suffer more than their higher-rated IG counterparts during broad market selloffs, and recover more quickly when markets rise. BBBs saw strong outflows into year-end 2018, driving yields higher – yet they have lagged the 2019 recovery in risk assets.

The bottom line in the chart above illustrates the disconnect: The difference in spreads between BBBs and A-rated euro corporates (one rung higher on the ratings scale) has held steady around the wide levels seen at year-end – rather than tightening as it typically does during risk-on periods. At the same time, sub-investment grade bonds with a BB-rating (the top rung of high yield) have outperformed higher-quality BBB bonds, with the difference between their spreads dropping. See the top line in the chart.

A positive global backdrop

Concerns about slowing global growth fueled the December selloff in risk assets, with fears about the European Central Bank’s (ECB’s) asset purchase wind-down an additional weight on euro credit. The ECB is on track to buy only around 2% of European IG corporate issues this year, we estimate, down from 15% last year.

We attribute the BBB cohort’s lagging recovery partly to a surge in BBB issuance by euro-area financials looking to strengthen their balance sheets, rather than worries about ratings downgrades. The elevated issuance may be here to stay, but we see more room for the broad European corporate market, including BBBs, to recover.

Fears about a 2019 recession appear overblown (see our 2019 Global investment outlook). We see global growth slowing, not enough to end the expansion but enough to keep major central banks on hold. Euro-zone growth should stabilize at low levels in 2019, helped by extra-easy ECB policy, fresh fiscal stimulus and the lifting of one-offs such as regulation-related disruptions to the auto industry.

The ECB maintained its policy last week, as we expected. We agree with its assessment that growth risks have shifted to the downside. This makes ECB growth and inflation estimates seem optimistic, we believe, and a 2019 rate rise unlikely. We see the U.S. Fed on hold until at least September (see our recent Macro and market perspectives). This all makes for a positive global backdrop for credit.

Read more market insights in our weekly commentary.

Medium-term threats to European unity, the European economy’s still-anemic growth and its dependence on trade do make us cautious toward European risk assets. We generally prefer U.S. fixed income over European bonds given the Fed has already tightened policy. Yet we see BBB-rated euro corporate bonds as an opportunity for currency-hedged U.S.-dollar-based investors and euro-based investors alike.

The key risk: a re-emergence of risk-off sentiment and related outflows associated with recession concerns and geopolitical tensions. We would need to become more optimistic on the euro-zone growth outlook or the potential for resolutions to political issues–including Brexit–to turn more positive toward European credit overall. Elsewhere in European fixed income, we are underweight European sovereigns, as we expect rates to gradually rise over the medium term from their current abnormally low levels.

Richard Turnill is BlackRock’s global chief investment strategist. He is a regular contributor to The Blog.