by Equities, AllianceBernstein

Value stocks have underperformed for years. But things may be changing. Cheaper stocks have shown signs of awakening recently, and several market forces could tip the scales in favor of value after a prolonged growth surge.

It’s been a tough decade for investors who focus on attractively valued stocks with unappreciated recovery potential. Global value stocks have underperformed growth stocks for most of the past decade. In the last two years, this trend has been fueled by the rising popularity of the high-growth FAANG stocks (Facebook, Amazon, Apple, Netflix and Google) in the US.

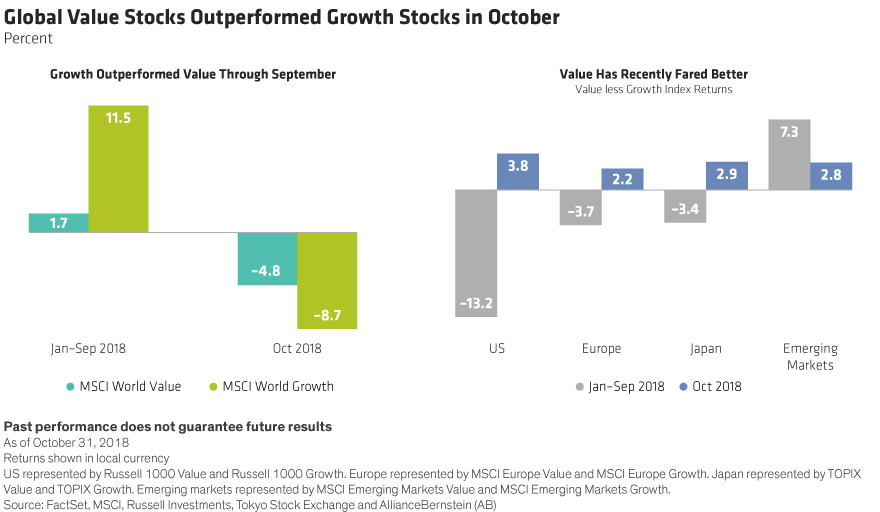

Shift Appears in Third Quarter

But signs of life for value have recently appeared. In the third quarter, value stocks in emerging markets beat growth stocks by 8.8%, while value stocks in Japan also outperformed. And as stocks fell sharply in October, the MSCI World Value Index declined by 4.8%, outperforming the MSCI World Index by nearly 4% (Display, left). Value stocks also outperformed growth stocks in October across regions (Display, right).

It’s too soon to say whether the recent trend is the start of a bigger shift back toward value. But there are some good reasons to believe that value’s long, dark winter may be coming to an end.

1. Rising rates are usually good for value—When interest rates rise, valuations of growth stocks tend to decline more than those of value stocks. It’s simple math: a rising interest rate pushes up the discount rate that investors apply to future cash flows. That can hurt growth stocks, which derive most of their value from long-term profit growth but may not generate much cash today. In contrast, value stocks typically have lower long-term growth but stronger short-term cash flows, meaning that a higher discount rate typically has a lower impact on their valuation. So with US interest rates rising from historic lows, the table may be set for a real value rebound.

2. Earnings and valuations are out of synch—By definition, the earnings growth of value stocks tends to be lower than that of growth stocks. As a result, value stocks typically trade at a discount to growth stocks. Lately, value stocks trade at a 35% discount to growth stocks globally on a price/forward earnings basis. That’s a much deeper discount than usual, especially as the difference in forecast earnings growth between value and growth stocks is around its long-term average. If you believe that earnings matter for stock valuations, this discount appears unjustified. When it corrects, we believe value stocks will post strong performance.

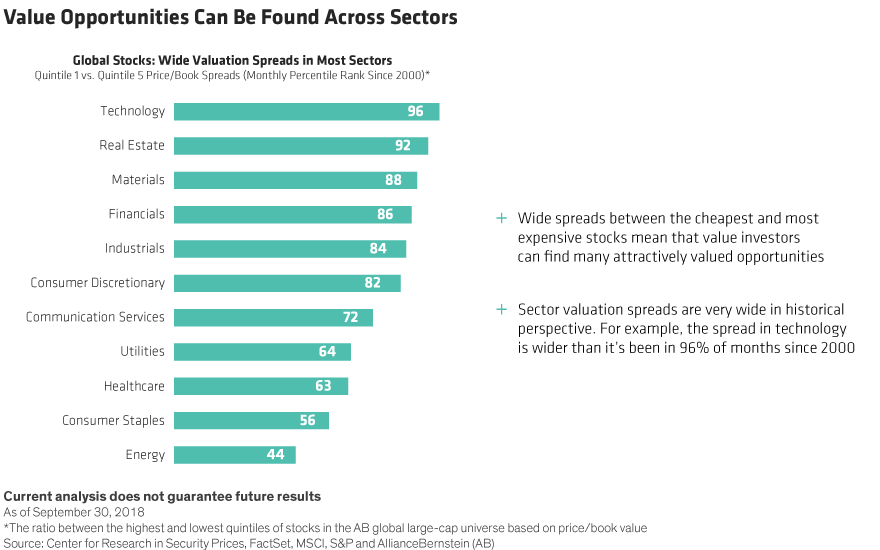

3. Sector opportunity is widespread—Some sectors tend to do better when rates rise. In financials, for example, banks typically benefit from rising interest-rate margins, and insurers enjoy lower costs to match their liabilities. But beyond these sectors, we’re finding underappreciated stocks today in diverse sectors from consumer discretionary to technology to materials. Spreads between the cheapest and most expensive stocks within sectors are unusually wide (Display). This means investors don’t have to rely on big sector positions to capture the opportunity.

Challenging Markets Favor Value Stocks

Recent market turbulence has rattled investor confidence in equities. Yet we think value investors should embrace the volatility—especially as corporate profits remain relatively solid. Even though earnings growth is expected to decline in some markets next year—notably in the US—profits remain robust around the world. And while the market declines have been painful, stocks are now much cheaper than they were at their late January peaks—even in the US.

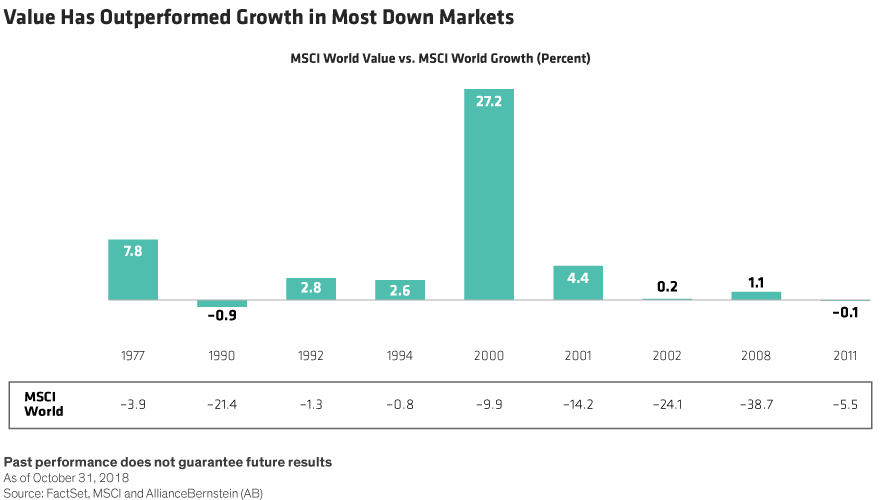

Value stocks have also performed much better than growth stocks through most difficult markets in the past (Display). That’s because when markets correct, stocks that have risen the most tend to fall furthest. For example, since the MSCI created the value and growth style indices in 1975, the broad market has fallen in nine calendar years. Value stocks outperformed growth stocks in seven of those years. In 2000, when the dot-com bubble burst, value outperformed growth by 27%.

In fact, value stocks—which are often seen as risky—could actually help protect investors from volatility today. That’s because with cash-flow yields so high today, cheap stocks of companies that generate ample cash have a helpful buffer against further steep falls in valuation.

Volatility creates opportunities for value investors, too. When markets are falling, stocks of strong companies also get hit. Investors who swim against the tide to buy cheap stocks with solid and underappreciated businesses can take contrarian positions to capture powerful returns in a potential value equities recovery.

Source: Center for Research in Security Prices, FactSet, MSCI, Russell Investments, Tokyo Stock Exchange and AllianceBernstein (AB)

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.

AllianceBernstein Limited is authorised and regulated by the Financial Conduct Authority in the United Kingdom.

Copyright © AllianceBernstein