by Research Team, Purpose Investments

“Alternatives” is a name given to a very wide range of assets. However, at the broadest level, they encompass any investments outside the realm of traditional asset classes such as cash, equities, and fixed income (see Appendix for some of the more common definitions).

Investors use alternative assets for a variety of reasons, including diversification and risk-management. Whatever the reasons for adding these asset classes to a portfolio, use of these assets is increasing and will likely continue to grow in the years ahead.

This primer aims to provide a basic overview of why alternative assets continue to gain traction and simple ways to incorporate alternatives into an investment portfolio.

Why alternatives?

Investors use alternative assets for various reasons. They’re uncorrelated to most other asset classes, and so provide excellent diversification and risk-management benefits. Depending on the asset type, they can also provide everything from protection against inflation, rising interest rates, or market volatility to higher yields or returns. Whatever the reasons for adding these asset classes to a portfolio, use of them is growing.

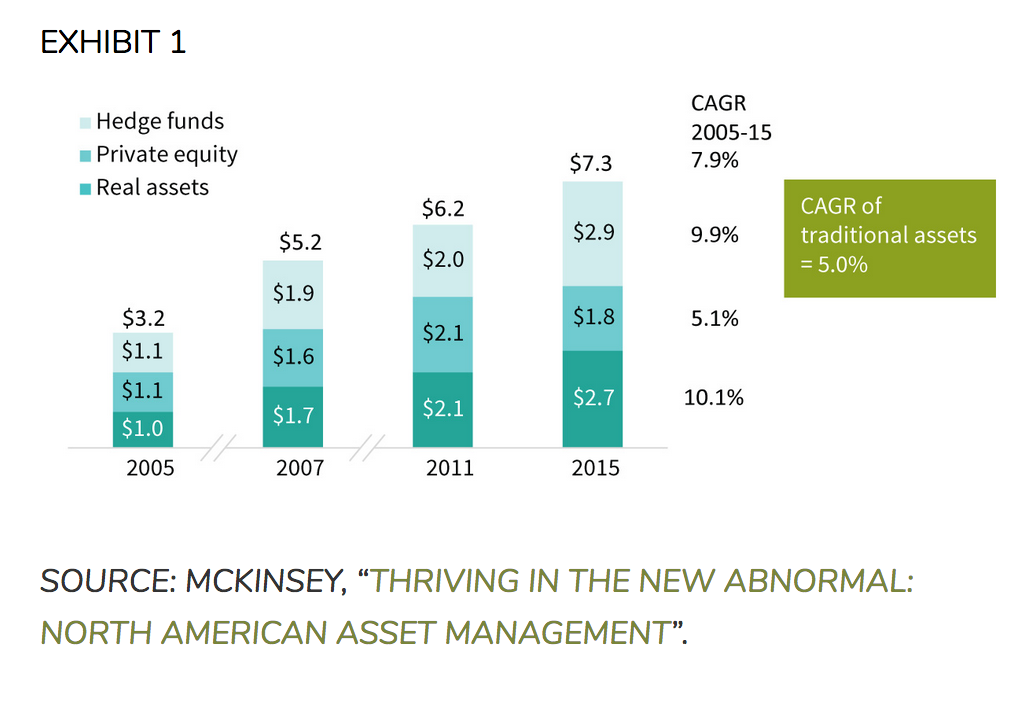

In fact, a study by McKinsey1 suggests that globally, the compound annual growth rate of key alternative asset classes – including real assets, private equity and hedge funds – outstripped that of traditional assets by 2.9% between 2005 and 2015.

The need to increase portfolio diversification

Diversification is important for maintaining a well-constructed, resilient portfolio. One way to do this is to ensure the different portfolio components or asset classes have uncorrelated return streams (i.e., their values move in different directions through the market cycle, so portfolio returns don’t all move up or down at the same time). This smooths out overall portfolio returns and provides for a less volatile investment experience.

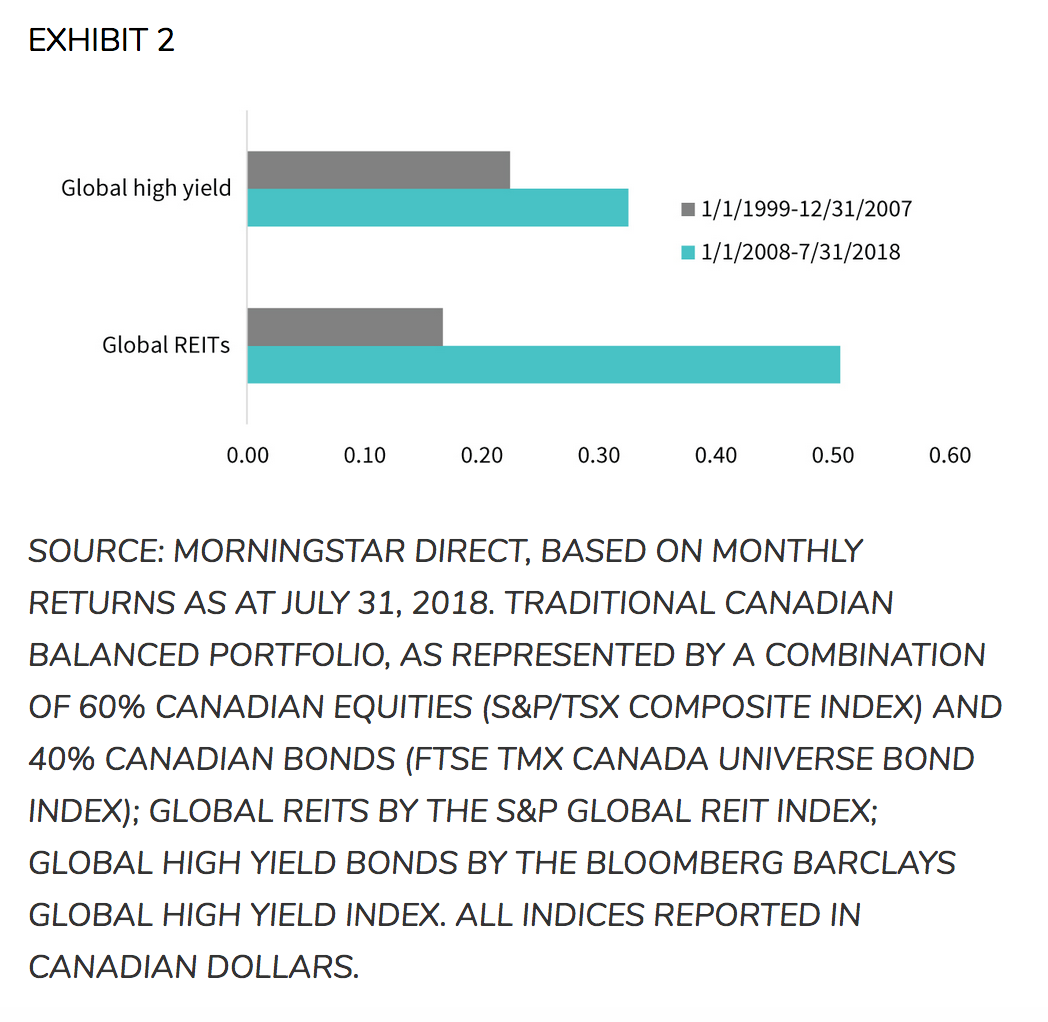

In decades past, asset classes such as REITs and high-yield bonds provided uncorrelated sources of return to a typical Canadian balanced portfolio2. However, since the financial crisis, these correlations have risen (Exhibit 2).

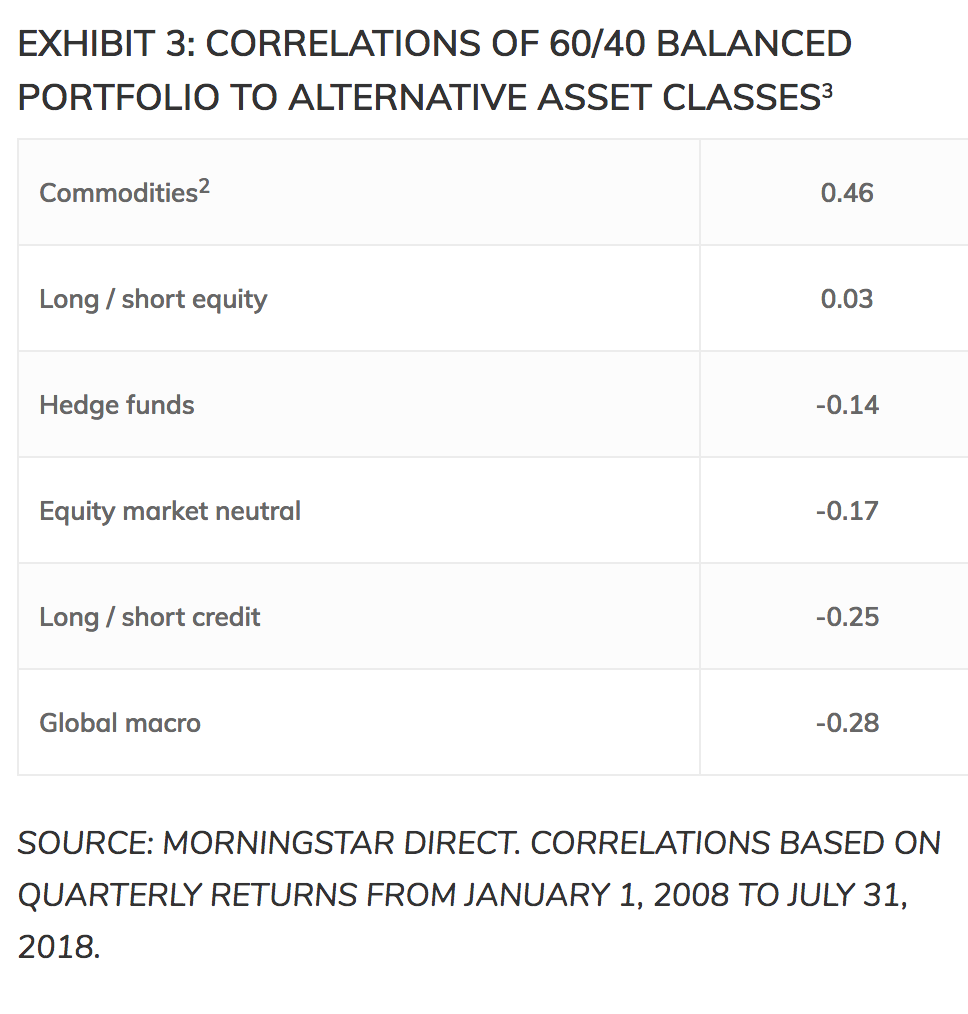

What we now consider alternative asset classes, meanwhile, still provide low or even negative correlations to the same Canadian balanced portfolio (Exhibit 3). During the height of the financial crisis in 2008, many of them actually saw lower maximum drawdowns (Exhibit 4).

Valuations are stretched

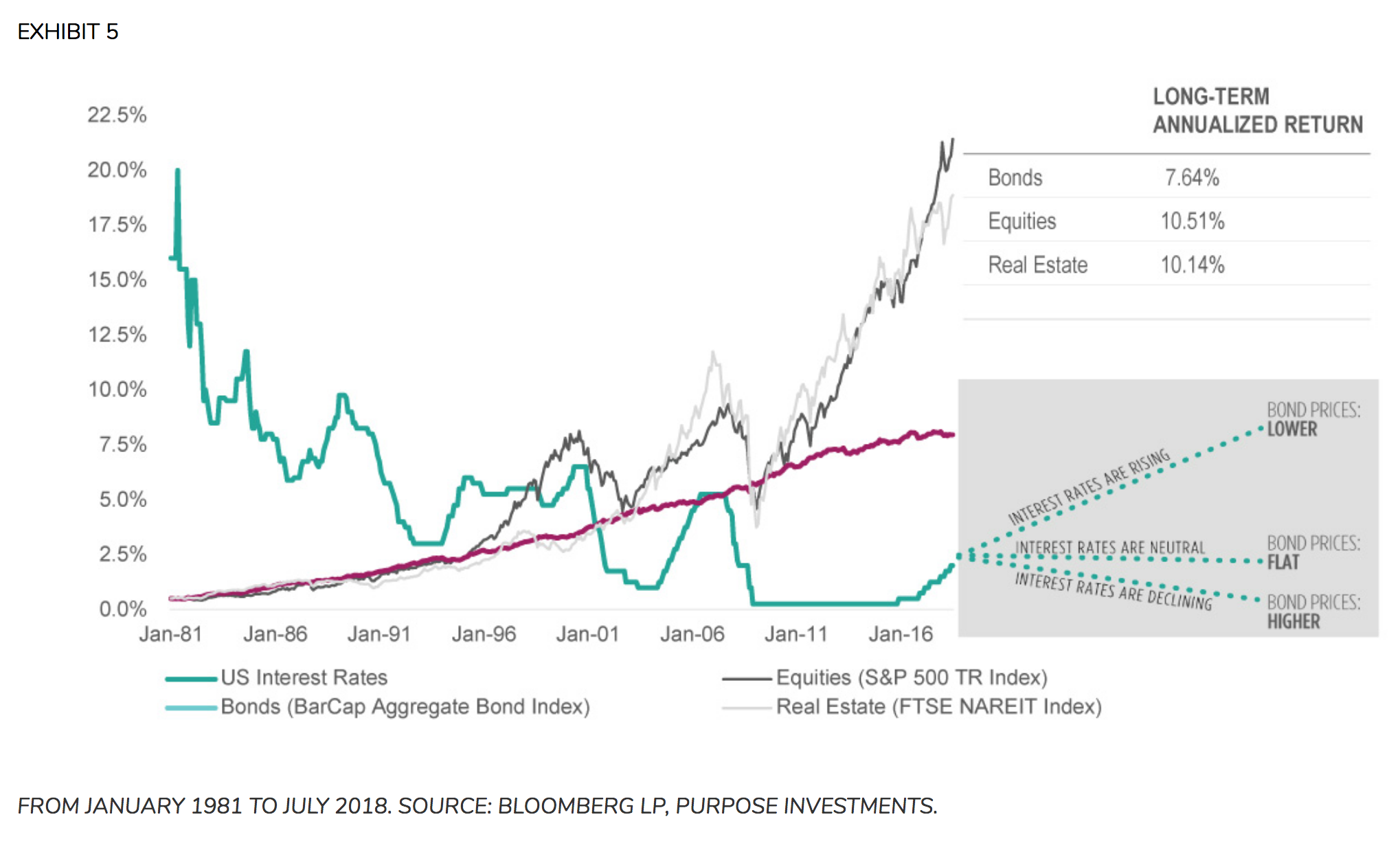

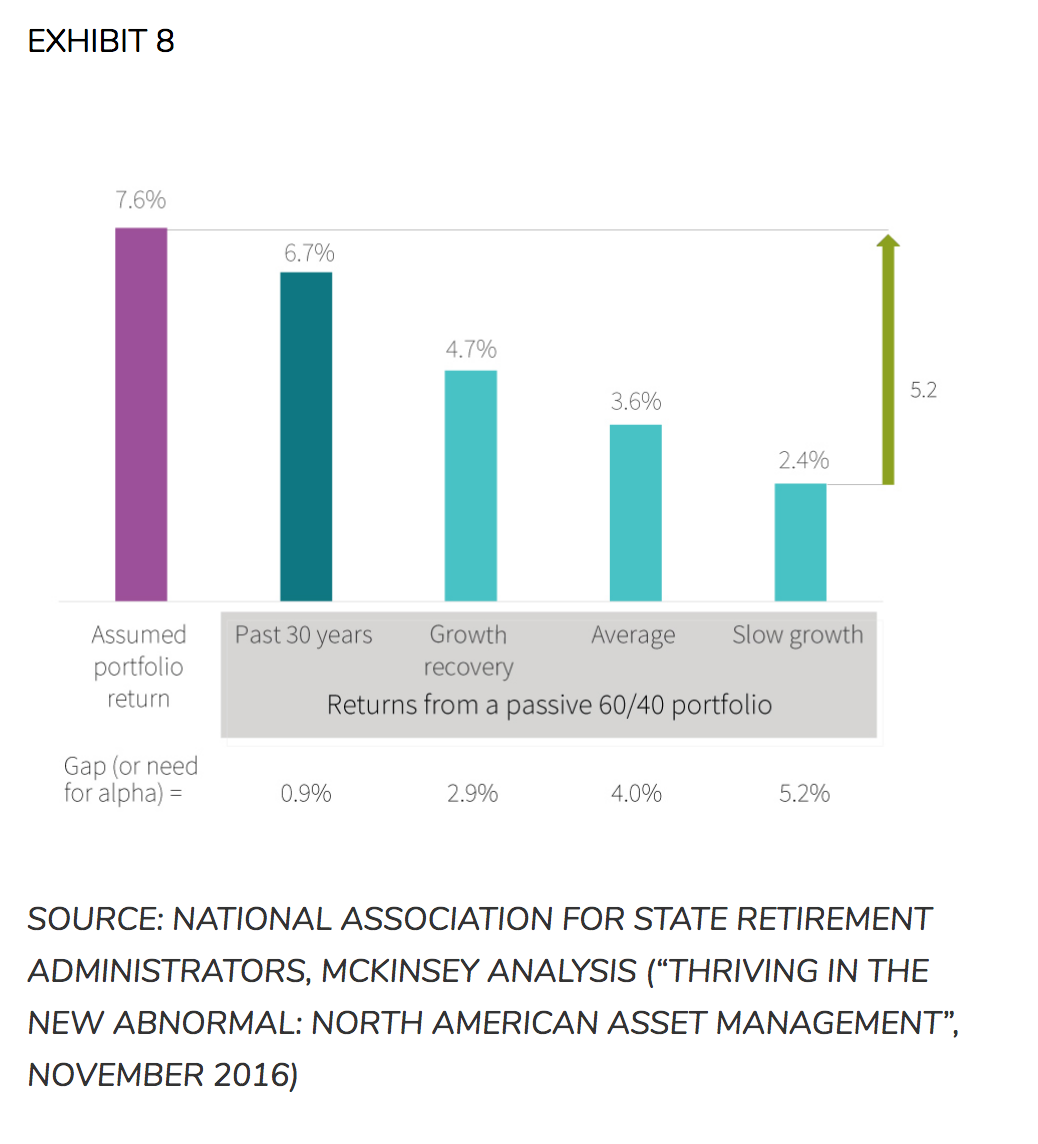

While bonds continue to have low correlation to stocks4, this may not provide investors with much comfort in the years ahead. The unprecedented interest-rate declines across the globe that have been such a tailwind for investors over the past 30-plus years have pushed both equities and fixed-income securities to historically high valuations. A new era of flat-to-rising interest rates could mean we won’t see the same strong performance we’ve come to expect.

Research from McKinsey examining US public pension funds supports this view. Going forward, it estimates the gap between the 60/40 portfolio return expectations and reality is as much as 5.2% (Exhibit 8), depending on the economic environment ahead. Depending on the asset class, alternatives may provide another source of diversified returns and/or yields.

Volatility is expected to rise

In the years since the financial crisis, equity volatility5 has trended lower, and even reached all-time lows in November 2017. Dampening of volatility is widely considered to be one of the consequences of quantitative easing (QE). As a result, the bond-buying and ultra-low rates that central banks put in place to deal with the financial crisis have driven investors searching for yield into riskier assets. In addition, investors have come to expect that central banks will step in with more QE whenever the economy appears likely to hit another roadblock.

Central banks, though, have started to reverse course. This is worrisome, as many investors may find they’re ill-prepared for a macro event that returns volatility to long-term average levels. Case in point: the last time markets saw this level of complacency was in 2007. In addition, hawkish central bankers may prompt more significant selloffs in bonds, pressuring fixed-income holdings. The bottom line is that there will be fewer places to hide.

Going forward, most investors will need to diversify beyond stocks and bonds to manage risk, increase yields, lower portfolio volatility, and ultimately, reach their long-term financial goals.

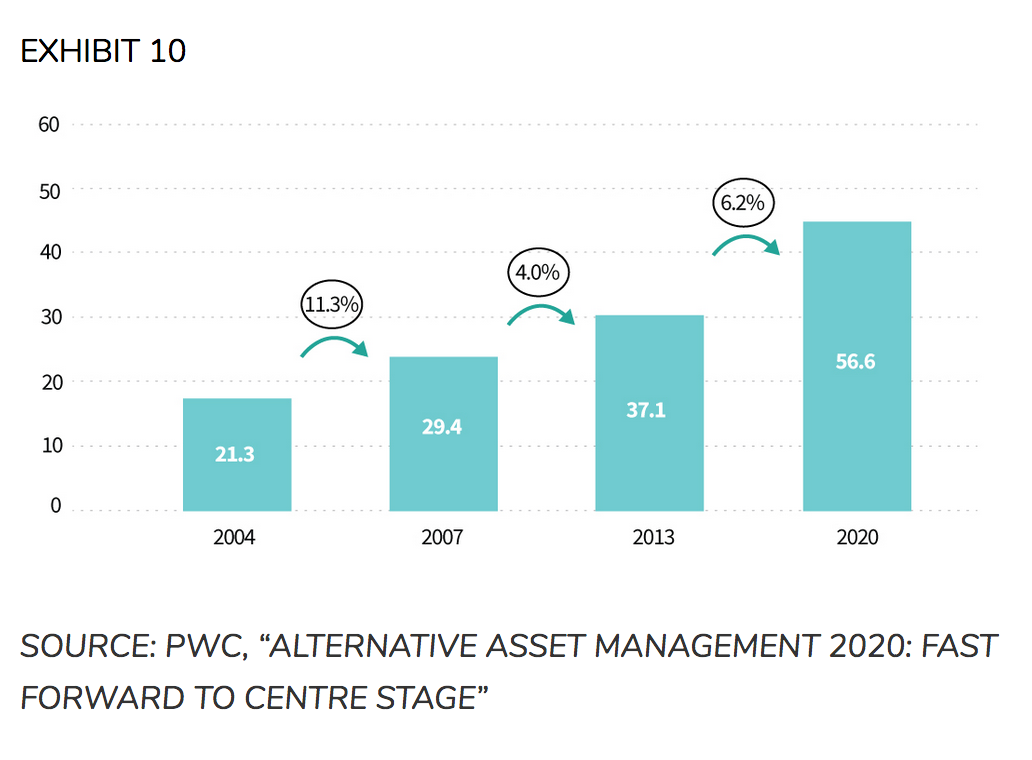

Allocation by “smart money” to alternatives

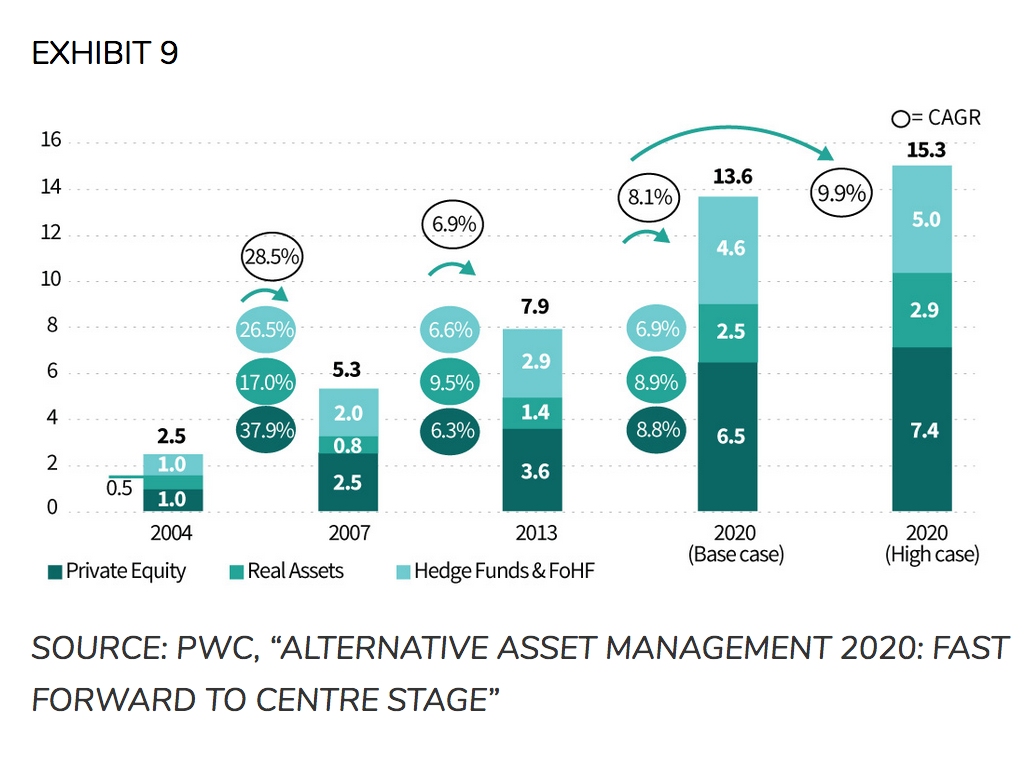

Faced with long-term liabilities, sophisticated institutional investors such as sovereign and public pension funds have recognized the need to further diversify. They’ve responded by adding alternative assets to their portfolio mix over the past decade. In fact, PwC estimates global allocation to private equity, real assets and hedge funds will grow to US$13.6 trillion to US$15.3 trillion by 2020. Based on PwC’s estimated growth of pension fund assets to US$56.6 trillion by 2020, this translates into 24% to 27% allocation to alternative assets.

Adding alternatives to your portfolio

When markets turn volatile, investors are cautioned to focus on a long-term strategy and ignore the ups and downs. This is always good advice, but diversifying beyond the traditional balanced portfolio with alternative investment strategies is also important.

We look at alternatives as generally falling into two buckets: alternative strategies and alternative diversifiers. Both are important and have a place in a properly risk-managed portfolio. However, they each figure differently in the portfolio construction process.

Alternative strategies

Alternative strategies involve thinking about and using traditional asset classes such as bonds and equities in different ways.

Bonds

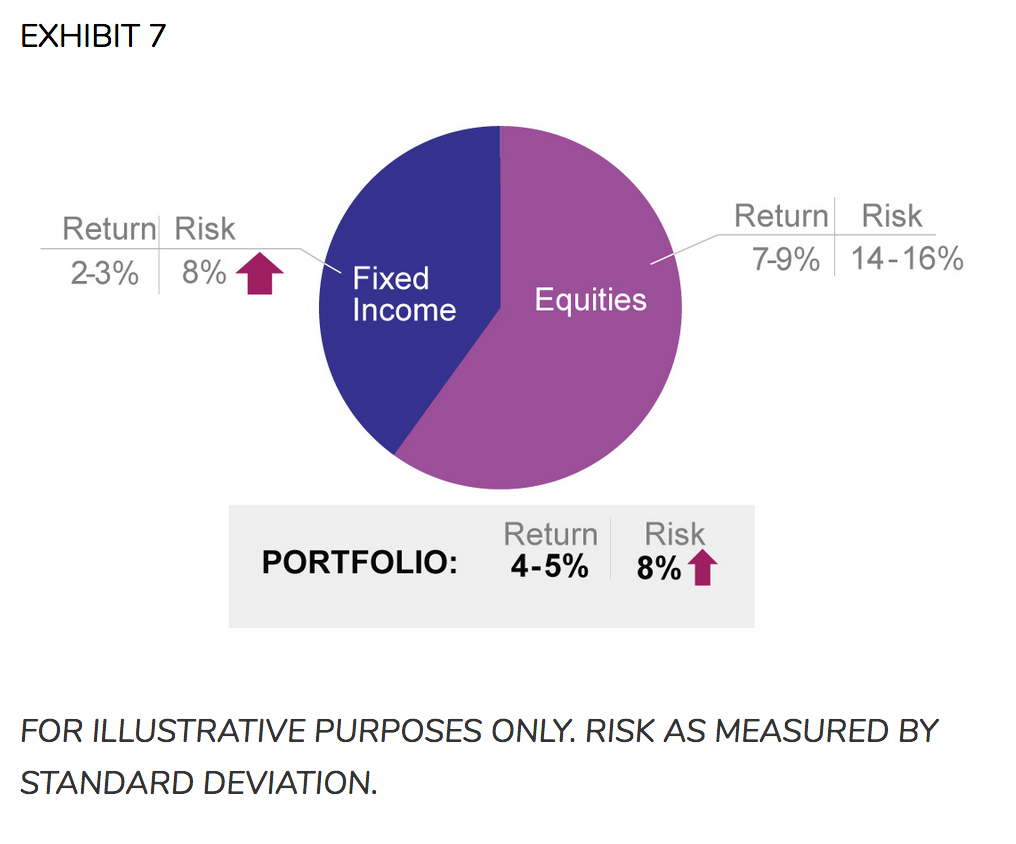

After the precipitous decline in interest rates over the past 30-plus years, a flat-to-rising-rate environment will not be very supportive for fixed-income returns. Going forward, bonds may generate an average of 2% to 4% annually. However, what’s more concerning is that the historical 1:1 risk-to-return ratio for the asset class is likely to rise.

Consequently, the real job of alternative strategies for fixed income is going to be managing risk. This can be done by adding investment funds and other products to your portfolio that employ interest rate hedges to lower duration, help preserve capital and reduce the risk-return ratio.

Equities

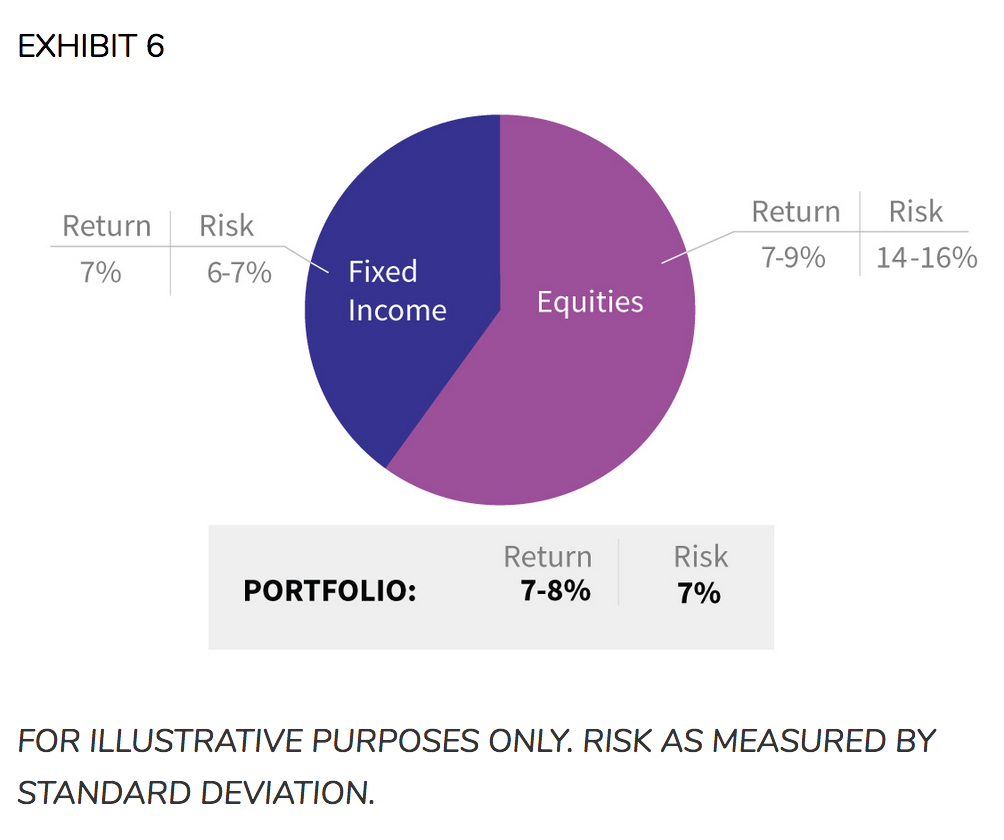

Going forward, a higher allocation to equities than the conventional 60%6 is likely going to be necessary, because a 40% weighting in an asset class that yields 2%-4% won’t be enough for investors to reach their long-term financial goals. However, a higher allocation to equities will inevitably increase portfolio risk, due to the higher volatility generally associated with stocks.

Managing risk at the equity level can be achieved not just through sector and geographical diversification, but also through an intelligent equity risk-management strategy. For example, the majority of a portfolio may be invested in long equity positions, but some market beta7 and risk can be tactically hedged out by taking short positions in broad market indices. This type of long/short strategy helps not only to diversify the portfolio, but also to prevent a 1:1 beta to the ups and downs of equity markets.

Investors may also manage risk by diversifying the sources of volatility, such as through options strategies. Mining volatility over the last 10 years has been an attractive alternative investment strategy, providing moderate diversification and low correlation to long-only equity portfolios. As a replacement for some long equity positions, options strategies can provide similar returns with lower volatility. They can also be used as a high-income alternative to lower-yielding fixed-income assets.

Alternative diversifiers

Diversifiers may include infrastructure, real estate, commodities, currencies, private equity and debt, venture capital, and more (see Appendix for more details). It may also include adding certain hedge fund strategies that are going to provide a different outcome and return stream than traditional equities or bonds. This will serve to diversify the entire portfolio.

When alternative strategies and diversifiers are used together, investors can achieve enhanced portfolio returns with lower associated volatility than a traditional 60/40 portfolio alone.

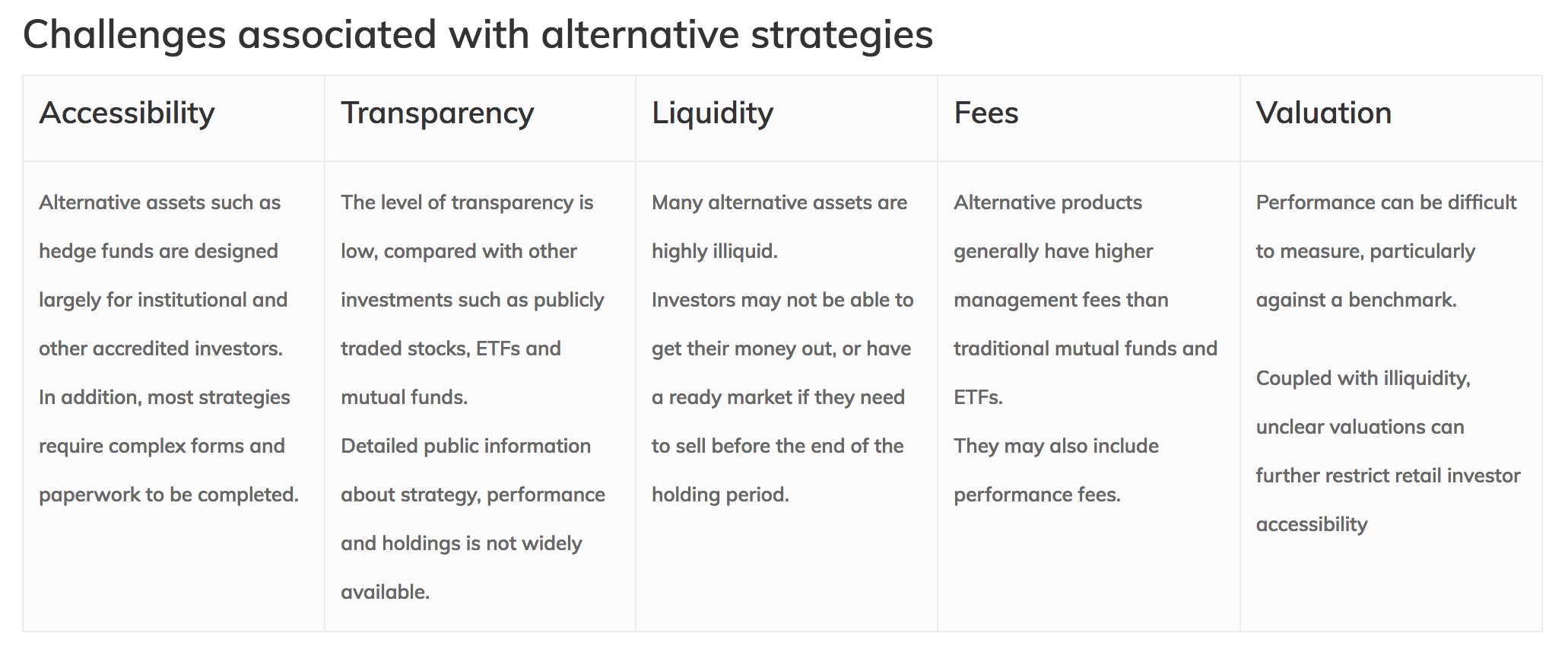

Alternative assets such as hedge funds are designed largely for institutional and other accredited investors.In addition, most strategies require complex forms and paperwork to be completed.The level of transparency is low, compared with other investments such as publicly traded stocks, ETFs and mutual funds.Detailed public information about strategy, performance and holdings is not widely available.Many alternative assets are highly illiquid.Investors may not be able to get their money out, or have a ready market if they need to sell before the end of the holding period.Alternative products generally have higher management fees than traditional mutual funds and ETFs.They may also include performance fees.

Performance can be difficult to measure, particularly against a benchmark.

Coupled with illiquidity, unclear valuations can further restrict retail investor accessibility

Appendix—alternative asset definitions

While not an exhaustive list, the following are some of the more common types of alternative investments.

Real estate and infrastructure

Historically, alternatives have included asset classes such as real estate and infrastructure. This is still true in the case of direct investment in commercial or residential real estate, or physical infrastructure assets such as toll roads or airports. However, publicly traded REITs and infrastructure companies – and specialty funds that invest in them – have grown substantially in popularity, providing broad, liquid access. For this reason, these assets are largely considered to be mainstream equity – and don’t necessarily provide an uncorrelated source of return to a traditional stock and bond portfolio.

Options

Options are contracts that allow an investor to buy or sell an underlying security – often a stock or ETF, but can alsoinclude commodity futures and currencies – at a specified price on or before a predetermined date. Options can be a great addition to a portfolio, providing diversification benefits, a potential source of income, and a way to manage and/or reduce risk. They are also widely accessible to retail investors, especially since the introduction of sophisticated put and call writing strategies in mutual fund and ETF format.

For more detailed information on this asset class, read our Introduction to Options.

Hedge funds

There is no one specific strategy for the “hedge fund” asset class; rather, the term refers to how the investments are structured. Hedge funds are generally pooled investments that are registered as either limited partnerships (LPs) or limited liability companies (LLCs). A common theme among them, however, is that they are, for the most part, exclusively available to accredited investors. The Ontario Securities Commission8 defines an accredited investor as an individual:

- Who either alone or with a spouse, owns financial assets with an aggregate realizable value of at least $1 million, before taxes but net of any related liabilities, or net assets of at least $5 million; or

- Whose net income before taxes exceeded $200,000 in each of the two most recent calendar years or whose net income before taxes combined with that of a spouse exceeded $300,000 in each of the two most recent calendar years and reasonably expects to exceed that level in the current calendar year.

Some of the more widely known hedge fund strategies include the following.

Long / short equity

Essentially, long/short strategies involve buying (long) securities or ETFs that the manager believes will increase in value, and selling short those that are expected to decline. The ultimate goal of this type of strategy is to generate returns from the long positions and profit from declines in the short positions, while minimizing market exposure. Examples of different long/short strategies include:

• Long-bias equity, which maintains more long exposure than short in the portfolio. An example of this is a 130/30 fund, which would be long 130% equities and short 30%.

• Short-bias, which maintains greater short exposure than long.

• Paired trades, where a long position in a stock in a particular sector is offset by a short position for the same amount of money in another stock. An example of this might be a case where the manager believes interest rates are going to rise. The manager might take a long position in a bank, which would generally be expected to profit from rising rates, and a short position in a REIT, as real estate equities tend to be sensitive to short-term interest rate movements.

Absolute return

Most traditional equity strategies are tied to a benchmark where performance is measured relative to an index. Absolute return strategies, meanwhile, are not tied to any particular benchmark. Instead, the aim is to generate positive absolute returns over the long term, through all types of market conditions. These types of investments are generally less constrained, and managers have more freedom to play in different asset classes, according to market environment.

Event driven

In this type of strategy, the manager would analyze M&As, restructurings, bankruptcies, and other company-specific events and take positions depending on the expected outcome. For example, in the event of a merger between two companies, the manager might take a long position in the stock of one of the companies and a short position in the other.

Relative value

While markets are generally thought to be efficient, there are times when the pricing of certain securities doesn’t match their inherent value. Relative value strategies are designed to exploit these inefficiencies or anomalies. For example, two oil refiners may be priced similarly, but the manager may believe that one is overvalued while the other undervalued. Based on this analysis, the manager might choose to short the overvalued security and hold the undervalued one.

Tactical trading / global macro

These strategies may take long or short positions in a variety of asset classes, including equities, fixed income, currencies and/or commodities, based on the manager’s assessment of events or developments, whether positive or negative, in global markets.

Multi-strategy

Multi-strategy funds may use a number of different strategies, including those listed above. The ultimate goal is to generate positive returns with less volatility than a single-strategy fund. Multi-strategy funds provide investors with diverse exposure to multiple asset classes in one fund.

Commodities

Like hedge funds, the term “commodities” actually encompasses several different physical markets. “Soft” commodities, for instance, include agricultural products such as wheat, sugar and coffee. “Hard” commodities, meanwhile, include base metals (e.g., copper, iron), precious metals (gold, silver, platinum, palladium), and oil. Commodities also include futures markets where these hard and soft commodities trade.

Private equity

Private equity is direct investment in the shares of private companies that are not publicly traded on a stock exchange. Because they’re not publicly listed, private-equity investments tend to be less liquid, and long holding periods may be required. In addition, transparency is an issue because these companies are not required to comply with the same disclosures and regular financial reporting as their public counterparts. For these reasons, they are generally the domain of institutional and accredited investors.

Private debt

Private debt includes non-publicly traded fixed income securities such as distressed debt, direct lending, mezzanine financing and structured financing. This asset class is useful for companies that cannot access traditional bank lending. Some examples are small- or medium-sized businesses, start-ups, companies that are complex in nature, and even those in need of financing to avoid bankruptcy.

Debt instruments of private companies are popular with many institutional and other accredited investors, as they generally have low correlation to traditional investments such as equities and high yield, corporate and government bonds. However, like many private equity securities, they also tend to be relatively illiquid and can require long holding periods.

1 Source: McKinsey, “Thriving in the New Abnormal: North American Asset Management”

2 An exception to this is commodities, but given the high allocation to natural resources on the S&P/TSX Composite Index, this is not surprising.

3 In Exhibit 3 and 4, Canadian balanced portfolio represented by a combination of 60% Canadian equities (S&P/TSX Composite Index) and 40% Canadian bonds (FTSE TMX Canada Universe Bond Index); commodities by the Bloomberg Commodity Index; equity market neutral by the Credit Suisse Equity Market Neutral Index; long-short equity by the Credit Suisse Long/Short Equity Index; hedge funds by the Credit Suisse Hedge Fund Index; long-short credit by the Morningstar MSCI Long-Short Credit Index; and global macro by the Credit Suisse Global Macro Index.

4 During the January 1, 2008 to July 31, 2018 period, Canadian equities (as measured by the S&P/TSX Composite Index) and Canadian bonds (as measured by the FTSE TMX Canada Universe Bond Index) had a correlation of -0.02, based on monthly returns. Source: Morningstar Direct.

5 As measured by the CBOE Volatility (VIX) Index.

6 Assuming a traditional 60% equity / 40% fixed income portfolio.

7 Beta is an historical measure of the risk an investor is exposed to by holding a particular stock or portfolio compared to the market as whole. Beta is calculated using regression analysis, and you can think of beta as the tendency of a security’s returns to respond to swings in the market. A beta of 1 indicates that the security’s price will move with the market. A beta of less than 1 means that the security will be less volatile than the market. A beta of greater than 1 indicates that the security’s price will be more volatile than the market. For example, if a stock’s beta is 1.2, it’s theoretically 20% more volatile than the market.

8 Source: National Instrument 45-106 Prospectus and Registration Exemptions (NI 45-106), Section 1.1.

*****

Commissions, trailing commissions, management fees and expenses all may be associated with investment funds. Please read the prospectus before investing. If the securities are purchased or sold on a stock exchange, you may pay more or receive less than the current net asset value. The indicated rate of return is the historical annual compounded total return including changes in share/unit value and reinvestment of all distributions and does not take into account sales, redemption, distribution or optional charges or income taxes payable by any securityholder that would have reduced returns. Investment funds are not guaranteed, their values change frequently and past performance may not be repeated

Certain statements in this document are forward-looking. Forward-looking statements (“FLS”) are statements that are predictive in nature, depend on or refer to future events or conditions, or that include words such as “may,” “will,” “should,” “could,” “expect,” “anticipate,” intend,” “plan,” “believe,” “estimate” or other similar expressions. Statements that look forward in time or include anything other than historical information are subject to risks and uncertainties, and actual results, actions or events could differ materially from those set forth in the FLS. FLS are not guarantees of future performance and are by their nature based on numerous assumptions. Although the FLS contained in this document are based upon what Purpose Investments believe to be reasonable assumptions, Purpose Investments cannot assure that actual results will be consistent with these FLS. The reader is cautioned to consider the FLS carefully and not to place undue reliance on the FLS. Unless required by applicable law, it is not undertaken, and specifically disclaimed, that there is any intention or obligation to update or revise FLS, whether as a result of new information, future events or otherwise.

Copyright © Purpose Investments