The Good, the Bad and the Ugly: Three Reasons US Rates are Going Up - Context

by Fixed Income AllianceBernstein

The US Federal Reserve decided against an official short-term rate hike at this week’s meeting—hardly a surprise. But US Treasury yields continue to climb in 2018, and not all the explanations are good news.

Higher interest rates are arguably the most striking feature of the financial landscape this year. Major equity indices are virtually unchanged, and so is the US dollar, but two-year US Treasury yields are up by 60 basis points, and the 10-year Treasury is up by 50 basis points.

We see three main reasons why interest rates are rising in 2018:

1) The Good: Economic Growth Is Strong. The US economy has been rolling—and the momentum is likely to continue. Through the end of the first quarter, gross domestic product (GDP) expanded by 2.9% year over year. That’s well above any reasonable estimate of potential growth (typically between 1.75% and 2.0%). Higher-frequency indicators suggest that growth will remain healthy. If rates rise because growth expectations are up, that’s a good thing—it means investors are confident in the economy.

2) The Bad: Inflation Is Waking Up, Too. Inflation is rising along with growth. Right now, the price increases (around 2% by a variety of measures) aren’t alarming, but pressures have clearly picked up over the past few months. Rising commodity prices and robust labor markets suggest that there’s fuel for rates to rise further.

When inflation was too low in the wake of the recession, rising inflation would have been welcomed. But with the business cycle much more advanced now, further inflation increases would be bad. They could force the Fed to overtighten, hurting economic growth. Or they could drive up expectations of future inflation, impairing plans for business investment.

3) The Ugly: The Budget Balance Is Deteriorating. Growth and inflation can tell us a lot about the demand for US Treasuries, but they don’t tell us anything about supply. The government’s fiscal position determines that. And the fiscal position is, in a word, ugly.

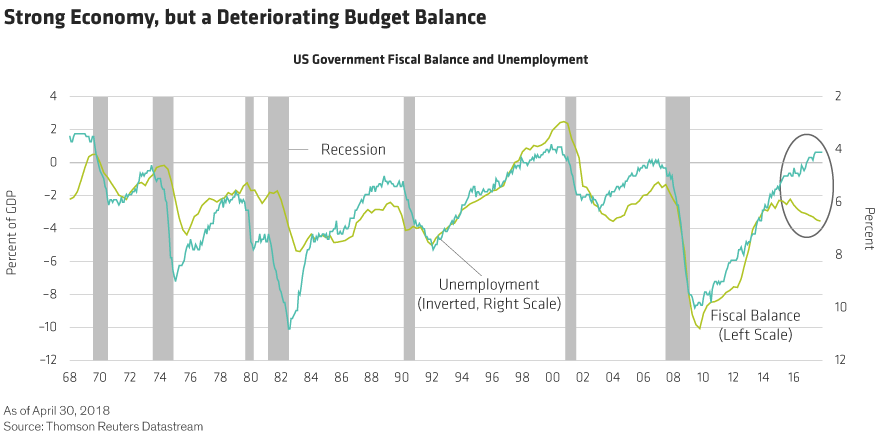

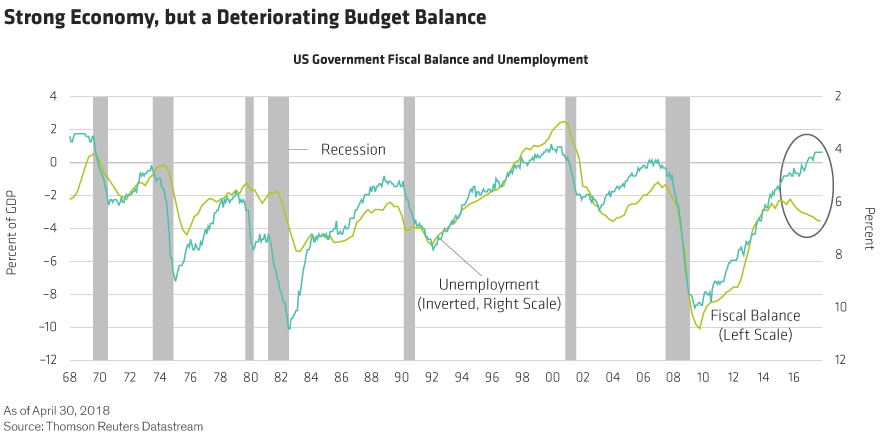

Over time, the fiscal balance—the budget deficit as a percent of GDP—strongly correlates with the business cycle. When growth is strong (and unemployment is low), tax revenues rise and the budget balance improves. Right now, though, growth is strong and unemployment is low—and the budget balance is deteriorating, not improving (Display).

The culprit? The tax cuts and the spending package passed by Congress. The risk of a buyers’ “strike,” in which investors demand sharply higher yields for holding more US Treasuries, spikes in these conditions. That’s not the base case in our forecast, but it would be a very ugly development.

So, how have these three factors combined to impact our forecasts?

Strong growth and rising inflation underpin our projection of higher interest rates. We’ve expected rates to rise for a while, and so far the moves have been generally in line with our forecasts. We’d prefer to see rising growth expectations be the only driver of higher rates, but rising inflation will inevitably play some role. That’s why we think growth will stabilize, not continue to accelerate.

The fiscal indiscipline, though, is beyond what we expected. We think the effect—over time—will be unambiguously negative.

The Price of Abandoning Fiscal Discipline

As we mentioned, fiscal deterioration increases the risk of a buyers’ strike. Again, that’s NOT our base case, and we have no way to forecast when—or if—a disruptive market event will happen. But we can say confidently that the risks of that scenario have risen. Even if that sort of disruption doesn’t happen, the lack of fiscal discipline—and the associated increase in the supply of US Treasuries—is likely to push rates higher than growth and inflation suggest they should be.

The other big issue with expanding the budget deficit now: it’s harder to do it the next time the economy slumps. Fiscal stimulus makes sense in a downturn, but right now is exactly the time to be saving money to prepare for the next slowdown. When that time comes, the stimulus will cost a lot more than it needs to.

None of this is a reason to panic in the near term. Growth is strong, which can hide a lot of structural weaknesses. But higher deficit spending borrows from future growth to boost today’s growth. It’s better to have fuel to burn when the economy is weak than it is to toss fuel onto an already hot economy.

As we see it, rates should continue to rise in the next few months, and we’re watching closely for signs that rising inflationary pressure or an increasing debt supply could push rates up more sharply than we expect right now.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

Copyright © AllianceBernstein